How Concerning are Low Mortgage Volumes in Detroit?

On Thursday, May 7, Zillow will visit Detroit as part of its Housing Roadmap to 2016 series of events and roundtables.

The housing issues Detroit faces are both familiar to dozens of struggling cities nationwide, and utterly unique to the Motor City. Leading up to our May 7 visit, we will be posting a series of research pieces diving in to these complex issues. We hope to shed light on the challenges, but also to illuminate what makes the city so unique and glean potential lessons from which other struggling cities may be able to learn.

Below is the first in this series.

The number of purchase mortgages originated in the city of Detroit in recent years has been remarkably low. Depending how you slice the data, you can make the case that things are improving, or that Detroit is facing some difficult racial and geographic lending issues.

There were only 529 homes purchased with a mortgage in Detroit in 2013, up from 318 in 2011 but down from 772 in 2009, according to data from the Home Mortgage Disclosure Act (HMDA). In and of itself, the low number of purchase originations should not be a cause for concern, because home prices themselves are so low in Detroit. Comparing across metro areas, very affordable markets – both in terms of median home values and the share of income needed to afford a monthly mortgage payment – tend to have a higher prevalence of cash sales (figure 1).

In the Detroit metro, roughly half (52 percent) of all sales in Q4 2014 were cash transactions. But in the city of Detroit the share was much higher, at 80 percent. Of course, median home values in the city of Detroit were also much lower than the metro as a whole – $40,400 in the city at the end of 2014, compared to $114,000 in the larger metro.

In the Detroit metro, roughly half (52 percent) of all sales in Q4 2014 were cash transactions. But in the city of Detroit the share was much higher, at 80 percent. Of course, median home values in the city of Detroit were also much lower than the metro as a whole – $40,400 in the city at the end of 2014, compared to $114,000 in the larger metro.

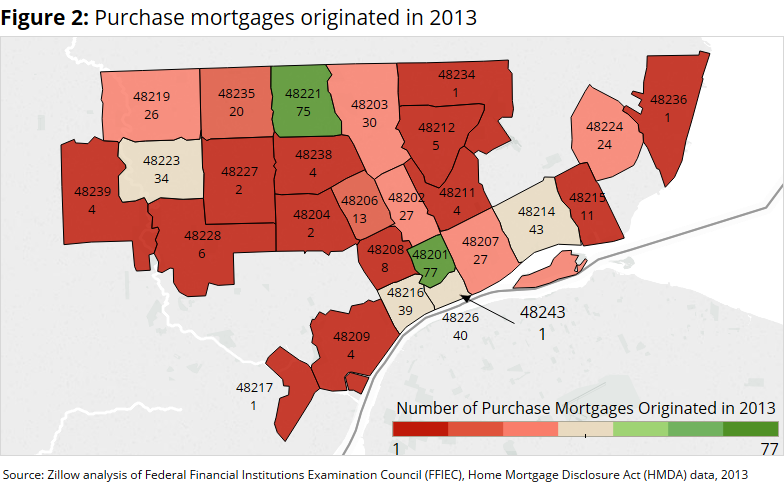

Within Detroit city limits, the broad relationship between cash sales and affordability also holds. More than one-third of the 529 purchase mortgage originations in 2013 were made in just four of the city’s 33 ZIP codes (48126, 48226, 48201 and 48207), covering the downtown core and adjacent neighborhoods (figure 2).[1] The more affordable, outlying parts of the city had far fewer of the already small number of mortgage originations.

As we’d expect, home values are higher in the areas with more mortgages: The current (March 2015) median home value in the four ZIP codes covering the downtown core is $56,000, while the median home value outside the downtown core is $40,000. The ZIP code with the largest number of purchase mortgage originations in 2013 – 48201, which includes the trendy Midtown neighborhood – also has the highest median home value of all ZIP codes in the city, at $82,900.

