How a Faster Market Enabled More Home Sales in 2020, Despite Falling Inventory

- In 2020, a higher velocity of sales (lower days on market) helped the U.S. housing market transition to both higher sales volumes and lower inventory levels.

- This low level of inventory could persist as a “new normal” if time on market remains so low.

The housing market in 2020, especially the latter half of the year, was defined by two seemingly contradictory forces: The number of closed home sales soared, even as overall inventory — the standing pool of homes actually available to buy — plummeted. The deciding factor allowing both of these to be true was a drastic acceleration in the speed of the market itself, with buyers snapping up newly listed homes just days after they hit the market.

It’s a trend that, should it hold, could reset traditional understandings of what “normal” inventory levels look like.

Overall, 2020 was an incredibly challenging year for the broader economy — but the fact that housing emerged as an indisputable success story proves just how flexible the housing market can be even as conditions rapidly change. Consumers can adjust and act more quickly, technology can enable more efficient connections between sellers and buyers and the market can thrive in previously unimagined ways.

Still, there are some practical rules that can’t be broken. No matter how efficient the process is, all buyers need at least some time to discover and decide on a home to purchase. And there are potential limits to how many sales can occur if new inventory doesn’t hit the market at some minimum level. But our data suggest the market is not yet approaching this minimum, and that overall inventory can in fact fall farther, time on market can continue to shrink and sales can continue to grow as long as new listings keep coming on line as they have in recent months.

