This post is part two of a three-part series on now-casting the MBA Weekly Mortgage Applications Index. To read more on this subject, see the summary, part one and part three.

In part one, we used percent change in loan requests on Zillow between Sunday and Friday to “now-cast” the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Index for the same week. Since MBA publishes its index each Wednesday with data corresponding to the previous week, Zillow data can provide a signal about the direction of the index several days in advance. In this analysis, we discuss using shorter, intra-week Zillow data to now-cast the MBA series and provide an even earlier signal about the current state of the economy.

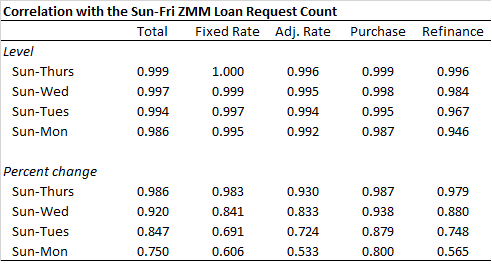

The stronger the correlation between the full-week and the partial-week Zillow data, the more reliable the signal from the shorter, intra-week data. As the table below illustrates, there is a very strong correlation between the number of Zillow loan requests on Sunday through Friday of a given week, and the number of requests for shorter intervals in the same week over the period June 2011 through March 2014. Although still strong, the correlations weaken somewhat for the percent change series, most notably for the adjustable rate and refinance series. Nevertheless, for all five series, the week-on-week percent change in the Sunday through Wednesday counts have upwards of 80 percent correlations with the week-on-week percent change in the Sunday through Friday counts.

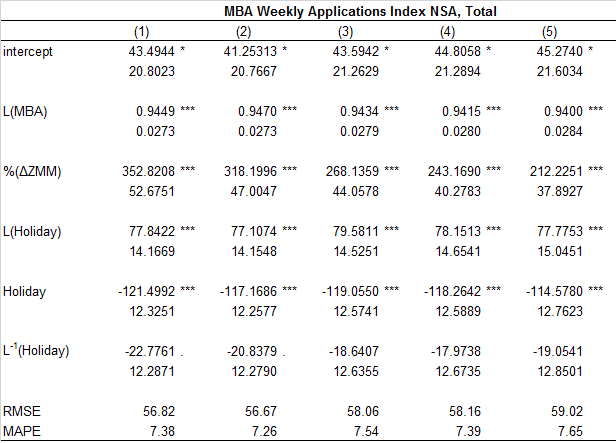

Previously, we determined that we best forecast the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Index level using a lagged value of the index, the contemporaneous percent change in Zillow loan requests, and an indicator of whether a U.S. banking holiday occurred in the week preceding, of, or following the forecast week. Below, we re-estimate the same model but replace the percent change in Zillow loan requests for the full week with the percent change in Zillow loan requests for the partial week (e.g., Sunday through Wednesday).

The results show that, in general, the now-casts for all partial-week Zillow samples perform roughly similarly. On average, the Root Mean Squared Error (RMSE) of the forecast, a standard measure to illustrate how far off our predictions are from the observed values, increases by 4.5 percent when moving from the Sunday-through-Thursday Zillow sample to the Sunday-through-Monday sample, and increases by an average of 5.9 percent between the worst-performing and best-performing intra-week samples.

From a practical perspective, and since the errors are similar across the various intra-week samples, using the percent change in Zillow loan requests between Sunday and Tuesday to now-cast the MBA index would appear to make most sense. Since our model relies heavily on a lagged value of the MBA index, which is released on Wednesday morning, we can use that data in addition to the count of Zillow loan requests through the previous evening to forecast the current weekly value and publish an estimate on Wednesday.

