Home Values Are Back, Except Where They’re Not

The median U.S. home value is back to its pre-recession peak, but not all markets behave the same. Denver recovered years ago, while Las Vegas still has a long way to go.

The median U.S. home value is back to its pre-recession peak, but not all markets behave the same. Denver recovered years ago, while Las Vegas still has a long way to go.

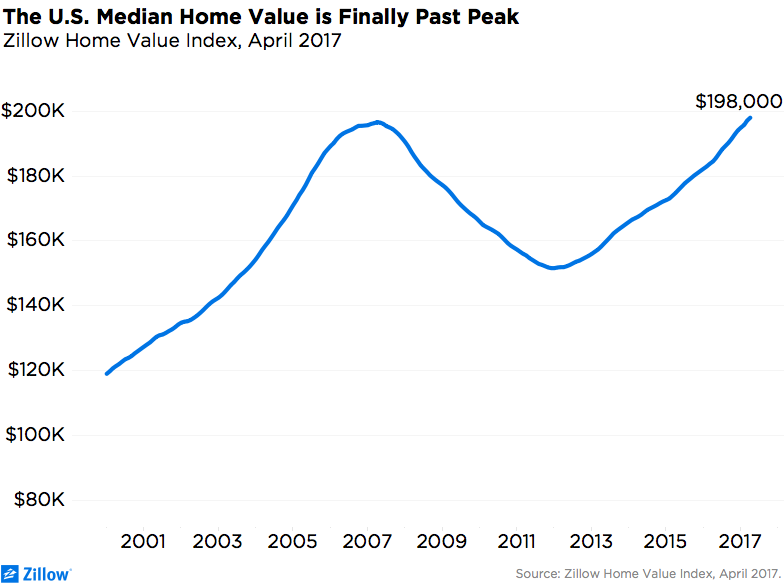

Ten long years after climbing to a frenzied housing-bubble peak of $196,600, then crashing into the worst economic downturn since the Great Depression, the median U.S. home value finally has passed that earlier peak — in March, the Zillow Home Value Index (ZHVI) reached $197,100. All signs are that it will continue to chug along, driven this time by the economic fundamentals of supply and demand.

Ten long years after climbing to a frenzied housing-bubble peak of $196,600, then crashing into the worst economic downturn since the Great Depression, the median U.S. home value finally has passed that earlier peak — in March, the Zillow Home Value Index (ZHVI) reached $197,100. All signs are that it will continue to chug along, driven this time by the economic fundamentals of supply and demand.

However, the median does not tell the story of a nation.

To get that, it’s important to look at individual markets — and they tell different stories, including many that have not yet returned to their former peaks.

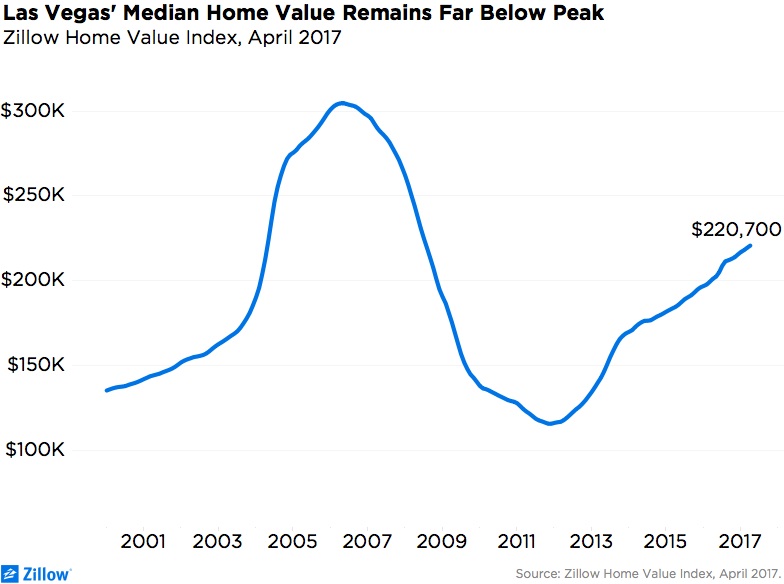

Las Vegas remains the most behind. Local home values are gaining — in April 2017, the median home value in Las Vegas grew at a faster pace than the national median, up 9.7 percent from a year earlier. Now at $220,700, the median in Las Vegas is well above the national median of $198,000 — but still 27.6 percent below its May 2006 peak of $304,700. There’s no telling how long it will take to get back there.