Lean Logistics

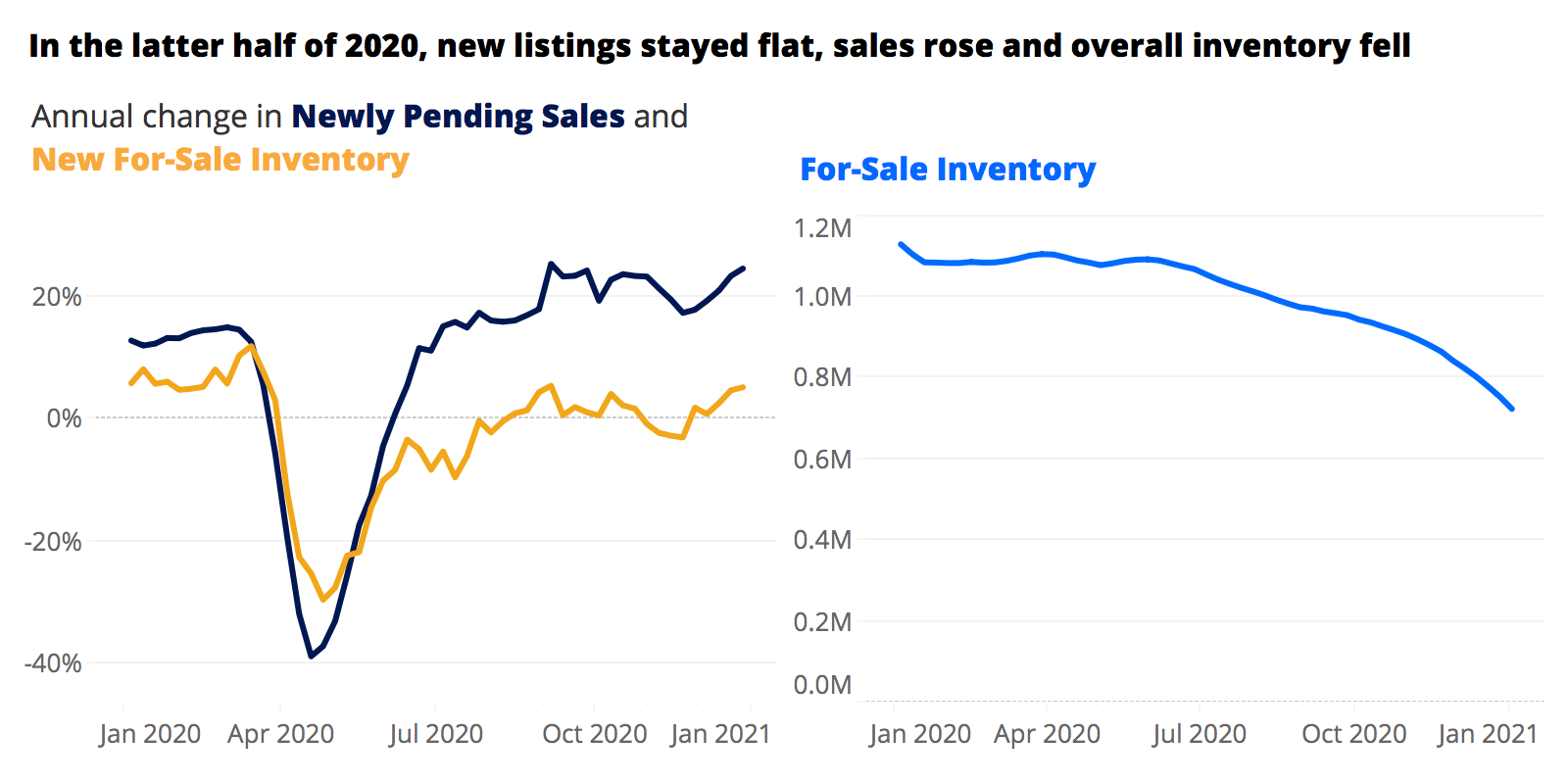

So how did we get here? The number of homes available to buy, the number of home sales that can ultimately occur and the amount of time homes spend on the market before selling are all interconnected. In the latter half of 2020, the flow of new listings hitting the market remained broadly similar to 2019 levels, the speed of sales increased (the time a home spent on the market before selling decreased) and the number of sales increased — which, when combined, served to reduce the overall level of inventory. In more detail:

- New listings remained constant: Throughout the second half of 2020, new listings were neither meaningfully up nor down in any week (ranging between -10% and +10% from 2019 levels). The total number of new listings in the second half of 2020 was almost identical to the total in the second half of 2019.

