Uncategorized

March Home Sales Forecast: All Eyes on Inventory

It’s difficult to increase the number of home sales when there aren’t many homes available to buy, and constrained by limited inventory, home sales have struggled to rise over the past year. We don’t expect that trend to ease much in March, according to our March home sales forecast, setting up a potentially difficult spring shopping season for home buyers.

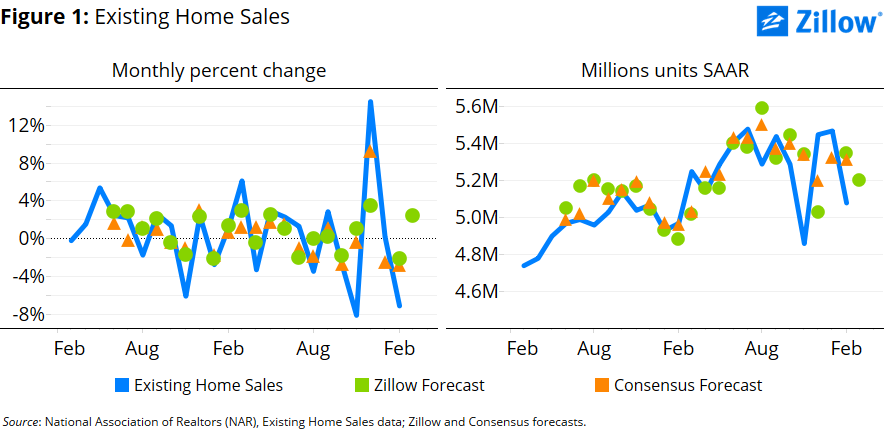

- Zillow expects existing home sales to increase 2.4 percent in March from February, to 5.2 million units at a seasonally adjusted annual rate (SAAR).

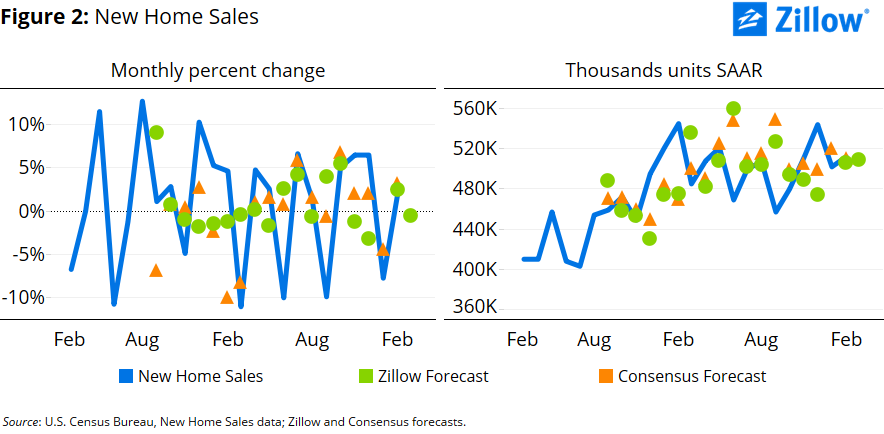

- New home sales should retreat 0.5 percent to 509,000 units (SAAR), remaining in the range where they have spent the past year.

It’s difficult to increase the number of home sales when there aren’t many homes available to buy, and constrained by limited inventory, home sales have struggled to rise over the past year. We don’t expect that trend to ease much in March, according to our March home sales forecast, setting up a potentially difficult spring shopping season for home buyers.

Both existing and new home sales have been essentially flat since mid-2015, with neither increasing for more than three months in a row since July 2014. Existing and new home sales have moved in opposite directions in six of the past seven months – a trend that last occurred in late 2013/early 2014, and has only occurred in 20 out of the past 199 months (roughly 16.5 years).

We expect this to continue in March, and forecast a 2.4 percent increase from February in existing home sales, to 5.2 million units at a seasonally adjusted annual rate (SAAR), and a 0.5 percent monthly decrease for new home sales to 509,000 units (SAAR).

An Inventory Story

Existing home sales fell sharply in February, according to the National Association of Realtors (NAR), with for-sale inventory lingering at near-decade lows. There were slightly more than 2 million (SAAR) homes for sale in February 2015 according to NAR, of which 1.8 million (89 percent) were single-family homes and the remainder were condos/coops.

Inventory of for-sale homes has held steady between 2 million and 2.2 million units (SAAR) since early 2013, near levels last seen between 1999 and 2001, despite a 13 percent increase in the number of households nationwide over the past 16 years. Scaled by the number of households, there are currently just over 17 existing homes on the market for every 1,000 households, compared with roughly 18-19 homes for sale per 1,000 households that prevailed in the late 1990s and early 2000s.

Looking only at single-family homes, for which a longer history is available, there are currently just over 15 single-family homes on the market for every 1,000 households – a number that has been roughly steady over the past three years, but is well below historic levels. In the early 1980s, there were 25-30 single-family homes for sale for every 1,000 households and in the mid-1990s, there were about 20.

Existing Home Sales: Widening Regional Chasm?

For much of the second half of 2015, existing home sales hovered around 5.4 million units (SAAR) – November’s regulatory-driven decline aside. February data put sales on par with levels observed in late 2014 and early 2015. Even with the expected monthly increase, existing home sales should end March about 0.9 percent below where they stood in March 2015 (figure 1).

The nationwide median price of an existing home sold in February fell 2.2 percent to $225,700, the largest month-over-month percent drop since May 2010, but there were wide regional differences: prices were down in South, Midwest and Northeast but up sharply in the West. In March we expect U.S. existing home prices to edge higher, to $225,800, putting them up 3.9 percent year-over-year.

The nationwide median price of an existing home sold in February fell 2.2 percent to $225,700, the largest month-over-month percent drop since May 2010, but there were wide regional differences: prices were down in South, Midwest and Northeast but up sharply in the West. In March we expect U.S. existing home prices to edge higher, to $225,800, putting them up 3.9 percent year-over-year.

Two price points merit particular attention: The median sale price in the West and the median sale price for existing homes in the South. Prices in urban markets in the West have been trending steadily upward at the same time as concerns are rising around some urban markets in the South sensitive to slowing foreign purchases (e.g., Miami) or energy-industry employment losses associated with low oil prices (e.g., Houston). A continued divergence in sales prices between the West and the rest, particularly amid potential slowing in some Southern markets, will reinforce the widening chasm in regional housing markets.

New Home Sales: Potentially Promising Signs

New home sales increased 2 percent in February to 512,000 units (SAAR), according to the Census Bureau, in line with expectations. And in a potentially promising signal for buyers, the inventory of new homes for sale reached its highest level since October 2009, although it remains well below historic norms. Our forecast suggests that new home sales should edge down in March, to 509,000 units (SAAR) (figure 2), and points to a steady monthly increase in the median price of new homes sold, from $299,000 to $309,900.

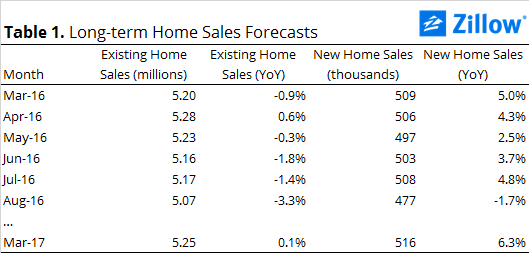

Our long-term forecasts (table 1) suggest relatively flat home sales over the next year.

Our long-term forecasts (table 1) suggest relatively flat home sales over the next year.

{kind=link}