Princeton sociologist and MacArthur Fellow Matthew Desmond won the 2017 Pulitzer Prize for nonfiction for his book, “Evicted: Poverty and Profit in the American City.” In it, he follows eight Milwaukee families as they face the trauma and destabilization of evictions, which he considers “a cause, not just a condition, of poverty.” Evictions are also incredibly common, touching the lives of millions of people each year – and plunging some of them into homelessness.

We spoke to him about the problem and possible solutions. Here’s an edited transcript:

What does it mean for housing to be affordable?

For about 100 years, there’s been a consensus in America that we should spend about 30 percent of our income on housing costs. That gives us enough money to save, to afford enough food and to buy transportation. Research shows that when families are hitting that marker of affordability, they have more money to invest in their kids. They buy more food, their kids are healthier, they get the school products they need. That’s my idea of affordability, and that goes way back to debates that were happening generations ago about what Americans should pay for their housing. For a long time, many renters met that goal for affordability, but of course today, times have changed.

When did that change, and how?

Incomes for Americans of modest means have been flat and stagnant over the last two decades, but housing costs have soared. This was especially true in the 2000s, and they haven’t soared just inexpensive cities like Seattle and Boston. They’ve soared all around the country.

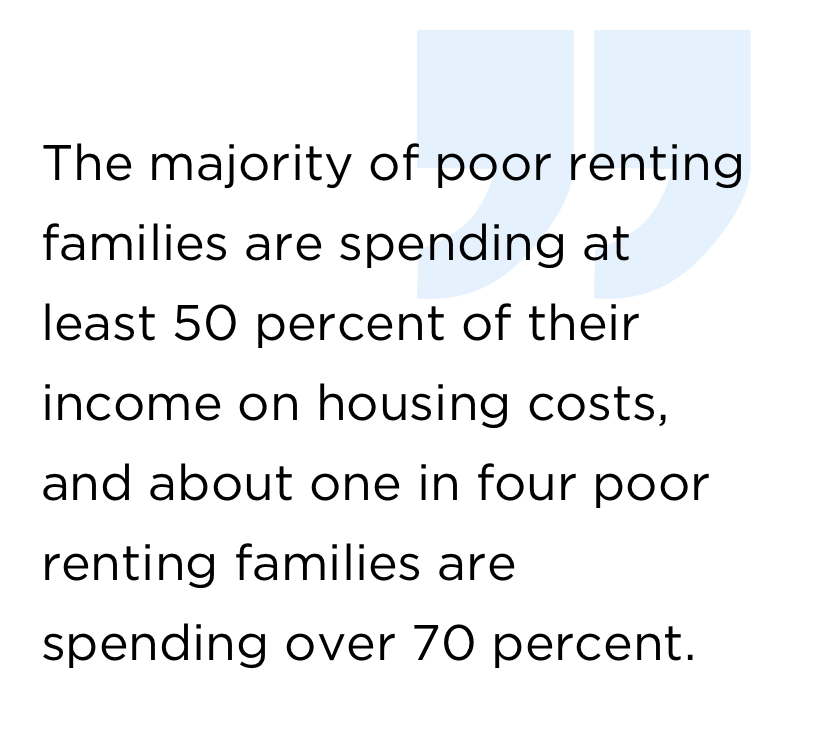

That’s created a situation where, according to the latest data from American Housing Survey, the majority of poor renting families are spending at least 50 percent of their income on housing costs, and about one in four poor renting families are spending over 70 percent of their income on housing costs.

There is housing assistance, but it’s only for a lucky minority of families below the poverty line. Only about one in four families who qualify for housing assistance today get it, because we don’t have enough to go around. We haven’t invested in this problem in a deep way.

In your book, Sherrena is a landlord who’s rich, especially compared to her tenants, and who evicts a few of them a month. But you don’t seem to blame landlords as individuals. You approach it as a systemic problem.

There are good landlords, and there are bad landlords. There are good tenants and bad tenants. Depending on what our politics are, we might be more inclined to say these landlords are greedy or these tenants are lazy, but I think if you look at it from the sidewalk view, and you spend a lot of time with folks just trying to make a living working in the low-income rental market, you understand it’s much more complicated than that. I felt that my job as a writer wasn’t to paint anyone with a simple brush. That meant trying to understand landlords’ perspectives just as deeply as tenants. That also meant not shying away from asking questions about what do they make, and are we okay with the profit margins of landlords in poor neighborhoods being as high as they are?

When did evictions become so common?