Detailed Methodology

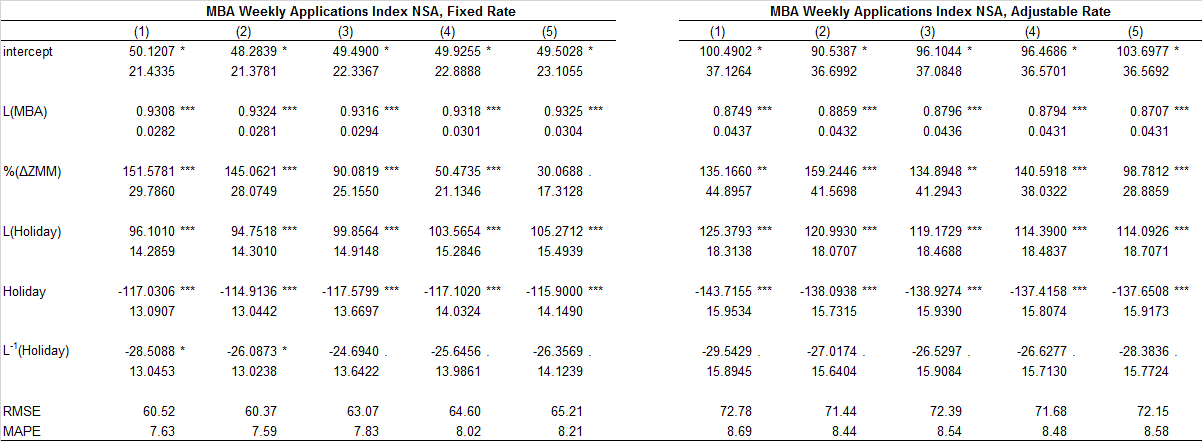

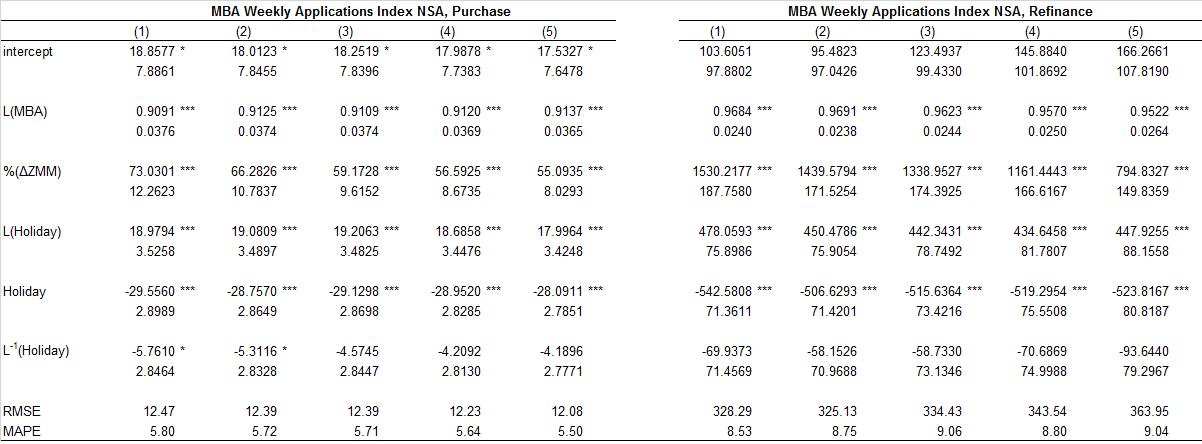

We model the non-seasonally adjusted Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Index level as a function of a lagged value of the index, the contemporaneous percent change in ZMM loan requests, and a series of indicator variables taking the value of one if a U.S. banking holiday occurred in the week preceding, of, or following the forecast week. This is equivalent to model (4), which was identified as the best performing forecast in the previous analysis.

The tables below show the results of this exercise. Model (1) uses the weekly percent change in ZMM loan requests for Sunday through Friday, model (2) uses the percent change for Sunday through Thursday, model (3) uses the percent change for Sunday through Wednesday, model (4) uses the percent change for Sunday through Tuesday, and model (5) uses the percent change for Sunday through Monday.

For the most part, the percent change in ZMM loan requests remains strongly significant across all intra-week samples. The forecast generally deteriorates as the length of the intra-week sample shortens, although for most indexes, the Sunday through Thursday data seem to perform best. A notable exception is the purchase index forecast which improves as the intra-week sample shortens with the percent change in Sunday through Monday ZMM loan requests producing the best forecast. However, in general the forecasts for all intra-week ZMM samples perform roughly similarly. On average, the Root Mean Squared Error (RMSE) of the forecast increases by 4.5 percent when moving from the Sunday through Thursday ZMM sample to the Sunday through Monday sample, and increases by an average of 5.9 percent between the worst-performing and best-performing ZMM samples.