Housing Demand in a High-Inflation World: Why Non-Shelter Inflation Might Not Dent Buyer Demand

Buying a home today with a fixed-rate mortgage can be a hedge against housing inflation, locking in the cost of shelter even as other prices may rise.

Buying a home today with a fixed-rate mortgage can be a hedge against housing inflation, locking in the cost of shelter even as other prices may rise.

The Consumer Price Index – the most-commonly used measure of inflation – is currently rising at its fastest pace since the early 1990s, and consumers are coming to grips with inflation in ways they haven’t had to in a generation. But while prices for seemingly everything seem to be on the rise, what this inflationary spike means for housing in particular is much less clear.

Buying a home today with a fixed-rate mortgage can serve as a hedge against housing inflation, locking in a fixed monthly cost of shelter, and securing a place to live, insulated from the risks of rising prices, interest rates, and rents. We just experienced the fastest-ever pace of increase in home prices, as well as a rapid rebound in rents, so potential homebuyers may still be keen to guard against future rises in housing costs. The rise in prices of everything else, meanwhile, could leave potential homebuyers with less budget room for their mortgage payment; or it could make housing look relatively more attractive as a worthwhile place to spend. That latter effect, combined with rising costs for builders to construct new homes, could contribute to home prices rising further in the near term, pushing homeownership further out of reach for potential first-time buyers.

One of the most widely used measures of the general price level, the Consumer Price Index (CPI) is meant to capture changes in a standardized basket of goods and services that typical U.S. households will purchase in a typical month – including, among other things, fuel, food and housing. The cost of housing contributes to CPI through its “shelter” component, consisting mostly of so-called Owner’s Equivalent Rent, and, to a lesser extent, actual rent paid by tenants. Owners’ Equivalent Rent is estimated by asking homeowners how much their home would cost to rent, and is intended to capture the value of the flow of housing services provided by the home they own, not the changing cost of purchasing a home or the monthly cost of mortgage payments or property taxes.

While growth in the shelter component of CPI has begun accelerating recently, rising 3.5% year-over-year in October, it is nonetheless lagging behind both annual home price appreciation (up 19.2% year-over-year in October) and observed rents (up 14.3% year-over-year in October). It is likely that annual growth in the shelter component of the CPI will continue to rise in the coming months.