Crippled by debt, Las Vegas homeowners continue to struggle. At one point, more than 70 percent of the area’s mortgages were underwater; many homeowners stopped paying their mortgages for months and years at a time with little consequence. Some filed for bankruptcy and walked away, assuming lenders would take ownership, only to return years later to find homes still in their names. Sometimes, their homes had been taken over by squatters or, more absurdly, by renters making monthly payments to someone pretending to be the owner.

Crippled by debt, Las Vegas homeowners continue to struggle. At one point, more than 70 percent of the area’s mortgages were underwater; many homeowners stopped paying their mortgages for months and years at a time with little consequence. Some filed for bankruptcy and walked away, assuming lenders would take ownership, only to return years later to find homes still in their names. Sometimes, their homes had been taken over by squatters or, more absurdly, by renters making monthly payments to someone pretending to be the owner.

Negative equity in Las Vegas at the end of 2016 stood at 16.6 percent, way down from its peak but still the highest rate among major U.S. metro areas. Other markets in which median home values continue to fall short of their bubble-era peaks include Orlando, Fla. (home values are down 20.2 percent from peak), Miami (17.9 percent), Phoenix (14.7 percent) and St. Louis (6.2 percent).

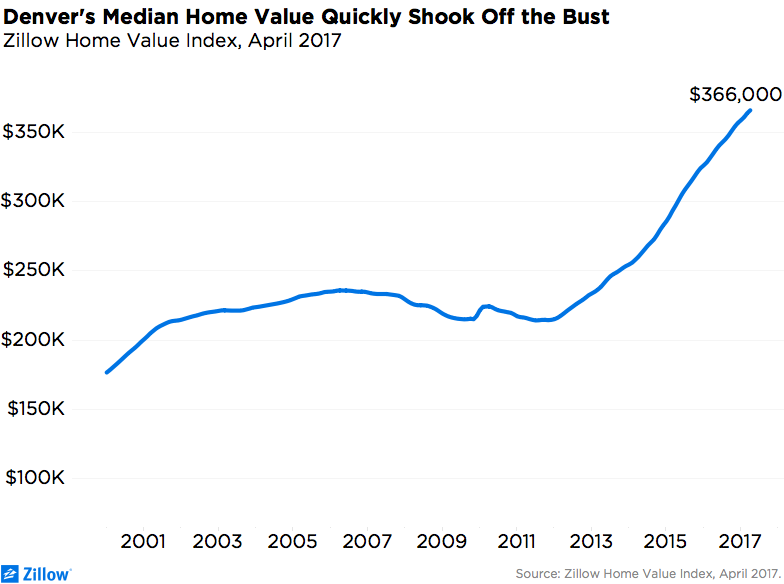

On the other end of the spectrum is Denver, which quickly shook off the bust – home values passed their pre-recession peak of $235,900 four years ago (March 2013) and haven’t looked back. Denver’s median home value in April was $366,000 — up 54 percent from its bubble-era peak. Denver can thank its massive population growth and its limited supply of new homes for sale. Such rocket-like growth could indicate a local bubble starting to form in Denver and similar fast-growing markets, like the Bay Area. However, rapid growth alone does not indicate a bubble if prices are driven by solid economic fundamentals like strong job growth, wage gains, true demand and limited supply — which is the case in Denver.

On the other end of the spectrum is Denver, which quickly shook off the bust – home values passed their pre-recession peak of $235,900 four years ago (March 2013) and haven’t looked back. Denver’s median home value in April was $366,000 — up 54 percent from its bubble-era peak. Denver can thank its massive population growth and its limited supply of new homes for sale. Such rocket-like growth could indicate a local bubble starting to form in Denver and similar fast-growing markets, like the Bay Area. However, rapid growth alone does not indicate a bubble if prices are driven by solid economic fundamentals like strong job growth, wage gains, true demand and limited supply — which is the case in Denver.