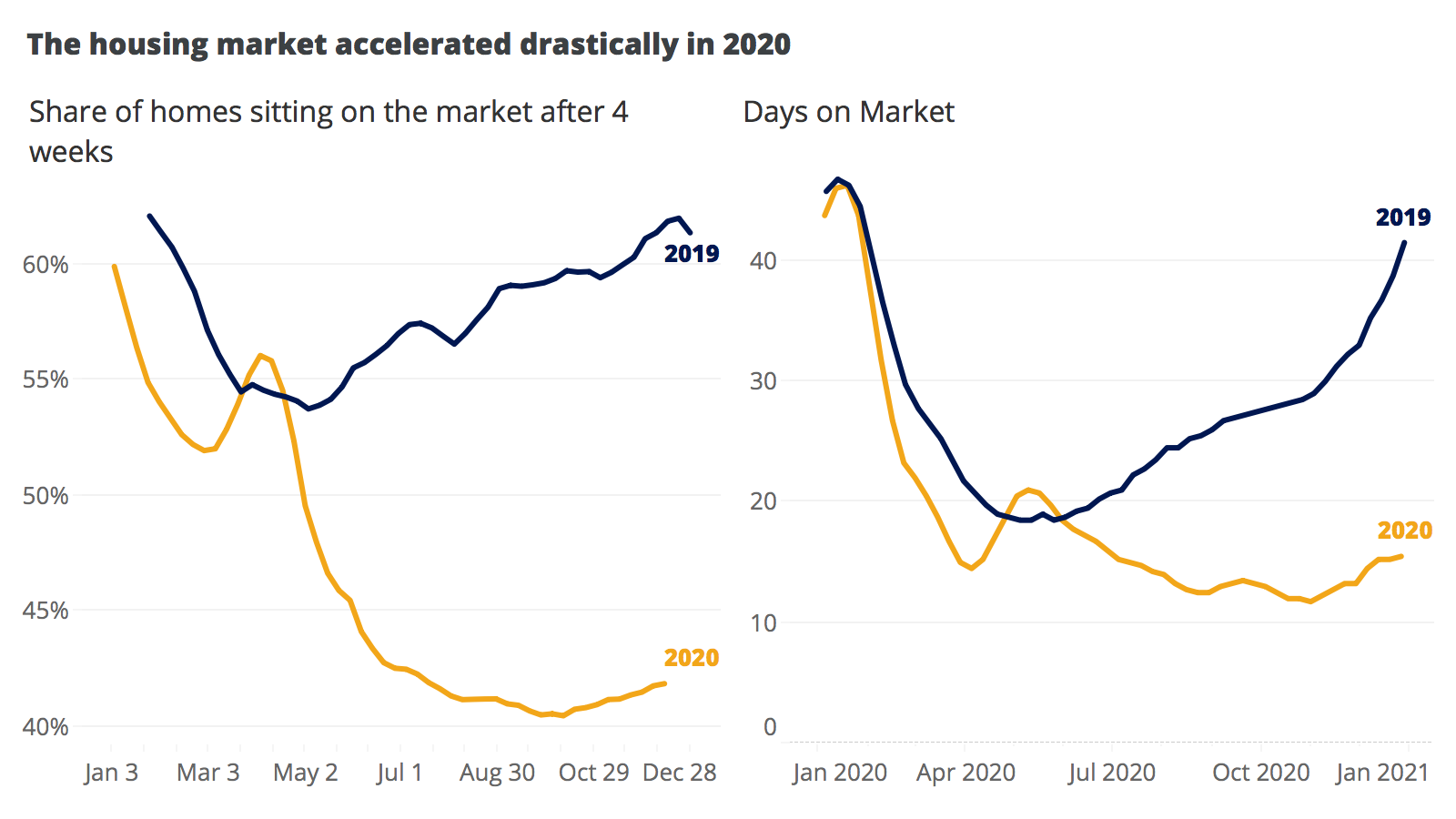

- Velocity increased: Homes sold much faster than they did in 2019, and the gap widened as the year went on. In June 2020, homes were on the market a median of 16 days, down from 21 in June 2019. By December, time on market was 17 days — almost a full month (25 days) faster than the same time in 2019.

- Sales increased: Newly pending sales — transactions that are under agreement but not yet closed, often used as a more timely indicator for closed sales to come — were higher than 2019 levels every week. In total, there were 20% more pending sales in the second half of 2020 than in the second half of 2019. Overall, existing home sales volumes ended 2020 up 5.6% from 2019 — despite a weeks-long, pandemic-related pause in the Spring.

- Overall inventory decreased: The inventory gap between 2020 levels and 2019 levels — already wide to start the year — only widened as the year progressed: At the end of June, total inventory was 21% below levels from June 2019. By the end of December, total inventory was down 35% year-over-year.

Like a warehouse transitioning to just-in-time inventory management, the U.S. housing market became more streamlined in 2020, with typical home sales occurring much more quickly after initially being listed. And because homes were on the market for so much less time before selling, there was a much smaller stockpile of listed homes observed at any given point in time — what we refer to as inventory.

Homes are also selling incredibly quickly at a time of year when the market generally slows down as the weather cools and people take time off for the holidays. The typical home that sold in the week before Christmas 2019 was on the market for 39 days. In the same week in 2020, the typical sold home was on the market for just 16 days. Put another way: A majority (60%) of homes listed for sale in the first week of November 2019 were still on the market by the end of that month. In 2020, less than half (~40%) of homes listed for sale in the first week of November were still on the market at the end of the month.

Markets Move Differently

Logically, the number of pending sales (plus other de-listings) cannot forever exceed the number of new listings: Eventually, if this imbalance continues, it would drive overall inventory down to 0. Practically speaking, this isn’t going to happen — it’s virtually unimaginable for the pool of inventory to shrink to 0 and for sales levels to be limited to no larger than the number of incoming new listings. But there IS a floor for how low inventory/new listings/time on market can get before further sales growth becomes practically impossible, given our current conditions.

