Rent Prices Soar Beyond Pre-Pandemic Projections (July 2021 Market Report)

Typical U.S. rent has pushed beyond where they are projected to have been if pre-pandemic trends had held.

Typical U.S. rent has pushed beyond where they are projected to have been if pre-pandemic trends had held.

Rents continued on a strong trajectory and have pushed beyond where they are projected to have been if pre-pandemic trends had held, according to the July 2021 Zillow Real Estate Market Report, erasing the small affordability gains renters made during the brief period of rent softening that ended this spring. And while U.S. home value appreciation again broke records in July, there are signs of a rebalancing in the for-sale market to come, with inventory rising for the third consecutive month and home value appreciation slowing in almost half of the nation’s largest markets.

Typical U.S. rents grew 9.2% year-over-year in July, according to the Zillow Observed Rent Index (ZORI) — the fastest recorded by Zillow records in data that reaches back through 2015 — to $1,843/month. Projecting forward historical ZORI values from February 2020 — the last full month before the COVID-19 pandemic hit the U.S. in earnest — we estimate that the U.S. ZORI in July was 2.9% ($52) higher than where it would have been if the last roughly 18 months had been more ‘normal.’

Rents first surpassed their pre-pandemic trajectory in June, recovering from a difference of -3% (-$55) at its lowest point last September. The stalled rental market from last spring through this past winter stood in sharp contrast to the still-strong for-sale market, but recent months of intense rental demand has caused rent growth to accelerate.

Rents in nine of the nation’s 50 largest metros — Tampa, Riverside, Las Vegas, Jacksonville, Memphis, Phoenix, Virginia Beach, Atlanta and Miami — are more than 10% higher than their projected rent levels for July based on pre-pandemic trends, topping out at 15.6% higher in Tampa. Only nine metros are yet to catch up with their projected levels, mainly concentrated in more-expensive coastal markets: Los Angeles, Washington D.C., Chicago, Minneapolis, Seattle, Boston, New York, San Francisco and San Jose. Even so, rents in New York, San Francisco, and San Jose were all up year-over-year, posting slight gains after more than a year of consecutive declines. While the recovery in these expensive markets has taken longer to take effect, their rebound has been strong — and accelerating — in recent months.

For-sale inventory, while still down 27.6% nationwide from a year ago, climbed 4.5% from June, the third straight month-month increase, and was higher than June in 47 of the top 50 markets. Inventory was up more than 10% month-month in Detroit, Buffalo and Cleveland, but remains down between 16% and 38% from last year in each of those markets. Inventory fell month-over-month in Boston, Raleigh, and Miami, and only three metros saw both positive month-over-month and year-over-year inventory — San Jose, San Francisco, and Washington D.C.

The typical U.S. home was worth $298,933 in July, with appreciation yet again setting records — up 16.7% year-over-year and 2% from June. Among the largest markets, Austin once again topped the charts with year-over-year growth landing at 41.5%. Even the nation’s slowest-growing metros are still appreciating at a double digit pace: New Orleans had the lowest year-over-year home value appreciation of any top 50 metro, at 11.6%.

However, there are signs the market may be nearing the peak of home price appreciation, as 22 of the top 50 metros had slower month-over-month growth in July than they did in June. As inventory continues to come onto the market and tip the scales more in favor of buyers, we will likely see moderation in home price growth coming in the near future. Nationwide and in all 50 of the largest metros, the share of for-sale listings that experienced a price cut increased from June, and in 47 metros and the U.S. as a whole the median time a home stayed on the market before selling stayed the same or increased from June. All signs point to the likelihood that the market is beginning to cool off.