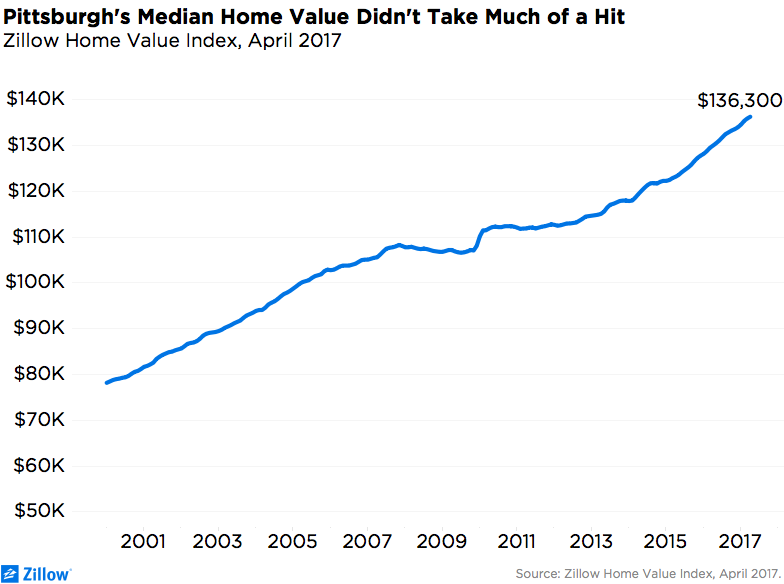

Some fortunate markets, like Pittsburgh, stuck to those fundamentals all along and missed the dramatic boom-and-bust cycle that the rest of the country suffered through.

Some fortunate markets, like Pittsburgh, stuck to those fundamentals all along and missed the dramatic boom-and-bust cycle that the rest of the country suffered through.

Steel City has experienced steady home value growth for the past two decades, with only some modest flattening between 2008 and 2013. Like the stable (and incidentally, affordable) housing market that it is, Pittsburgh has continued to hit “peak” home values ever since, and in April posted a median home value of $136,300.

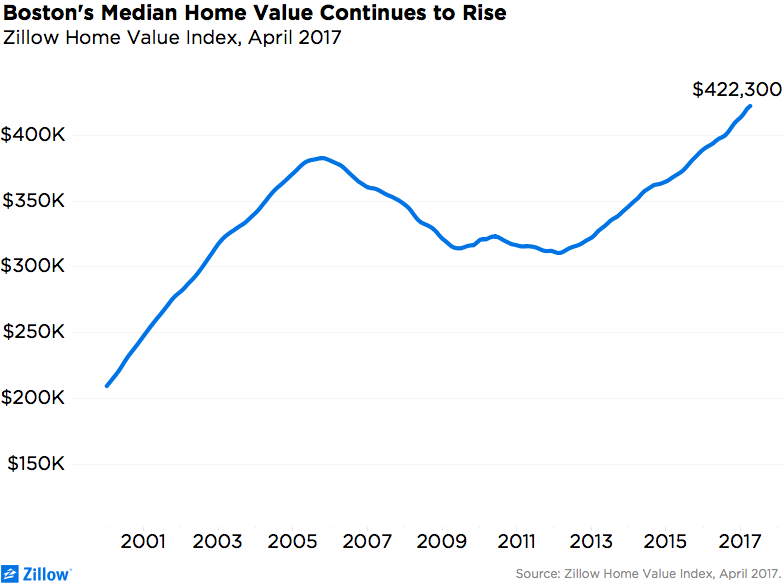

A market that more closely reflects the experience of the overall U.S. housing bubble and decline is Boston, where home values peaked a little earlier than the rest of the country — in November 2005 — at $382,700. That was followed by six long years of falling home values, then a gradual return to its pre-recession peak, in November 2015. A full decade.

A market that more closely reflects the experience of the overall U.S. housing bubble and decline is Boston, where home values peaked a little earlier than the rest of the country — in November 2005 — at $382,700. That was followed by six long years of falling home values, then a gradual return to its pre-recession peak, in November 2015. A full decade.

Related:

{kind=link}