We know that homes near military bases – those most convenient for America’s military members and their families to buy or rent – are more valuable than homes overall. But how affordable are those homes on a typical enlisted soldier’s or sailor’s salary?

As it turns out, not very. And while most servicemen and women are already fighting an uphill battle against housing costs overall, depending where they’re stationed, that uphill battle could turn into a losing battle fairly quickly.

Military members are paid according to rank and experience, and they also receive a Basic Allowance for Housing[1] if they live off base. The goal of this allowance is to provide an equal standard of living for a soldier no matter where they are stationed. But our analysis reveals that while this allowance definitely helps military members better afford off-base housing, it does not accomplish its goal of providing an equal standard of living from base-to-base.

Branching Out

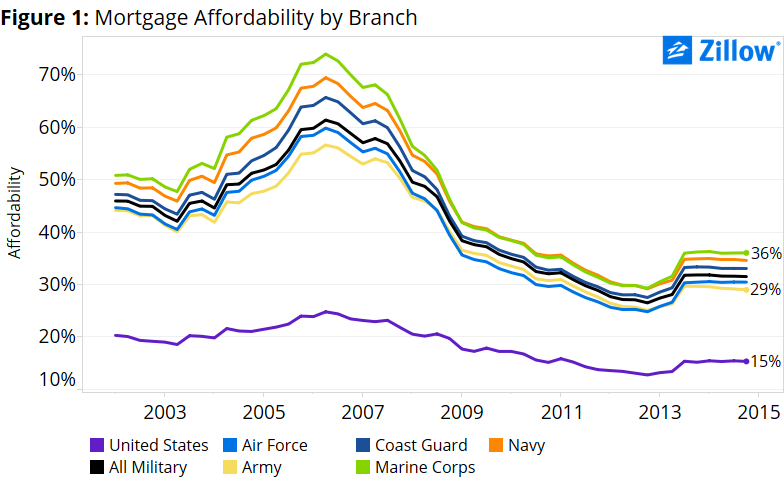

Nationwide, soldiers should expect to pay 31.5 percent of their income on a mortgage for a home near a military base, more than double the share their civilian counterparts should currently expect to pay. But this figure varies widely, depending on which branch a military member serves.

Nationally, a marine should expect to pay 36 percent of his or her income on a mortgage, 5.5 percentage points more than the overall military average. The navy is not far behind, with a typical sailor paying 34.6 percent of his or her income on a mortgage (figure 1). This makes sense, as naval bases and marine camps are – more likely than not – near the water, where homes command a premium over more inland locations.

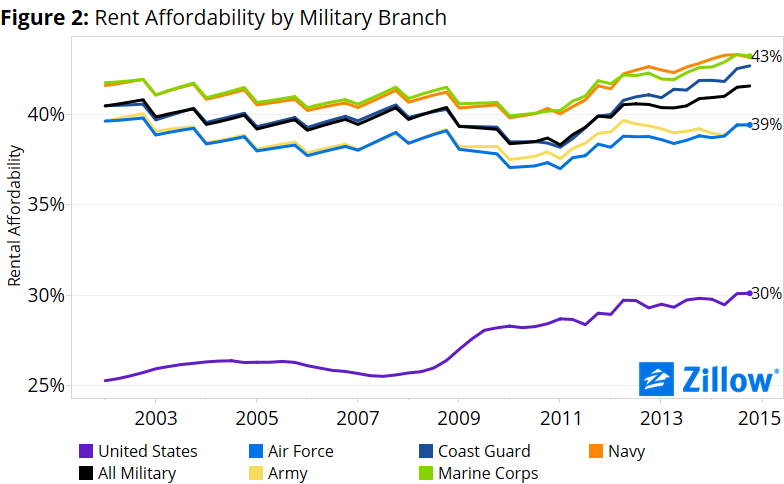

But not all soldiers and sailors buy a home. Military members not only need to move sometimes with very little notice, they also move very frequently. As such, the flexibility of renting a home instead of buying it can be a big advantage. But there is a trade off. Nationally, renting a home is less affordable than buying a home and paying a mortgage, and that holds true for homes near military bases.

Military members across all armed services should expect to pay 41.6 percent of their income on rent. But again, that figure differs among the various branches, with marines and sailors again expected to dig deeper into their wallets. Navy renters and marines should both expect to pay 43.2 percent of their income on rent (figure 2).

Different Terrain

Military members have little choice over where they’re stationed. And the primary law of real estate – location, location, location – applies equally to military members and civilians alike (figure 3).

Those stationed at any of San Diego’s myriad military facilities, for example, face a particularly dire situation. Military members stationed in San Diego and living off-base should expect to pay 65.5 percent of their income towards a mortgage, and 59.6 percent of their income toward rent.

In contrast, military personnel stationed at Fort Hood in Texas should expect to pay only 15.1 percent of their income towards a mortgage, and only 29.1 percent of their income towards rent – both very much in line with national averages.

Affordability isn’t pretty for military members and would look even worse without the Basic Allowance for Housing. But while this stipend does help overall, when it comes to the goal of providing an equal standard of living for all military members, no matter where they live, it clearly falls short. But there is a silver lining, however small. Uncle Sam does provide a number of benefits for those who serve, including access to commissaries and free or greatly discounted healthcare, which could help them stretch their housing dollar a little farther than their civilian counterparts.

Methodology

In order to produce an affordability index for typical military members, we pulled income for enlisted personnel paid at the E-4[2] paygrade, the military’s most common. We then integrated the Basic Allowance for Housing, which is adjusted by market, in order to get a more realistic view of affordability near each base. To construct a national series, we used weights calculated using five-year, 2013 American Community Survey data based on off-base areas where servicemen and women are most likely to live. We then aggregated this data to create nationally representative numbers for each branch of the military. In order to estimate mortgage affordability, we assumed the military member took out a loan backed by the U.S. Department of Veterans Affairs (VA), and put 0 percent down.

[1] In this analysis, the Basic Allowance for housing – which is adjusted each year – was smoothed using a 12-month trailing average.

[2] E-4 with four or more years of experience and dependents.