We need a lot more data on this question. When you read accounts in urban history from ‘30s and ‘40s, you’re left with a very strong impression that evictions used to be rare and scandalous and draw crowds. I remember running across this newspaper story about three families evicted in South Bronx in I think 1932, which said “because it was cold, only 1,000 people showed up to protest.” We’ve moved from that place to a place where we are likely evicting not tens of thousands or hundreds of thousands of people a year, but likely millions of people a year.

For a lot of folks on the receiving end of that, eviction has become commonplace, just a part of their life. There was this moment when I was spending time with Patrice Hinkston, and she was facing her first eviction, and she skipped court, and I said, “Aren’t you concerned that an eviction’s going to go on your record?” And she said, “Everyone I know except my white friends has an eviction record.” So we’ve moved from a place where 1,000 people are showing up in the cold to a place where Patrice can’t think of many people in her network who haven’t gone through this incredibly disruptive event.

You support the idea of a universal housing voucher program, in which everyone below the poverty line would pay just 30 percent of their income on housing.

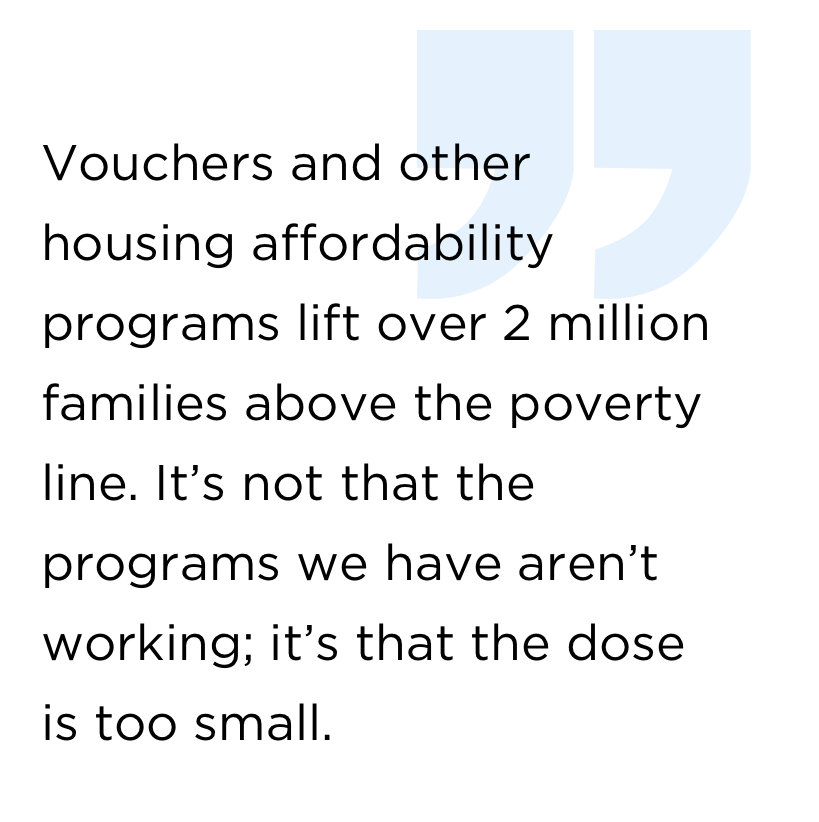

Vouchers work pretty darn well. When families see that voucher, they’re like, “Oh my gosh, I only have to spend 30 percent of my income on rent.” After spending years and years on the waiting list, they do one consistent thing with their freed-up income: They buy more food, and their kids become less anemic. They move to better neighborhoods, and they don’t move as much. Vouchers and other housing affordability programs lift over two million families above the poverty line. It’s not that the programs we have aren’t working; it’s that the dose is too small.

There seem to be a lot of unused vouchers – one person said maybe $1 billion a year. What is up with that?

In high-cost cities like Seattle and Portland, landlords have learned that it doesn’t really pay to accept a voucher tenant. It’s really embarrassing. I think the take-up rate in Portland for vouchers is something like 40 percent, so 60 percent of those vouchers get returned. So what’s going on? One thing that’s going on is that vouchers haven’t kept pace with cities like Portland, Seattle, New York, Washington that have experienced surges in housing costs. That’s one thing. Another thing is how vouchers are administered. When you finally receive a voucher, you have a certain window to find housing, and if you don’t find housing within that window, the voucher is returned. Some folks have argued that we need to do a better job of either expanding that window or expanding the housing search options of folks that do qualify and are granted a voucher.

You and others lay out the financial case very thoroughly. What are the hurdles to getting this done?

