Mortgage Comparison Tool: A Glimpse at Life Without the 30-Year Fixed-Rate Mortgage

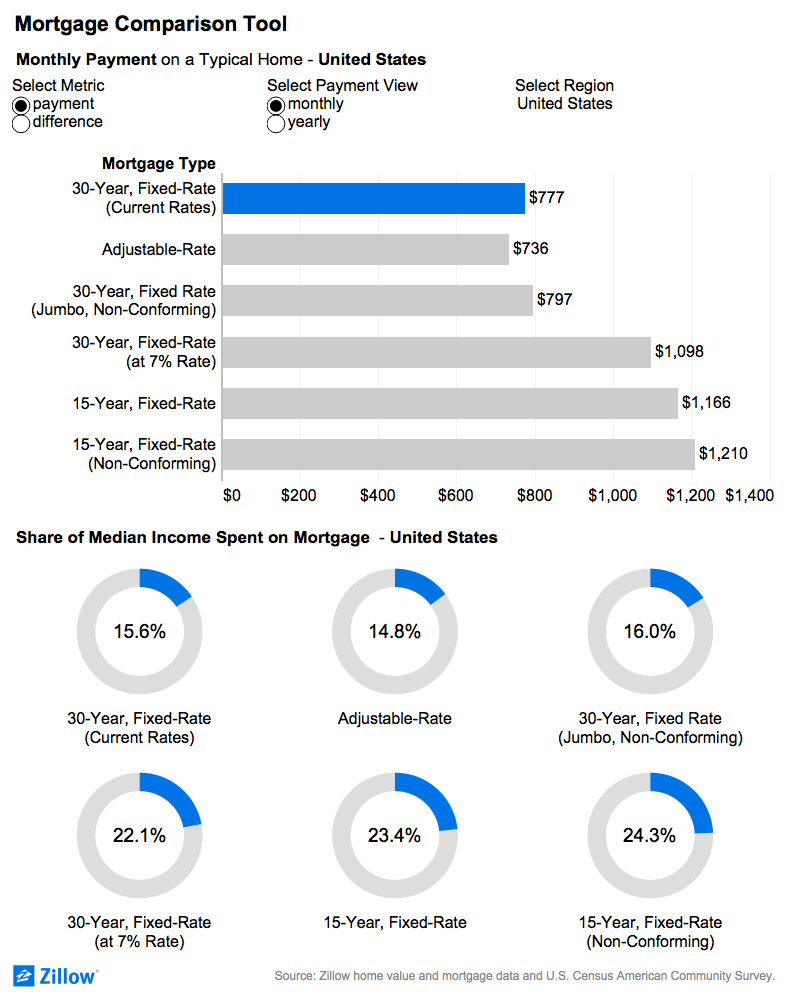

Hoping to reduce taxpayers’ risk, policymakers are considering changing the mortgage guarantee, which may lead to a shift toward adjustable-rate products, higher fixed interest rates and/or shorter-duration loans. Here's a comparison tool that shows how sensitive house payments are to changes in interest rates and loan duration.

As Congress contemplates a permanent fix to its decade-long “temporary” mortgage patch, the lore of the 30-year fixed-rate mortgage is permeating Capitol Hill.

Mortgage giants Fannie Mae and Freddie Mac (known as Government Sponsored Enterprises, or GSEs) don’t issue mortgages directly. Instead, they buy certain mortgages originated by other lenders and bundle them into mortgage-backed securities that are then sold to investors. Critically, these securities are guaranteed against default by Fannie and Freddie, protecting investors and making the securities more attractive. That guarantee enables long-term mortgage products like fixed, 30-year loans to be made widely available at lower rates.

But Fannie and Freddie have been under conservatorship of the federal government since 2008, which means those guarantees are largely backed by U.S. taxpayers, not private capital. Because Fannie and Freddie play such an outsized role in mortgage finance in this country, one of the longstanding legacies of the recession is that taxpayers today back a large majority of the nation’s mortgage market. Fears around the degree to which taxpayers would be on the hook if the market soured have kept Fannie and Freddie in Congress’ crosshairs.

Hoping to reduce taxpayers’ risk, policymakers are considering changing the guarantee, which may lead to a shift toward adjustable-rate products, higher fixed interest rates and/or shorter-duration loans. Those opposed to curtailing the government’s guarantee argue that without it, today’s 30-year fixed-rate mortgage could change drastically – to borrowers’ detriment.

What exactly would lending – and, critically, borrowers’ monthly costs – look like without the venerable 30-year, fixed-rate mortgage that has become the bedrock of housing finance? The Bureau of Labor Statistics estimates roughly seven in 10 mortgages held in 2014 were 30-year fixed-rate.

We don’t know what exact effects, if any, GSE reform might have on the 30-year mortgage. It’s possible any resulting dominant mortgage product would be wildly or only mildly different from what we have today. The figures in the comparison tool above provide a glimpse at mortgage alternatives and illustrate how sensitive house payments are to changes in interest rates and loan duration.

If monthly payments soar and stay elevated, at some point we’d expect home prices to fall in response to this decreased purchasing power. However, while some households may be able to absorb the extra borrowing cost, in the nearer term first time homebuyers or buyers on the margin could feel a real pinch as homeownership becomes less affordable.

{kind=link}