Q2 2015 Negative Equity: Improvement at the Bottom, Condo-Owners More Impacted

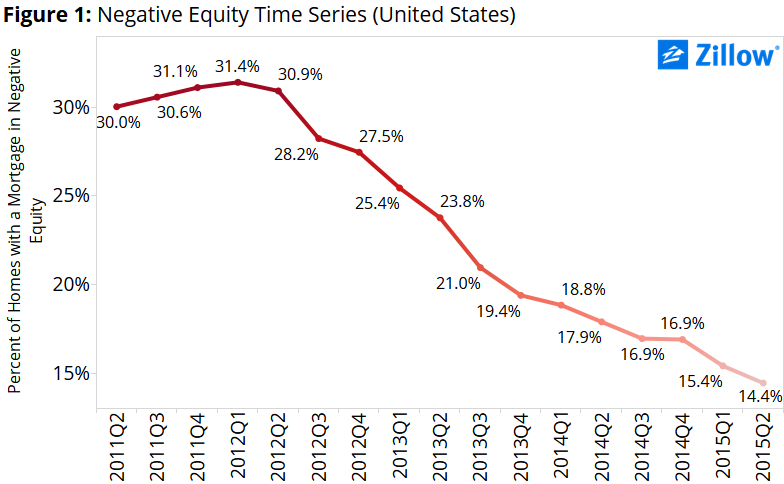

Nationally, the negative equity rate continued to fall in 2015 Q2 to 14.4 percent of homeowners with a mortgage, down from 15.4 percent in Q1 and 17.9 percent in Q2 2014. The fall marks the 13th straight quarter in which negative equity fell or stayed flat from the quarter prior.

Halfway through 2015, the share of homeowners with a mortgage was less than half it was at its early 2012 peak of 31.4 percent (figure 1). More than 8.3 million homeowners have been freed from negative equity since its peak.

Halfway through 2015, the share of homeowners with a mortgage was less than half it was at its early 2012 peak of 31.4 percent (figure 1). More than 8.3 million homeowners have been freed from negative equity since its peak.

Still, almost one third (31.4 percent) of homeowners with a mortgage are in so-called “effective negative equity,” lacking enough equity to sell their home, pay closing costs and afford a down payment on an equivalent or more expensive home (figure 2).

Owners of homes valued in the bottom third of home values tend to have higher rates of negative equity. Nationally, 24 percent of homes in the bottom third of home values are underwater, vs. 8.1 percent of homes in the top third. But because of strong home value appreciation among bottom-tier homes in the second quarter, many areas have seen significant declines in negative equity in the bottom tier.

Additionally, condo-owners are more likely to be underwater than owners of single-family homes. In Q2, 19.3 percent of condo-owners with a mortgage were underwater, compared to 14 percent of single-family home owners. This is partially attributable to the fact that condos are often less expensive and valued among the bottom tier of homes – nationally, roughly 50 percent of all condos are in the bottom tier. Also, condos were harder hit during the housing recession. Condos lost 34.5 percent of their value from the time the market peaked until it bottomed out, while single-family residences lost 20.6 percent.

Since peaking in Q1 2012 at 31.4 percent, the U.S. negative equity rate fell consistently for 10 straight quarters, before stalling in Q4 2014. The negative equity rate was flat at 16.9 percent in both Q3 2014 and Q4, before resuming its fall this year. Part of this was brought on by home value declines in the very bottom of the home value distribution. Some metros saw the bottom 10 percent of homes actually lose value, keeping negative equity rates flat or even rising among these homes, even as negative equity overall continued to fall.

Growth in home values has been consistently slowing since mid-2013, which has had ripple effects throughout the housing economy. Compared to the past year, in which home values grew nationally at a 3.4 percent annual pace, Zillow expects home values to grow 2.4 percent from June 2015 to June 2016. Because home values are appreciating at a slower pace, homeowners in negative equity will have to wait longer for home value appreciation alone to pull them back above water.

Negative equity varies considerably from city-to-city and region-to-region (figure 3).

