Hidden Costs of Homeownership Top $9,000 a Year

Prepare yourself by knowing the less-obvious costs of owning a home. Insurance, maintenance and more add up faster than you think.

Prepare yourself by knowing the less-obvious costs of owning a home. Insurance, maintenance and more add up faster than you think.

The everyday expenses of owning a home that many homeowners might pay little attention to – utility bills, property taxes, insurance and basic maintenance – add up to an attention-grabbing sum: Almost $10,000 per year for the typical U.S. homeowner.

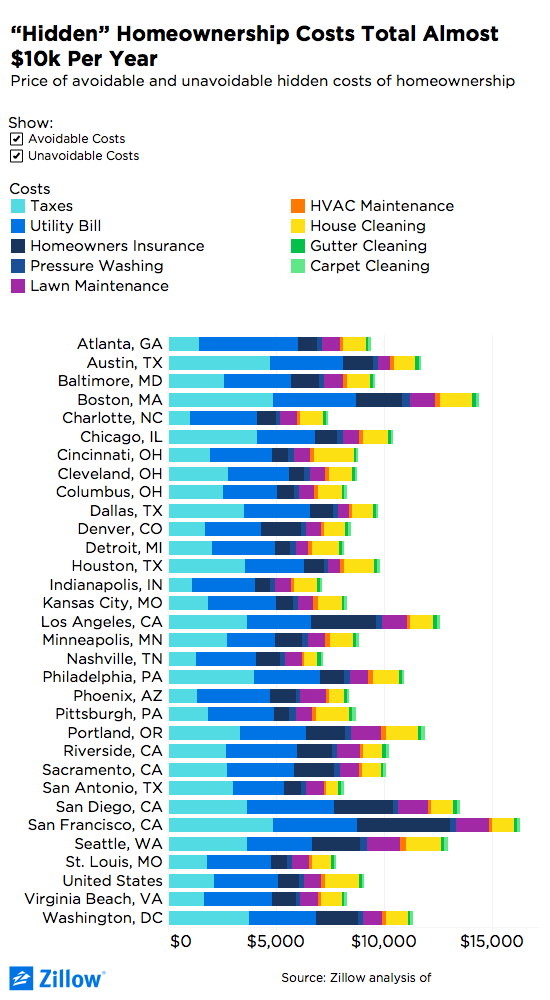

The hidden costs of homeownership can add up to $9,080 per year for the typical U.S. homeowner, and even more in some local markets, according to a new analysis from Zillow and Thumbtack. That amounts to an extra $757 per month above and beyond the monthly mortgage for the typical homeowner in the U.S. Zillow and Thumbtack’s research examined three unavoidable monthly expenses – property taxes, homeowners insurance and utility payments[1] – as well as six “optional” but very common home prep costs including cleaning, landscaping and basic maintenance.[2] Nationwide, unavoidable costs total $6,059 per year, while the optional maintenance and cleaning costs add another $3,021 annually.

Death and taxes are, of course, entirely unavoidable. But homeowners can at least save big on their tax bills depending on where they live because of the vagaries of local tax laws. The typical U.S. homeowner pays $2,110 per year in property taxes, although that varies dramatically among the 31 local markets included in this analysis, from a high of $4,865 per year in the Boston metro to a low of $1,021 on average in the Charlotte market.

In some areas, assessors’ offices might have little incentive to regularly update a home’s assessed value, particularly in slower-moving or more rural areas with more uniform home value appreciation across neighborhoods, or where assessors’ resources are stretched thin. In other places, assessors simply can’t significantly increase property taxes – despite home value growth – because of local laws.

Such is the case in California, where a state law known as Proposition 13 limits the rate at which a homeowner’s tax bill can increase. Because of this, homeowners in many California markets enjoy fairly low tax bills relative to their home’s value. For example, despite the fact that median home values in the San Francisco metro are almost twice what they are in and around Boston, Boston and San Francisco-area residents pay similar annual property taxes, ($4,865 and $4,831, respectively). Other metros with high annual total property tax bills include Austin ($4, 728) and Chicago ($4,117).

It also costs a lot to keep a home energized and comfortable all year long: The typical U.S. homeowner pays almost $3,000 per year ($2,953) in utility costs to keep the lights on, water flowing and HVAC running. Total utility costs are determined by both the rates set by local utility companies and regulators, and the amount of energy and water used in a given area. Areas with very hot summers and/or very cold winters, for example, may see seasonal spikes in energy usage to keep the A/C and heat on.

The highest estimated annual utility bills are in Atlanta ($4,557), San Diego ($4,042), San Francisco ($3,928) and Boston ($3,815). Markets with the lowest annual utility costs include Minneapolis ($2,234), San Antonio ($2,370), Columbus ($2,456) and Denver ($2,567).[3]

Last and lowest among the unavoidable costs of homeownership are annual homeowners’ insurance costs – although, like both property taxes and utility bills, individual insurance costs can vary dramatically from market-to-market and homeowner-to-homeowner.[4]

Nationwide, the typical homeowner pays slightly less than $1,000 per year in insurance costs ($996), on average, with a high of $4,260 in the five-county San Francisco Bay Area and a low of just $670 per year in and around Cleveland. But owners of properties located in a flood zone, for example, should expect to pay much higher insurance rates if they’re required to purchase federally-backed flood insurance. Additionally, some homeowners may choose to add pricier coverage to their homes, including added protection from wildfires, earthquakes, burglary and other optional insurance riders.

While property taxes, homeowners’ insurance and utilities are unavoidable, many homeowners choose to pay for any number of optional services to save time and/or improve the quality of their home and lives.

The most popular of these kinds of “optional” services include house cleaning, lawn maintenance/landscaping, carpet cleaning, gutter cleaning, pressure washing and HVAC maintenance, and run the typical U.S. homeowner $3,021 per year. But these costs are highly dependent on the cost of labor in a given area.

The biggest annual price tags for these services are in Seattle ($4,052), Portland ($3,674), Boston ($3,570) and San Francisco ($3,271). The least-expensive markets for these sorts of optional services are clustered in Texas and the Southeast, and include San Antonio ($1,962), Nashville ($1,997), Dallas ($2,082) and Austin ($2,235).

Given that almost half of home shoppers (47 percent) are first-time buyers, some of these costs may come as a surprise and will definitely have a meaningful impact on potentially tight household budgets. Determining how much you can afford is one of the most challenging aspects of home buying, especially for first-time buyers. Before starting a home search, it’s critical to take a good look at your finances to determine a monthly payment range you can comfortably afford.

While that big back yard or larger home may be appealing, it is important to consider how much maintaining those spaces could cost you.

[1] Utility cost data is provided from UtilityScore

[2] Zillow and Thumbtack’s Hidden Costs of Homeownership report factored in three unavoidable monthly expenses (property taxes, homeowners insurance and utilities from Utility Score) as well as six basic home prep costs from Thumbtack. Thumbtack looked at tens of thousands of quotes from small business professionals around the country and determined the average cost for each expense within the selected metros. For the purposes of this analysis, carpet cleaning, yard work, gutter cleaning, HVAC maintenance, house cleaning and pressure washing were identified as six of the most popular home maintenance-related projects.

[3] Zillow aggregation of ZIP code-level median utility bill estimates for single family homes provided by UtilityScore. Utility bill totals specifically accounted for electricity, natural gas, water, and sewer bills. To aggregate to the metro level, we weighted by property counts.

[4] This analysis assumes homeowners pay 0.5% of their home’s value every year in homeowners insurance, which we calculate as 0.005 multiplied by the area’s median home value (as measured by the Zillow Home Value Index).

{kind=link}