On the ground, there is a limit to how fast a home can sell. Technological innovations, in particular, have brought the market much closer to perfect efficiency, including better search tools, better agent/client relationship management tools and streamlined/online closing processes. Even so, it’s unreasonable to expect that a meaningful number of homes will be listed, get in front of an interested buyer with the appropriate budget, and have an offer made and accepted all within a single day. It’s possible, and certainly does happen in some cases, but it’s rare.

Still, the median time on market has fallen to extremely low levels in some areas over the past few years, offering some useful guidance for how fast markets can move and how low inventory could get without having an impact on sales volume. At times last year, median time on market in a handful of Ohio markets fell to as low as 4 days from initial listing to pending, and the speed of the market in the Bay Area was similarly lightning-quick at various points. But every market is very different, and the local home search process varies drastically. In New York, for example, the median time on market fell to 28 days at times this fall — positively glacial compared to Cincinnati or San Francisco, but still half the local pace from a year ago and a record-low for New York. The New York market just moves differently than others.

A Lower Bound on Inventory

But just how low can inventory go without impacting sales volumes? We saw in 2020 that inventory could fall for months on end without smothering sales, thanks to homes selling more quickly after being listed. So in essence, the question of how low inventory can go, consistent with current sales volumes, is another way of asking “how fast can homes sell?”