The Southwest, Southeast and parts of the Midwest continue to be plagued by negative equity rates in excess of 20 percent. In the Southwest, areas such as Bakersfield (22 percent), Las Vegas (25 percent) and Tucson (24 percent) have above average raters of underwater homeowners. Chicago (22 percent) and Dayton (21 percent) have the highest rates of negative equity among Midwestern metros. In the Southeast, Atlanta (21 percent) and Jacksonville (22 percent) have some of the higher incidences of negative equity among larger metro areas nationwide.

On the flip side, there are many areas with below average rates of negative equity. Areas with the lowest rates of negative equity tend to also be areas where home values have surpassed their bubble-era peak in home values or where home values weren’t as hard hit after the housing bubble burst in 2007. For example, San Francisco and San Jose metros have negative equity rates below 10 percent. Larger metro areas in Colorado and large Texas markets also have sub-10 percent negative equity rates.

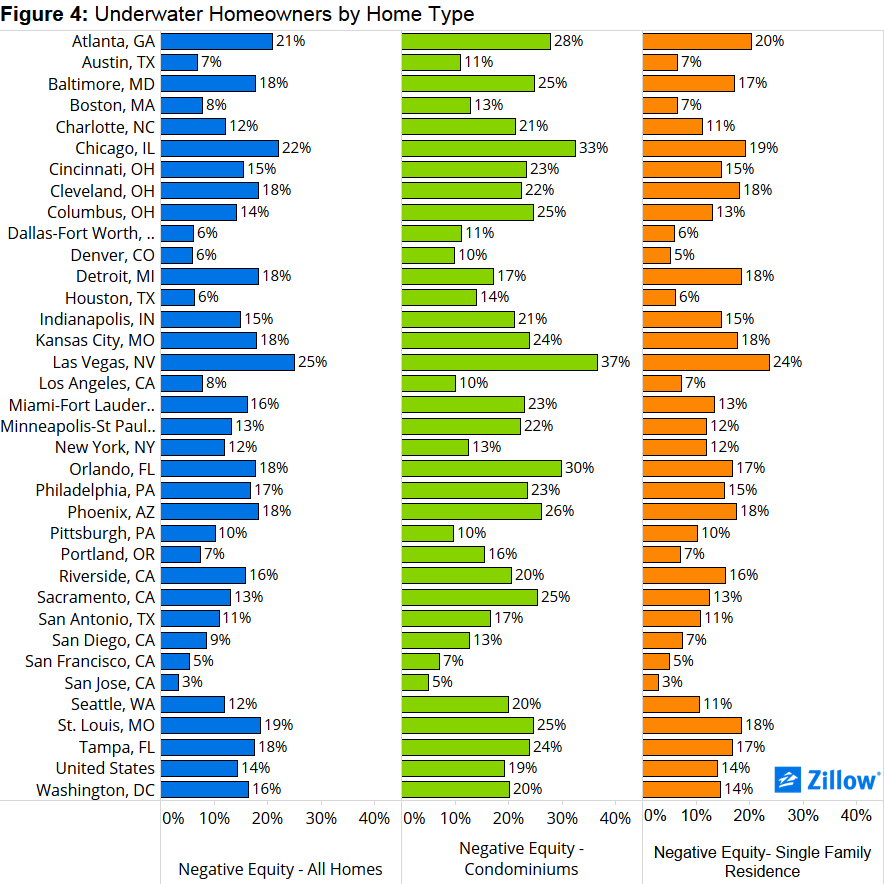

New for 2015 Q2, we compared the rate of negative equity across home type (figure 4). Nationally, condominiums had a higher rate of underwater homeowners when compared to homeowners of single family homes (19.3 percent vs. 14 percent). Metro areas with the largest rates of underwater condos are also markets with above average rates of negative equity. Las Vegas (36.7 percent), Chicago (32.6 percent) and Orlando have the highest rates of condo negative equity among the largest 35 markets.

San Jose (5.1 percent), San Francisco (7.1 percent) and Pittsburgh (9.6 percent) have the lowest rate of condo negative equity. Of the largest 35 metro areas, only Detroit and Pittsburgh have higher rates of negative equity in single-family homes compared to condominiums.

