- Lower incomes, smaller down payments, mortgage insurance and a relative lack of lower-priced homes make buying for first-timers marginally more difficult.

- First-time homebuyers should expect to pay about 17.4 percent of their income to a mortgage, compared to 15.3 percent for more traditional buyers.

- However, current affordability for first-time buyers still looks favorable to pre-bubble norms from 1985 to 1999, when they could have expected to pay about 22.5 percent of their income to a mortgage.

As rents continue to soar, buying a home looks like a downright bargain compared to renting. But not all home buyers are created equal, and younger, first-time buyers will face a few additional hurdles that more experienced buyers may not have to contend with.

It’s true that buyers of all means who step into the market today will have a much different (and likely a bit better) experience from that of home shoppers in the recent past, thanks to gains in inventory, continued low mortgage rates and less competition from investors and all-cash buyers. Additionally, the oldest millennials are reaching their mid-thirties and slowly joining the home buying hunt, helping to boost demand in the market and encouraging some sellers who may have had trouble finding buyers for their homes in previous years.

But the realities of the Great Recession remain, particularly for younger Americans. Many households lost their jobs, their homes and their savings during the recession, which pushed them into rentals en masse. This surge in rental demand led rents to rise to unaffordable levels and forced many traditional renters—new graduates and younger workers earning entry-level salaries—to compete for available apartments with families displaced by foreclosure. At the same time, college educations became more expensive, and many millennials left school saddled with huge debt burdens.

So while unemployment rates are dropping and labor markets are picking up, overall savings are still lagging. Putting 20 percent down on a home remains impossible for many millennial, first-time homebuyers. So how affordable is a mortgage for the average millennial or first-time buyer?

To answer this question, we assume a first-time buyer makes the median income of all 23- to 34-year-olds in a given area[1], attains a 30-year fixed rate mortgage with only 5 percent down and shops for a home priced according to the 33.3 percentile[2] of all home values[3]. By contrast, our traditional affordability numbers are reported assuming a household earns the median household income across all ages, purchases the median (50th percentile) valued home with 20 percent down on a 30-year fixed rate mortgage.

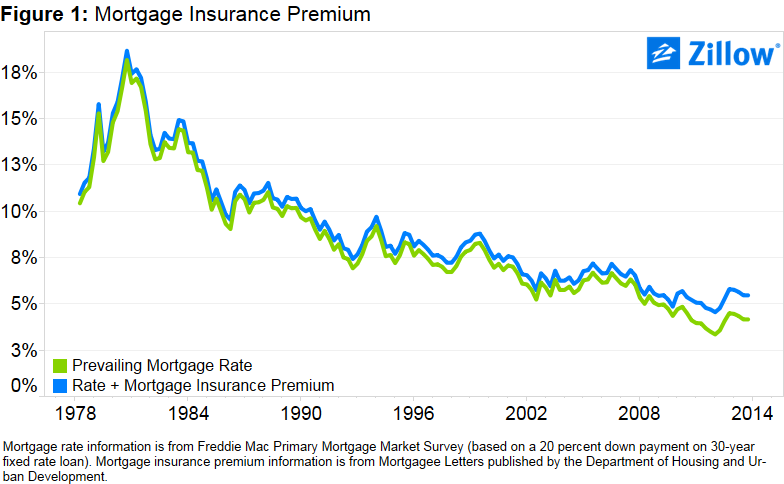

In order to secure a loan with less than 20 percent down, the first-time buyer also pays primary mortgage insurance and upfront fees.[4] Mortgage insurance is not negligible. In the third quarter of 2014, mortgage insurance added an average of 1.3 percentage points to the effective mortgage rate.

The first-time buyer may buy a less expensive property, but the lower purchase price is more than offset by a higher effective interest rate and a larger share (95 percent) of the sale price spread out over the 30-year term. Add lower incomes into the mix, and the first-time buyer can expect to pay a larger share of a smaller income to the bank every month.

Finally, buyers seeking lower-priced homes may find them in short supply in many areas, as lower-priced inventory either remains trapped in negative equity or was previously scooped up by investors and turned into rental housing over the past few years. In Denver, for example, there were almost four times as many homes available for sale in October in the upper price tier (homes priced at $357,900 or more) than there were homes priced in the lowest price tier (less than $219,000). The same was true in many other markets. Dallas, Atlanta, Phoenix and Nashville all had at least two times more homes for sale in the top tier than the bottom tier.

The interactive visualization below compares our first-time homebuyer affordability series to our traditional affordability numbers, both mortgage and rental affordability (the median rent as a fraction of median household income). The bar charts at the bottom summarize the major differences faced by the first-time buyer: lower-priced homes, lower income levels and higher effective mortgage rates.

While mortgages are less affordable for the first-time buyer relative to the traditional buyer, for both groups mortgages remain a bargain, both compared to the share of income spent on a mortgage historically and compared to the current share spent on rent. It’s likely that as life catches up to millennials approaching marriage, the rent on a larger unit needed to accommodate a new family will become prohibitive. Young couples and families will turn to the more affordable mortgage market while rates remain low, and join the ranks of first-time homeowners in coming years.

Please use the drop down menu to explore your metro area.

[1] The median income of 23- to 34-year-olds is estimated from a custom analysis of survey responses collected by the Census Bureau. These surveys include the 1990 and 2000 Decennial Censuses and the 1-year American Community Surveys (ACS) from 2006 to 2013 (IPUMS-USA, University of Minnesota, www.ipums.org). Income between decennial years and the 2006 ACS is the result of linear interpolation. Income is chained forward from 2013 and back from 1990 using the Employment Cost Index reported by the Bureau of Labor Statistics.

[2] The 33.33rd percentile of home values divides the bottom and middle tiers.

[3] Home values are chained back from 1996 using the House Price Indices published by the Federal Housing Finance Agency (FHFA).

[4] The prevailing premium upfront fees for mortgage insurance is drawn from the Mortgagee Letters published by the Department of Housing and Urban Development.