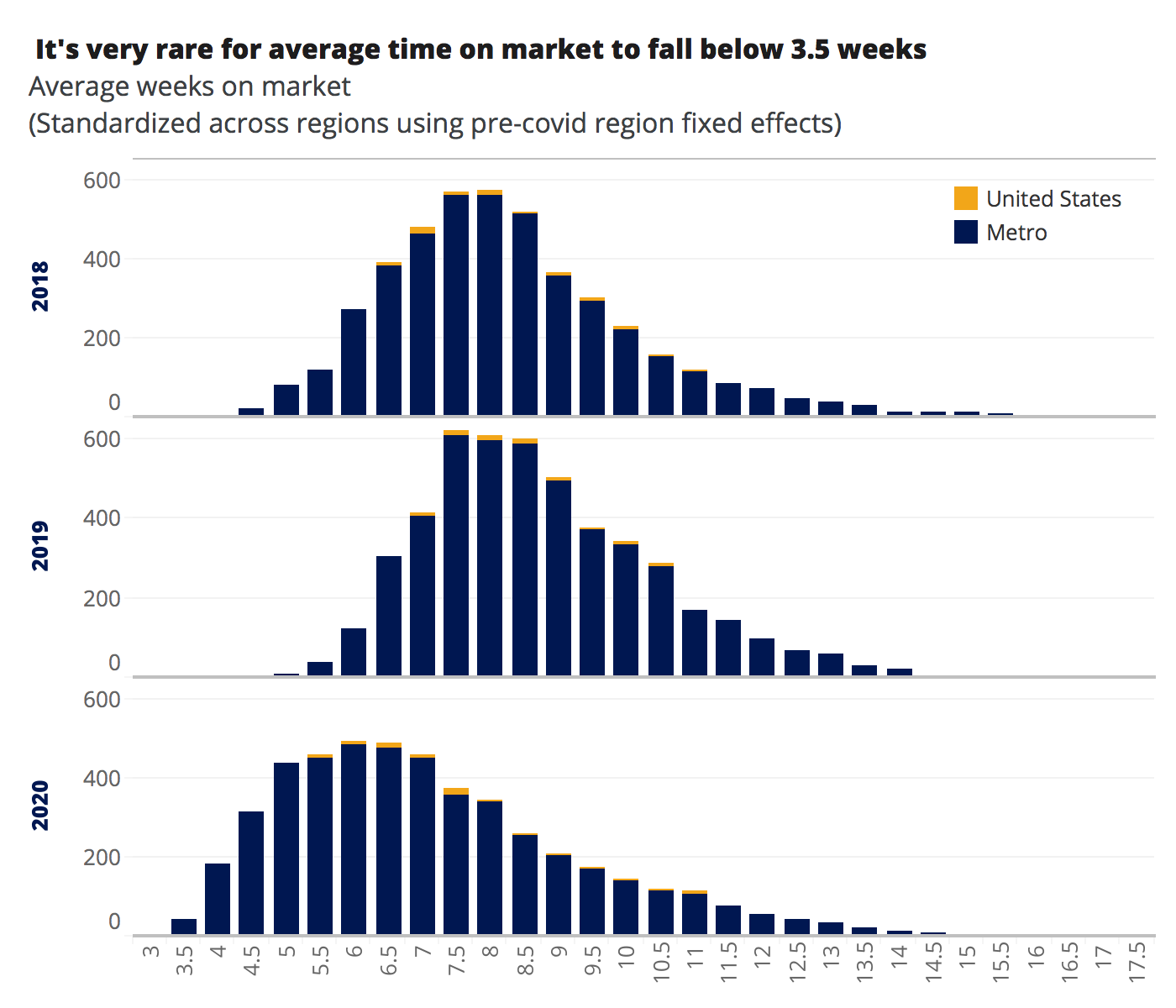

Average days on market (the relevant measure of sales speed) has varied widely between markets in recent years, but when we chart the data they reveal a seemingly hard lower limit at roughly 3.5 weeks.[1] At least under the current reality, it is just vanishingly rare for any market to break through that floor.

To translate that into inventory, multiply the weekly flow of new listings observed last year by that 3.5 week figure, and you get a rock-bottom minimum inventory of about 275,000 in the winter, or about 525,000 in the summer, beyond which further growth in sales volumes would likely become incredibly difficult. Compared to current (as of early 2021) levels of about 725,000 listings, this suggests inventory is not yet close to this theoretical lower limit.

In the rare cases where average time on market did approach the 3.5-week “limit,” sales volume did not subsequently decrease. Instead, at that point the flow of new listings came into equilibrium with the outflow of sales, likely thanks to the strong price appreciation helping pull more sellers out of the woodwork seeking to capitalize on recent, rapid gains in equity.

Further sales growth will depend both on a steady flow of new inventory and continued strong demand, both of which are expected through the coming year. Sellers are expected to overcome COVID-related anxiety as vaccine rollouts continue, and list homes in greater numbers. And continued gains in equity are likely to pull still more sellers off the sidelines as the look to turn paper gains in wealth into more-tangible returns. Buyers will continue to enter the market as they age, re-consider their housing needs and/or seek to take advantage of low mortgage interest rates.

A New Normal?