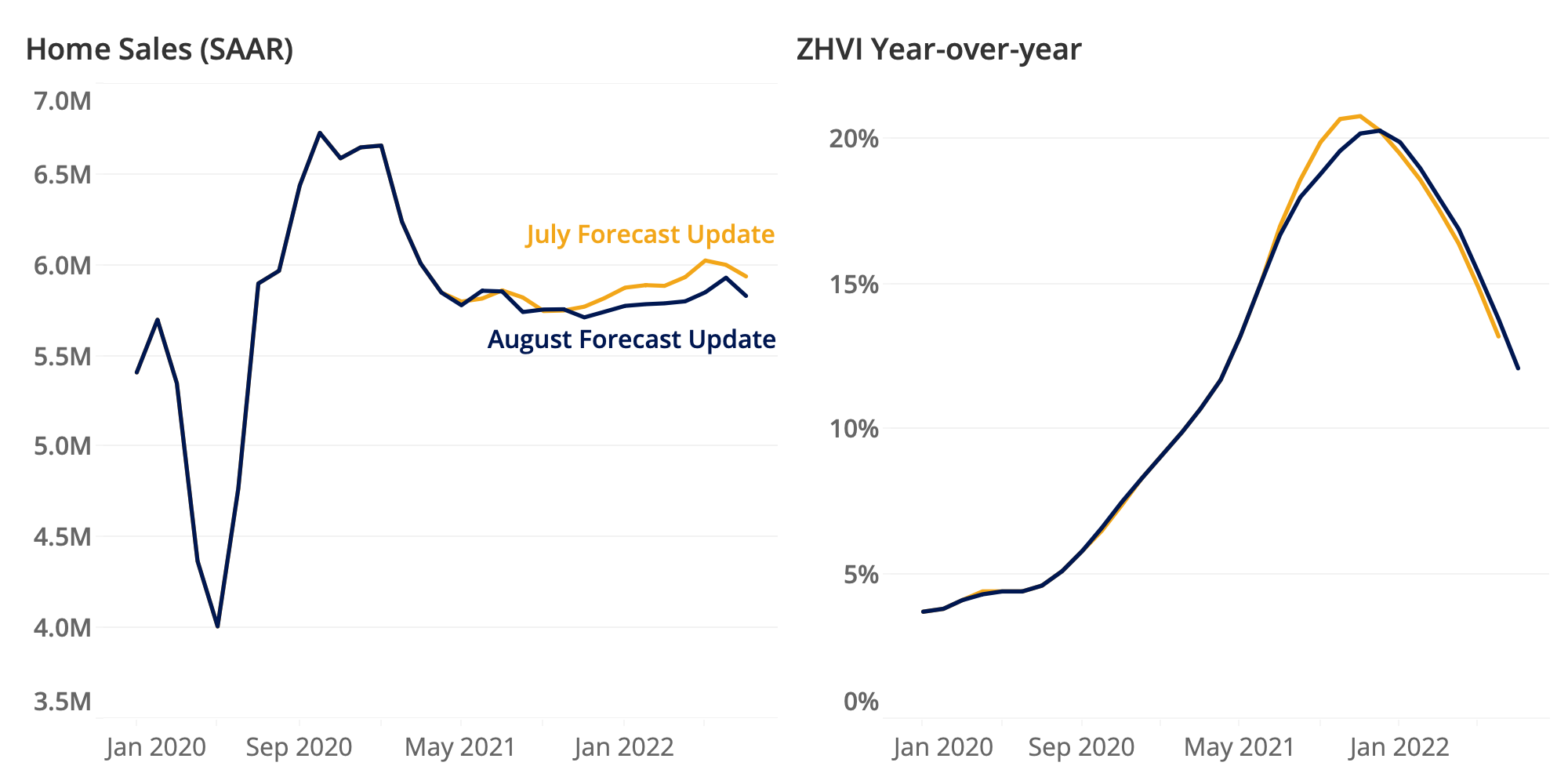

U.S. home value growth is expected to continue to accelerate through the end of 2021, before beginning to slow through summer 2022. The number of completed home sales nationwide this year is still expected to surpass 2020 levels, though slowed household formation may put a cap on potential sales growth.

Zillow economists expect home values to increase 5.2% over the next three months (July-October), by 8.1% through the end of this year (July-December) and by 12.1% through the twelve months ending in July 2022. The value of the typical U.S. home is expected to end 2021 up 20.3% from the end of 2020. The latest quarterly home value forecast is a downward revision from last month, when we expected 6.3% growth from June-September. The 12-month forecast has also been revised slightly downward from expectations of 13.3% growth between June 2021 and June 2022. The small downward revisions were influenced, in part, by the continued spread of COVID-19 and uncertainty posed by the impact of expiring forbearance programs. Zillow research shows the forbearance program has likely helped avoid a wave of costly foreclosures, and more inventory is expected to hit the market over the next few months as many borrowers exit forbearance and look to sell and capitalize on recent gains in equity.

Our expectations for existing home sales have also softened slightly compared to last month. Zillow expects a total of 5.89 million existing home sales in 2021, up 4.3% from 2020 (on its own the strongest year for existing home sales since 2006) but down from the 5.91 million total 2021 sales expected in our prior forecast. Recent declines in pending home sales volume outweighed what was otherwise a surprisingly strong June existing home sales report, and a continued slowdown in household formation also dented our longer-term outlook for sales.

Continued high inflation also factors into the home value appreciation outlook, presenting both upside and downside risks. On the upside, nominal home prices are likely to stay high with elevated inflation; on the downside, high inflation will put upward pressure on interest rates which can potentially dampen home purchase demand and home value appreciation.

{kind=link}