We don’t need to outsmart this problem; we need to out-hate it. We need to figure out ways of investing more in housing, and we absolutely should, because without stable shelter, everything else falls apart. Whatever your issue is, whatever keeps you up at night, whatever cause you donate to, the lack of affordable housing is somewhere at the root of that cause.

The question is, if it’s a smart investment, what trade-offs will need to be made? We have a housing policy that gives the most help to people who need it the least, affluent homeowners, and no help to people who need it the most, poor renters. There are these incredible benefits homeowners receive that renters are just left out of, including the mortgage interest deduction, which is expected to cost us over $90 billion a year in just a few years.

So, a pretty modest suggestion is to reform the mortgage interest deduction, cap it at $500,000 instead of $1 million, and redirect those savings to affordable housing programs. By one estimate, if we did that – which would affect only about 5 percent of mortgages in the United States – it would free up $87 billion over 10 years.

When you say we need to out-hate the problem, do you mean we need to realize how big it is and how many things it touches?

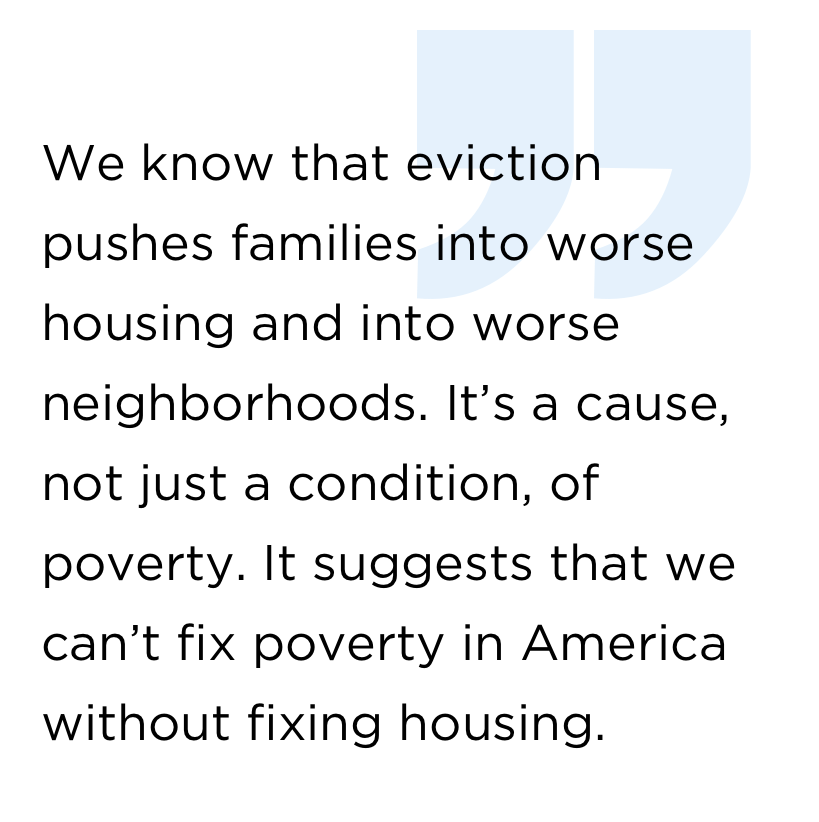

To realize how essential it is to confronting all these problems in our cities. We have a study that shows that families that lose their homes through eviction are about 20 percent more likely to lose their jobs in the following year. We know that eviction pushes families into worse housing and into worse neighborhoods. It’s a cause, not just a condition of poverty. It suggests that we can’t fix poverty in America without fixing housing.

It’s especially bad for women with children – something you compare to the way the criminal justice system affects the lives of African-American men.

The face of this epidemic is moms with kids, especially moms with kids in low-income communities of color. Among Milwaukee renters, one in five black women reports being evicted at some point in their lives, compared to one in 15 white women, which is incredible. It suggests that eviction is something like the feminine equivalent of incarceration. We have a lot of poor black men being swept up in the long arm of the criminal justice system, being locked up, and then we have a lot of poor African-American women being locked out. Especially mothers.

If you spend any time in housing court, you’ll just see tons of kids. Until recently, the housing court in the South Bronx had a day-care inside of it, because there were so many kids coming through its doors.

A study in Milwaukee showed that you can control for race and gender, you can control for even how much you owe your landlord, and what makes the difference in court is kids. If you live with kids, all else equal, the chance of you getting an eviction judgment almost triples. What you’re seeing in that finding is landlord discretion.

One tenant in “Evicted,” Larraine, occasionally buys lobster and expensive vinegar with her food stamps. You wrote, “People like Larraine lived with so many compounded limitations that it was difficult to imagine the amount of good behavior or self-control that would allow them to lift themselves out of poverty.” Can you describe those compounded limitations and what role high rents and evictions play?