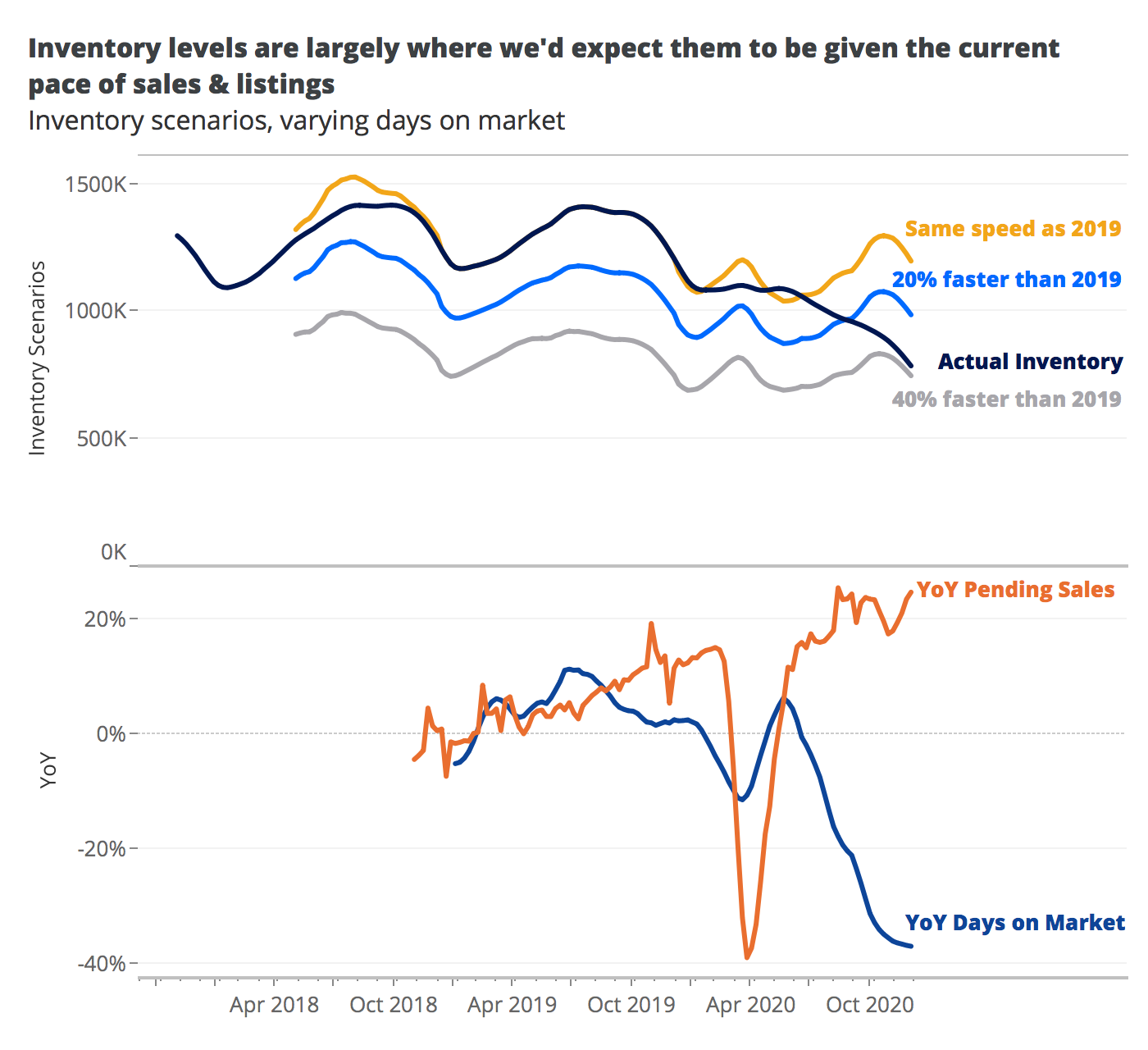

Finally, in some respects, inventory itself is not far off from where we would expect it to be given the currently rapid pace of home transactions. Combining observed time on market with weekly data on new listings, we can compute 3 scenarios for how inventory levels might have evolved if time on market matched the seasonal patterns of 2019, or if it were 20% or 40% faster than the speeds observed in 2019.

Actual inventory began 2020 exactly where we would expect if time on market had followed 2019 trends. Inventory then got dislocated by initial pandemic shutdowns in the early-mid Spring, and turned decisively downward beginning July 1. Two months later, it passed through the “20% faster” scenario and almost reached the “40% faster” scenario. And because pending sales are still outnumbering new listings, inventory continues to fall. But what this shows is that current U.S. inventory levels largely can be sustained as the new steady state/new normal, assuming the flow of listings rises to balance the current pace of pending sales and as long as sale speeds remain close to 40% faster than in 2019.

Where will the market go from here?

The current inventory and sales situation is like the emergency oxygen mask on a modern airliner — the flow of oxygen will be sufficient, even if the bag does not appear to fully inflate. In 2020, faster pending sales helped the U.S. housing market transition to a lower inventory level — now down more than a third when measured on a weekly basis — and maintain consistently higher sales volumes. And in 2021, it is entirely possible that time on market and inventory levels will keep falling even farther below pre-pandemic levels.

But at some point, these measures are likely to level off. The trailing-12-month sum of new listings reached 7.1 million before the lockdown, and it could reach or exceed that level by the end of home shopping season this year. If that greater flow of new listings matches the current, greater sales volumes, inventory could remain at low levels concurrently with high sales volumes for the foreseeable future, so long as time on market remains low.

[1]That pace may seem slow, because it is much higher than median time on market. But in this case, the average is important, because — particularly in fast-moving markets where competitively-priced homes often go under contract within a week — the long tail of unsold homes lingering for months on end will exert an especially strong upward pull on the average.