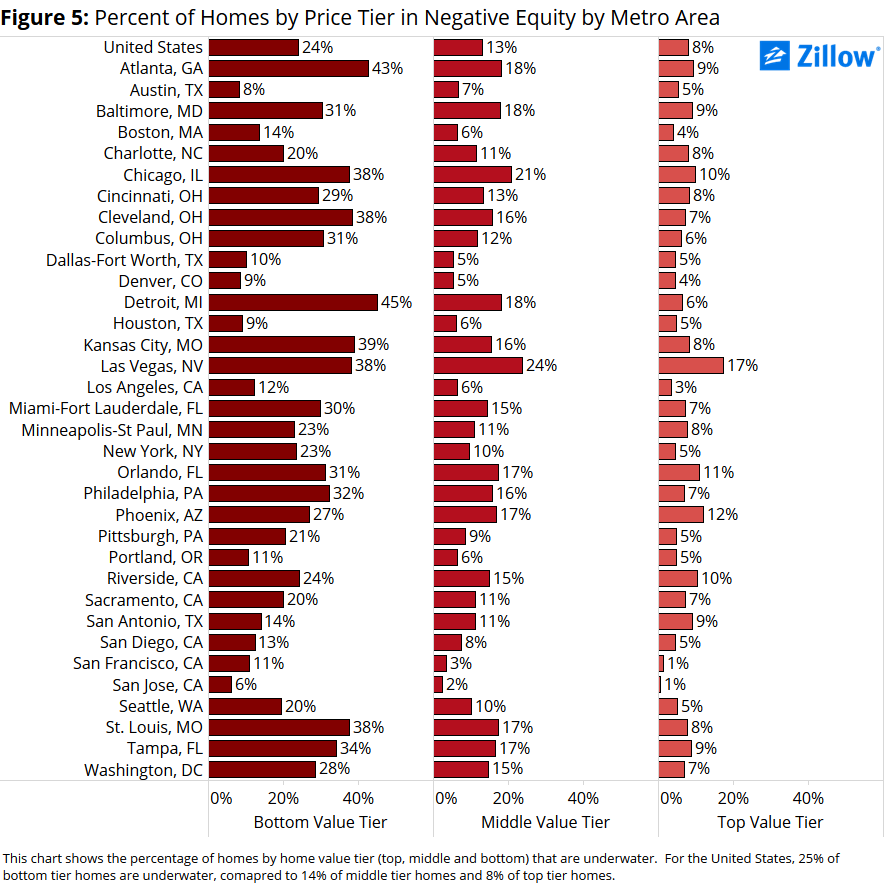

The bottom third of homes by value continue to be the homes most affected by negative equity (figure 5). Underwater homeowners of these cheaper, typically entry-level homes that are unable to sell are affecting the overall housing market. Potential first-time buyers will have difficulty finding affordable homes for sale because those homes are stuck in negative equity. And owners of those homes can’t move up the chain because they’re stuck underwater in the entry-level home they bought years ago. The logjam at the bottom is having ripple effects throughout the market, and as home value growth slows, it will be years before it gets cleared up.

Overall, 24 percent of homes in the bottom tier of home values nationwide are underwater, compared to 8 percent of homes in the top tier. Among the 50 largest metros, those with the greatest inequality between the top and bottom home values tiers in terms of negative equity are Atlanta (43 percent vs. 9 percent), Cleveland (38 percent vs 7 percent) and St. Louis (38 percent vs. 8 percent). But, all is not lost for owners in the bottom tier who are underwater. Homes in the bottom tier by value saw strong appreciation in the first half of 2015 (figure 6).

While it’s undoubtedly great news that the level of negative equity is falling, the imbalance between condominiums and single family homes may continue.

Over the coming year, even with slower appreciation in home values, negative equity is predicted to fall to 13.2 percent, freeing more than 650,000 homeowners, moving their loan-to-value ratio into the black. Some metropolitan areas are already seeing their rates approaching more “normal” levels of negative equity, however the distortions negative equity causes will stay with us for the foreseeable future. Moving forward, only time will heal these wounds.

{kind=link}