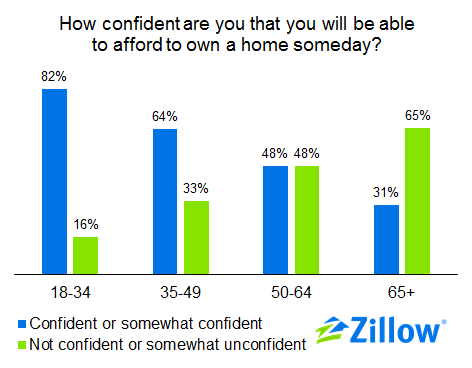

- More than 80 percent of young adult renters aged 18 to 34 are “confident” or “somewhat confident” that they will eventually be able to afford a home.

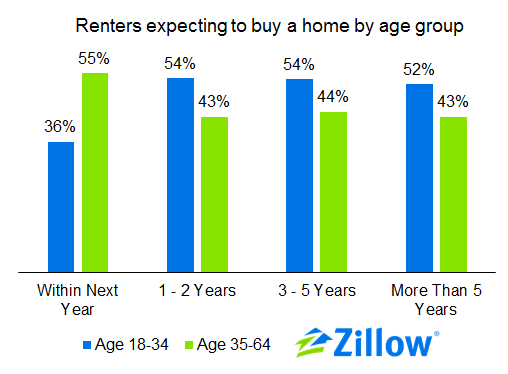

- Slightly more than one third (36 percent) of renters aged 18-34 said they expect to buy a home within the next year. But more than half (54 percent) of 18-34-year-old renters said they expect to buy a home in 1 to 2 years or 3 to 5 years.

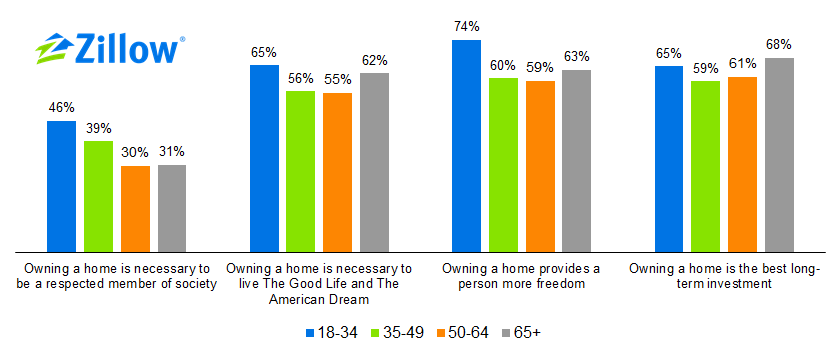

- Nearly two-thirds of young adults said they think that owning a home is necessary to live “The Good Life” and the “American Dream.”

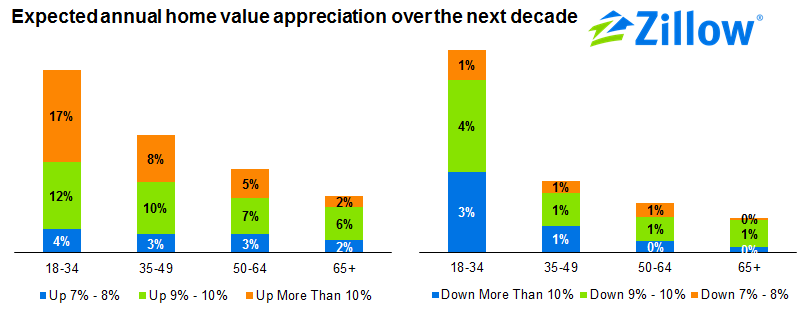

- When asked about their expectations for home value appreciation over the next decade, young adults appear to have exaggerated expectations. They are more likely than older age groups to think that home values will rise rapidly, and they are also more likely to think that home values will fall dramatically.

Despite the housing market tumult that marked their formative years, young adults remain optimistic about homeownership and, in some respects, hold more conventional views than older generations, according to results from the latest Zillow Housing Confidence Index (ZHCI).

The ZHCI is sponsored by Zillow and developed and administered by Pulsenomics LLC. The index is based on the results of the Housing Confidence Survey, which consists of more than 10,000 interviews across 20 different metro areas. (More information about the index and the survey can be found here.)