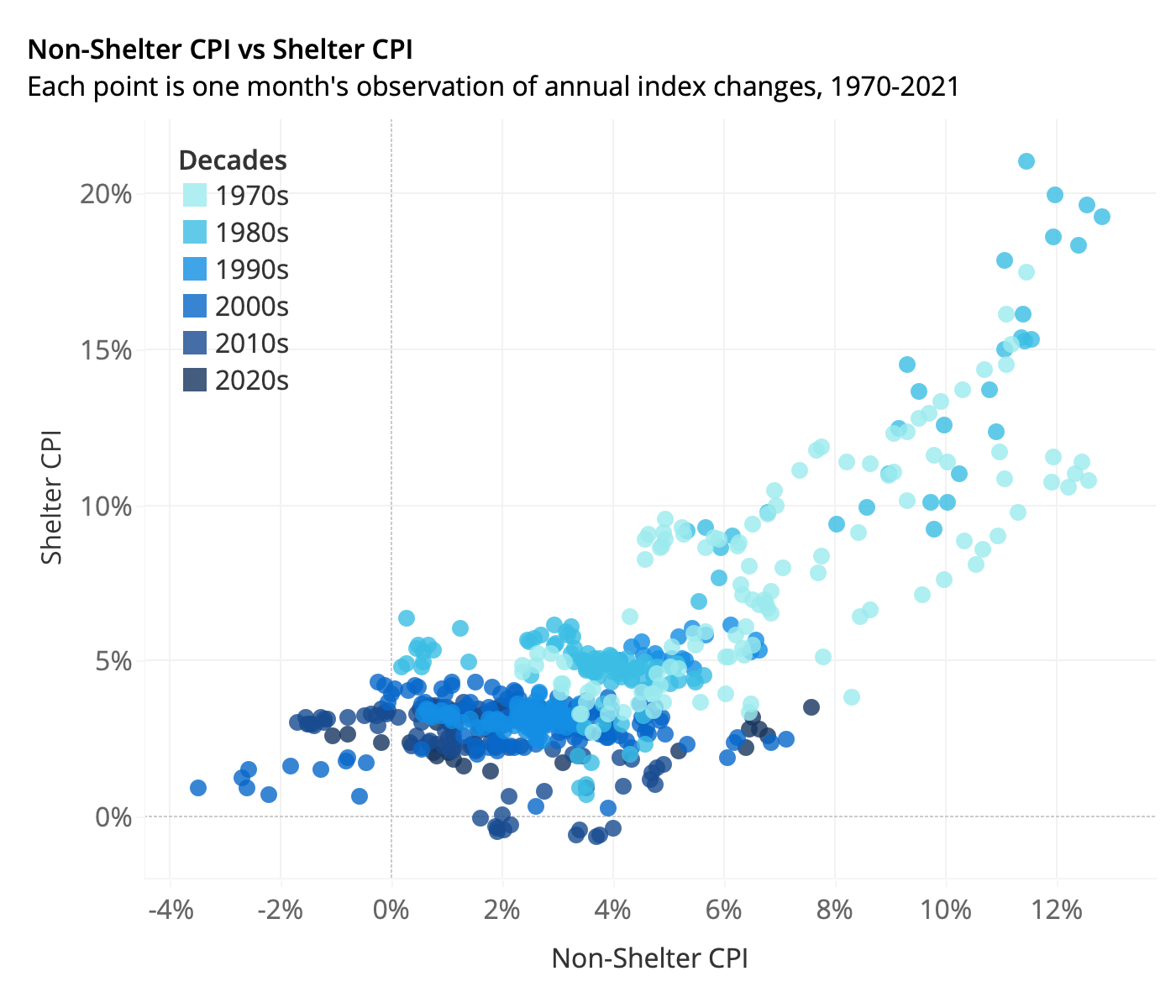

There is an imperfect but clear positive correlation between non-shelter and shelter CPI changes over the last 50 years:

In general, when non-shelter CPI growth exceeds 6%, shelter CPI growth also begins to climb. The relationship is best explained by the fact that most prices tend to rise under similar overall economic conditions: when the economy is running hot, or monetary policy is very accommodative, demand rises, pushing up prices across many categories, including housing.

That helps explain why this relationship is mostly only visible in the long run: demarcating the data by decade shows that most of the positive relationship is driven by the 1970s and 1980s, when inflation of all kinds was high. By comparison, recent decades have very little observable relationship between non-shelter and shelter price inflation.

There’s no clear economic answer for how consumer demand for housing will change in response to rising prices of other goods and services. But we do know that the change in demand for one good – housing, in this case – in response to rising prices on other goods can be broken into an income effect and a substitution effect.

The income effect captures the way that consumers will feel poorer, overall, as non-shelter prices rise: Someone spending an extra $100 per month on gas and groceries will have $100 less in their budget for mortgage or rent payments.

The substitution effect captures how people tend to shift spending away from costlier items toward more-affordable alternatives: Someone seeing airfare and hotel costs up 20% from last year might instead opt for a stay-cation this year – and redirect some of those savings toward a bigger or better home that makes a staycation more enjoyable. When non-shelter price inflation accelerates, the income effect tends to dampen housing demand, while the substitution effect actually intensifies it. The overall net effect is unclear, if everything else in the economy is not changing.

But if American household incomes are rising about as fast as non-shelter prices, then that would mostly cancel out the negative income effect and leave the positive substitution effect – boosting housing demand. That phenomenon might accurately characterize the movement of incomes and prices in 2020 and 2021, helping explain the rising demand for housing and, in turn, rapid home price appreciation over that same period.