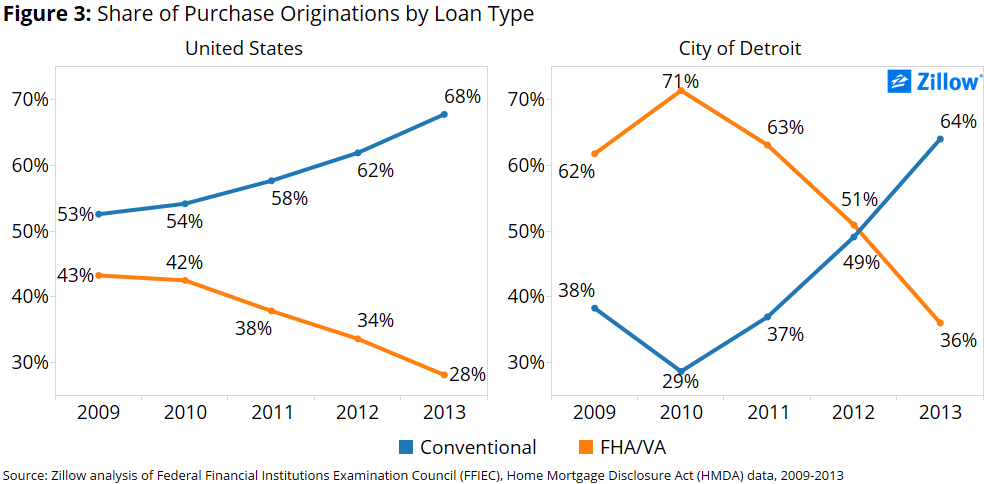

As the number of new mortgage originations in Detroit has dwindled since 2009, the types of loans originated have shifted as well. In 2010, almost three-quarters of purchase mortgage originations in Detroit were underwritten by the Federal Housing Administration (FHA) or Veterans Affairs Administration (VA) – loans targeted toward the highest-risk borrowers. By 2013, the FHA/VA share of originations had declined to about one-third (figure 3). In their place, the share of conventional loans written – those meeting the underwriting standards for Freddie Mac and Fannie Mae backing – has increased.

To some extent, these trends mirror the nation as a whole, although the movements in Detroit are more extreme. But whereas in 2010 the distribution of purchase originations in Detroit was roughly the opposite of the distribution for the nation as a whole, since then, the distributions have become more similar.

For better or worse, the types of purchase mortgages being originated in Detroit are becoming more like the types of loans being originated elsewhere.

But while the types of loans that survive the application process and are eventually originated are “normalizing” in Detroit, making it through the application process remains a challenge. Only 29 percent of loan applications started in Detroit in 2013 were eventually originated. An additional 3 percent were approved by the lender, but not accepted by the borrower, and 39 percent were purchased by the reporting financial institution from a different lender. Of all applications, including loans purchased from other lenders, 21 percent were denied.

Of course, these approval and denial rates understate the true extent of the challenges. Many potential borrowers never bother submitting an application, or are discouraged from even trying to get a loan. Of the purchase mortgage applications submitted in Detroit in 2013, 35 percent of the primary borrowers identified themselves as black, and 25 percent identified as white (37 percent did not identify a race or ethnicity). According to the Census Bureau, about 83 percent of Detroit’s population is black, and 11 percent is white. While the data on the race/ethnicity of mortgage applicants are admittedly incomplete, it is clear that black applicants are underrepresented among all mortgage applicants, relative to their weight in the city’s population.

Among new, complete applications submitted in 2013 where the primary applicant identified as black, 48 percent were approved. Among applications where the primary applicant identified as white, the approval rate was 70 percent.

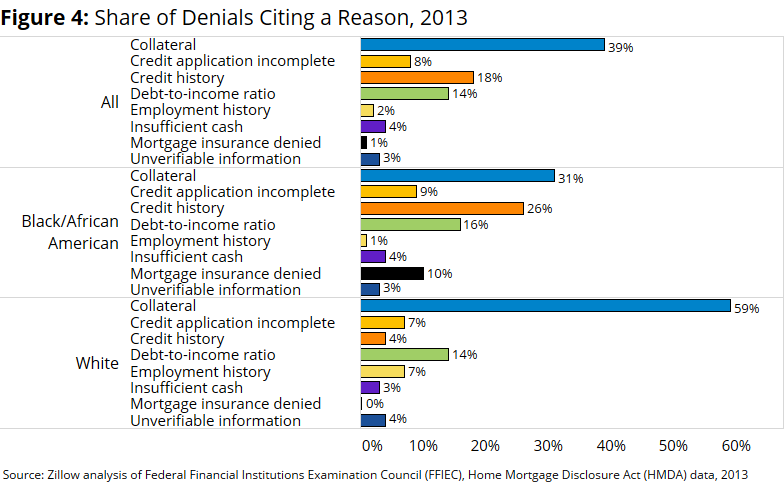

There are multiple reasons why mortgage applications are denied, but insufficient collateral was the most common primary reason cited by lenders for denying mortgage applications in Detroit in 2013, followed by weak credit histories and high debt-to-income (DTI) ratios. Again, there are striking differences across racial and ethnic groups. Among denied white applicants, collateral was cited in 59 percent of cases, credit history was cited in 7 percent of cases and high DTI was cited in 14 percent of cases (figure 4). Among black applicants, collateral was also the most commonly cited reason for denial (31 percent of denials), but it was much less frequently cited than for white applicants. Poor credit histories (26 percent) and high DTI ratios (16 percent) were much more common among blacks who had their mortgage applications denied.

There are multiple reasons why mortgage applications are denied, but insufficient collateral was the most common primary reason cited by lenders for denying mortgage applications in Detroit in 2013, followed by weak credit histories and high debt-to-income (DTI) ratios. Again, there are striking differences across racial and ethnic groups. Among denied white applicants, collateral was cited in 59 percent of cases, credit history was cited in 7 percent of cases and high DTI was cited in 14 percent of cases (figure 4). Among black applicants, collateral was also the most commonly cited reason for denial (31 percent of denials), but it was much less frequently cited than for white applicants. Poor credit histories (26 percent) and high DTI ratios (16 percent) were much more common among blacks who had their mortgage applications denied.

Overall, while the low number of mortgages originated in Detroit in recent years is not necessarily a concern in and of itself, a deeper dive into the data suggest more challenging trends, for which there are no easy answers.

[1] We exclude the largely commercial zip code 48243, which covers two city blocks in downtown Detroit.

{kind=link}