Young adult renters are very confident that they will someday be able to afford a home…

Among renters, confidence about future homeownership is very strong among young adults but fades for older cohorts. Over 80 percent of young adult renters age 18 to 34 are “confident” or “somewhat confident” that they will eventually be able to afford a home compared to 64 percent of prime working-age renters age 35 to 49, 48 percent of older adults age 50 to 64, and 31 percent of senior citizens age 65 or older.

In some respects, the downward trend is not surprising: Individuals who have not become homeowners by old age likely face a number of other barriers to homeownership, or have explicitly chosen not to become homeowners. By contrast, younger renters may still be students or are just starting their careers with temporarily low incomes but higher long-term income trajectories.

This pattern holds across the country, but there are notable differences across metro areas. Young adults are most confident that they will eventually be able to afford a home in Phoenix, Miami and Detroit – all places where housing is relatively affordable. At the other extreme, young adults were least confidence that they will eventually be able to afford a home in Philadelphia, Seattle and San Diego.

But their timelines have been pushed back somewhat.

Although many young renters expect to buy homes, their timelines have been delayed somewhat. Of renters who expect to buy a home, young adults remain a minority of expected buyers over the next year. But looking beyond a year, they become the majority of expected home buyers. Slightly more than one third (36 percent) of renters aged 18-34 said they expect to buy a home within the next year. But more than half (54 percent) of 18-34-year-old renters said they expect to buy a home in 1 to 2 years or 3 to 5 years.

Nationwide, 10 percent of renters overall said they plan to buy a home within the next year, and 35 percent said they plan to buy within the next two years. If these plans are realized, this would translate into about 4.3 million new owner households next year, and would lift the homeownership rate from 64.8 percent in 2013 to about 66.9 percent in 2015.[1] Still, jumps of this magnitude are rare in the history of the homeownership rate, suggesting that many of these plans will not come to fruition.

In some respects, young-adults’ views on homeownership may be more conventional than older adults.

Despite the suggestion that societal views on homeownership are shifting in the wake of the Financial Crisis, young adults still see homeownership as a marker of status and stability.

Nearly two-thirds of young adults said they think that owning a home is necessary to live “The Good Life” and the “American Dream.” Almost half said they believe that owning a home is necessary to be a respected member of society, and nearly three-quarters said they think that owning a home provides a person more freedom than renting – higher than for any other age group. When asked if owning a home is the best long-term investment, young adults expressed slightly more skepticism than the elderly, but still viewed the returns on homeownership more favorably than adults age 35 to 64.

And these more traditional views are not limited to the heartland, but are instead fairly widespread. For instance, young adults in Miami (82 percent), Detroit (76 percent) and Tampa (72 percent) are most likely to agree that owning a home is necessary to live “The Good Life” and “The American Dream.” Young adults in Denver (51 percent), Dallas (54 percent) and Philadelphia (56 percent) said they were least likely to agree with the statement. When asked whether owning a home is necessary to be a respected member of society, the largest share of young adults saying they agreed were clustered in Los Angeles (59 percent), St. Louis (54 percent) and New York (54 percent).

When it comes to assessing whether or not housing is the best long-term investment, recent experience seems to play an important role. The largest shares of young adults who said they think housing is the best long-term investment were in Los Angeles, Miami and Phoenix – all metro areas where home prices have recovered strongly since the recession. Young adults are more inclined toward other investments in St. Louis, Minneapolis and Seattle. St. Louis, which has experienced very slow home value growth in recent years, is the only metro area in the survey where young adults indicated they think that housing is not the best long-term investment.

Young adults are more likely to think that home values will go up a lot… and to think that they will go down a lot:

When asked about their expectations for home value appreciation over the next decade, young adults appear to have exaggerated expectations. They are more likely than older age groups to think that home values will rise rapidly, and they are also more likely to think that home values will fall dramatically.

About one-third of young adults surveyed said they expect home values to increase by at least 7 percent per year over the next decade, compared to 21 percent of adults aged 35 to 49, 15 percent of adults aged 50 to 64, and 10 percent of adults aged 65 and older. At the other extreme, 8 percent of young adults said they expect home values to fall by 7 percent or more each year over the next decade, compared to just 3 percent of adults aged 35 to 49, 2 percent of adults aged 50 to 64, and 1 percent of adults aged 65 and older. Across the 20 metro areas where the survey was conducted, the median annual home value appreciation over the past decade and a half was 4 percent.

[1] This calculation assumes that the number of households grows in 2014 and 2015 at the average rate observed between 1977 and 2013. If the number of households grows more slowly than the historical rate, the homeownership rate will jump further.