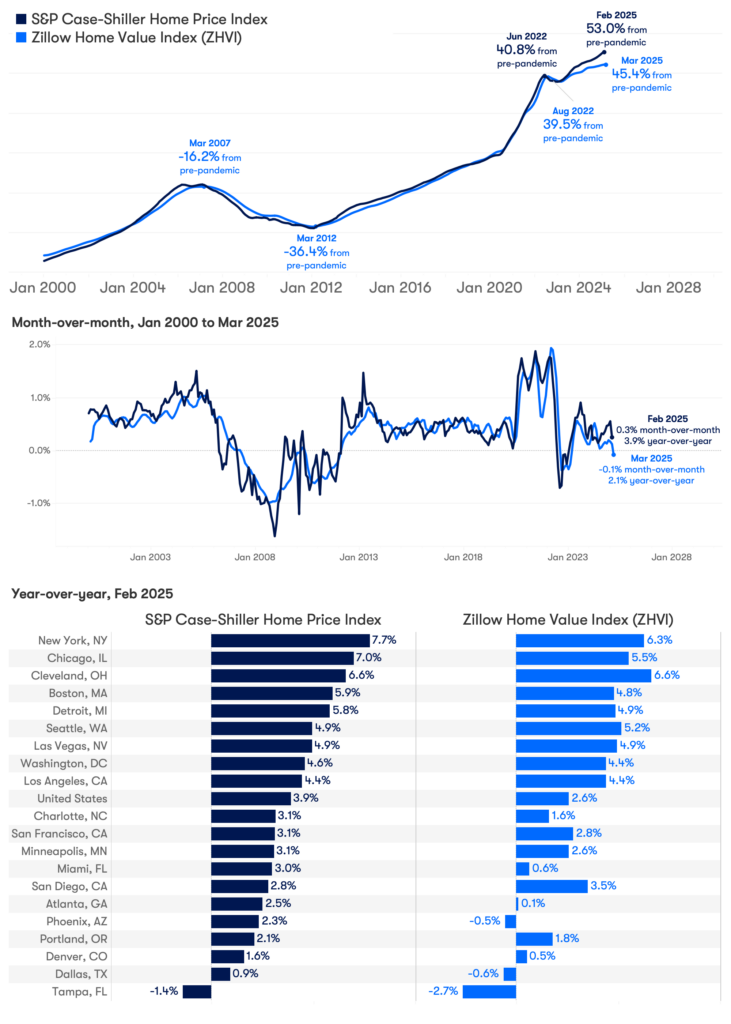

February 2025 S&P Case-Shiller Price Index: Home prices slow dramatically over February.

Home prices are increasingly untenable to potential home buyers. Waning consumer confidence, heightened insecurity over economic uncertainties and the future of household budgets are impacting the consumer housing market.

- The seasonally adjusted S&P CoreLogic Case-Shiller U.S. National Home Price Index® increased only 0.3% in February, a significant slow down from the previous month.

- Nationally, prices rose 3.9% year-over-year in February, down from 4.1% in January.

- Annual price growth also decelerated slightly in both the 10-city index and the 20-city index, though the 20-city index had softened more the previous month.

What happened:

The seasonally adjusted national S&P CoreLogic Case-Shiller Index (C-S) decelerated in February, under high mortgage rates and rising inventory nationally. Released one month earlier, March’s ZHVI seasonally adjusted appreciation adjusted to a slower pace earlier in the season, even turning negative for the first time in two years. Zillow now forecasts ZHVI to fall 1.9% by the end of 2025. The twelve-month forward forecast is now down 1.6%.

Why it matters:

Home prices are increasingly untenable to potential home buyers. Waning consumer confidence, heightened insecurity over economic uncertainties and the future of household budgets are impacting the consumer housing market. Unlike its normal countercyclical behavior, these early signs of an economic downturn have not brought lower mortgage rates along with it.

Recently, more affluent buyers have been able to leverage strong stock portfolios to outbid other buyers. However, sweeping tariffs have led to a stock market slump, affecting the down payment savings for the 29% of home buyers who use stock portfolios as a down payment source (2024 Zillow Consumer Housing Trends Report).

The trends of the next few months are incredibly important as experts grapple with another potential turning point in the macro economy and for housing.

Why the divergence:

The ZHVI and C-S began demonstrating a difference in the strength of home value appreciation midway through 2024 – another year of volatile interest rates without much pricing relief nationally. In both cases, monthly appreciation accelerated into the end of 2024, however, Zillow observed a more moderate appreciation overall. This trend began to decelerate in January 2025, and subsequent months have seen even greater slowdowns.

The cause of disagreement is likely built into the major methodological differences of the two indices: the C-S needs a repeat sales to include in its construction, likely under-capturing newer neighborhoods whose homes have yet to sell twice. By leveraging repeated Zestimates across the U.S. (using the same neural network algorithm for each subsequent month), the Zillow Home Value Index is better able to capture the influence of high rates of new construction since 2019.

A second primary difference is in their purpose. The Zillow Home Value Index captures the dynamics of the middle third of the market to focus on the experience of a customer shopping for homes. The C-S is value weighted across the whole distribution to follow the value of housing taken as an investment portfolio.

{kind=link}