Larraine was on disability. She was a grandmother, she was living in a trailer park that the city considered an environmental biohazard at the time, and she was spending over 70 percent of her income on the rent. Under those conditions, if Larraine saved 20 percent every month, at the end of the year, she’d have enough to pay for a bicycle. And that would come with nontrivial sacrifices like going without food and clothes and other things.

Under those conditions, when you’re someone like Larraine and you’re paying a huge amount of your income to rent a place that’s above your means but is at the bottom of the market, that’s a direct contribution to your poverty. And you’re facing other kinds of compounding disadvantages like isolation from the rest of the city, remnants of childhood poverty and domestic abuse, certain mental health issues, a very spotty job history — things like that coalesce into this clustering of social maladies.

Under those conditions, when you’re someone like Larraine and you’re paying a huge amount of your income to rent a place that’s above your means but is at the bottom of the market, that’s a direct contribution to your poverty. And you’re facing other kinds of compounding disadvantages like isolation from the rest of the city, remnants of childhood poverty and domestic abuse, certain mental health issues, a very spotty job history — things like that coalesce into this clustering of social maladies.

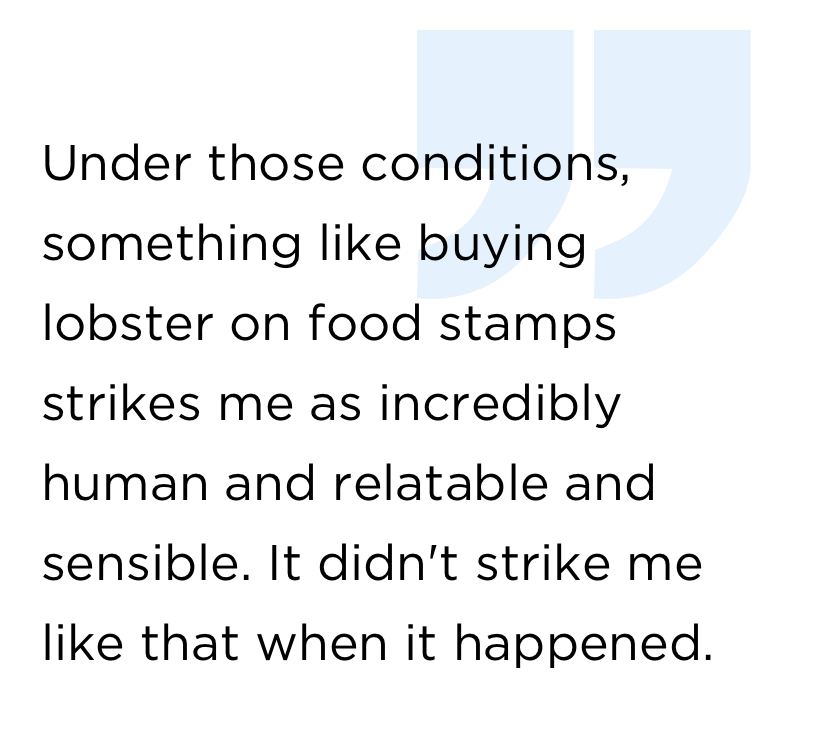

Under those conditions, something like buying lobster on food stamps strikes me as incredibly human and relatable and sensible. It didn’t strike me like that when it happened. When it happened, I was kind of angry at Larraine – not kind of angry, like, super angry.

But Larraine didn’t apologize, and she helped me understand that she’s not poor because she does stuff like that. She does stuff like that because she’s poor. That’s not just a rhetorical device. There’s a lot of work in microeconomics and behavioral psychology to back that up. Work on the earned-income tax credit shows that a lot of working poor families who receive this benefit do things like save and invest it in their children.

On a side note: I get asked about Larraine in a lot of interviews, and I never get asked about Sherrena gambling. It’s interesting to me.

Because Sherrena makes more than $100,000 a year, right?

Mmm hmm, but it’s an equally interesting question.

What do you mean?

There’s something about Larraine spending food stamps on lobster that strikes us as, like, we need an explanation, in a way that Sherrena spending the rent money on gambling doesn’t strike us as needing an explanation. Even though the rents that we see pulled from inner-city Milwaukee neighborhoods are relatively high, especially related to citywide rents, for conditions that aren’t that great, in neighborhoods that aren’t that great. So they could be a lot lower, right? Are we okay with a landlord gambling with rent money?

Related:

{kind=link}