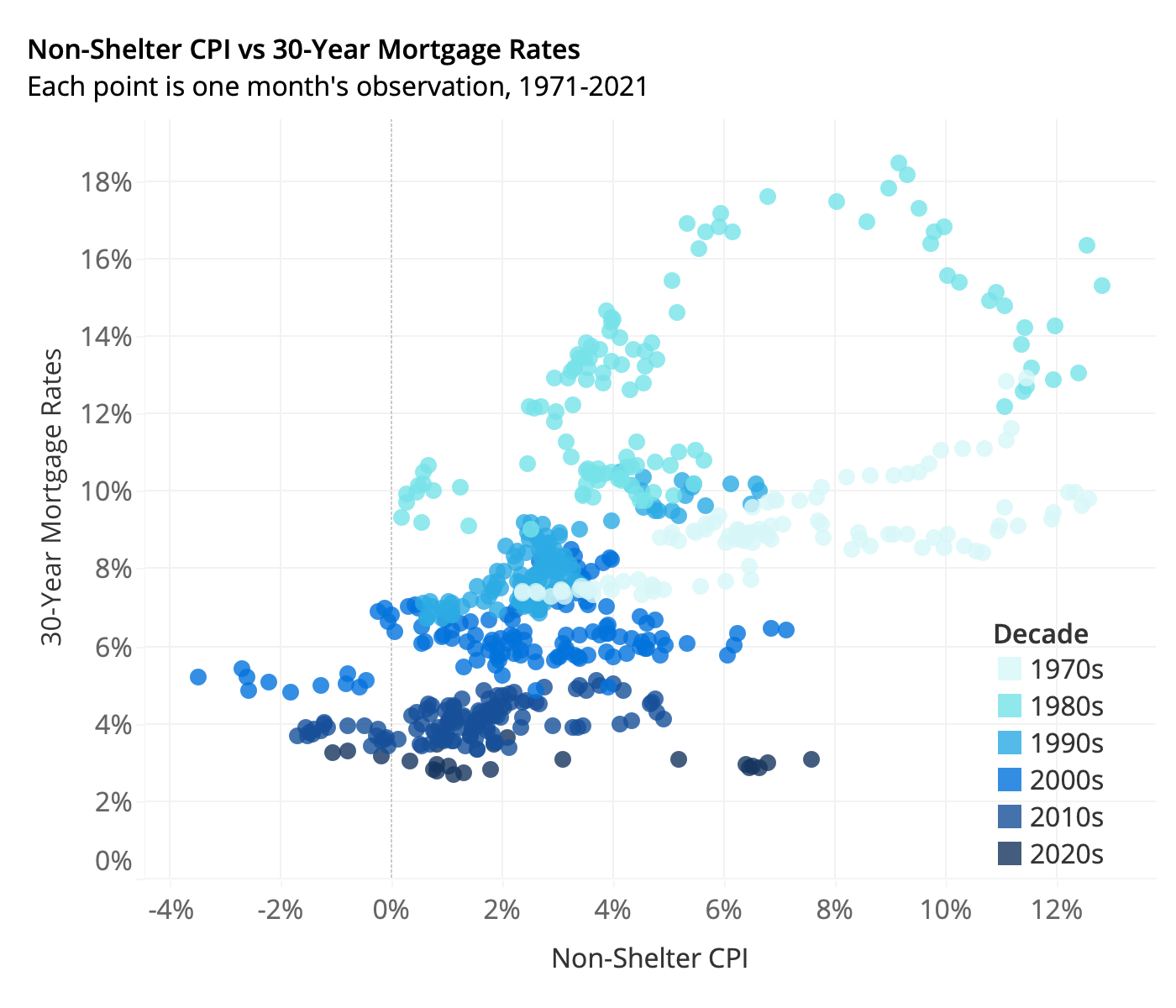

One more wrinkle to all this is that the cost of homeownership is determined in large part by the mortgage interest rates available to homebuyers and homeowners. Historically, higher non-shelter inflation tends to go hand-in-hand with higher mortgage rates.

Still, the two don’t move in lockstep, and there can be surprisingly long transitional periods in which inflation moves dramatically while mortgage rates do not. Now is one of those periods, representing a potentially golden opportunity of exceptionally low inflation-adjusted borrowing costs on mortgages. The annual rate of non-shelter inflation has accelerated more than 6 percentage points this year alone: from 1.3% in January 2021, to 7.6% in October 2021. Over the same period, the average interest rate on a 30-year mortgage has risen much more modestly: From 2.74% to 3.07%, or only one-third of one percentage point.

It makes sense that one year of inflation data would not completely rewrite people’s expectations far into the future, which 30-year mortgage rates are closer to reflecting. But even taking a market-implied future inflation rate, based on the ten-year Treasury Inflation-Protected Securities yields, shows that 30-year mortgage rates have not fully incorporated rising inflation expectations. The 10-year breakeven implied inflation rate derived from this market rose from an average of 2.08% in January, to 2.62% in October–that’s more than mortgage rates have risen! While acknowledging the difference between the 10- and 30-year horizons, these numbers suggest the real interest rate on mortgages (the actual nominal rate minus expected inflation) actually fell in 2021, from 0.66% in January to 0.45% by November: the lowest on record. This means that, so far, rising overall inflation has made the real cost of borrowing somewhat cheaper. There is no guarantee this trend will persist.

For now, the shrinking gap between mortgage rates and long-term expected inflation reflects the enticement of a long-term substitution effect. Prices on everything else are expected to rise over the next few decades, so the cost of borrowing money with a fixed-rate mortgage and locking in today’s housing prices over the longer term looks more and more attractive by comparison. That is one reason owning a home makes a good inflation hedge: Buying a home today with a fixed-rate mortgage locks in the purchase of a valuable service (a place to live!) at a fixed, nominal monthly cost – which will only get more attractive as most of the other things in life keep getting pricier.

Where will mortgage rates go from here? Most economists expect them to rise, not necessarily in direct response to inflation but rather because policymakers are tightening monetary policy in response to inflation. The interest rate on mortgages is largely determined by the forces of supply and demand in the market for mortgage-backed securities, in which one of the biggest buyers is the Federal Reserve. In response to both the improving job market and the threat of rising inflation, Federal Reserve Chairman Jerome Powell announced in November that the Fed would begin to reduce, or taper, the Fed’s monthly purchases of long-term Treasury bonds and mortgage-backed securities over the coming months. All else equal, the withdrawal of such a large buyer from the secondary mortgage market will tend to raise interest rates for borrowers.

{kind=link}