Pandemic Impacts Felt More Strongly by Lower-Income, Renter and Households of Color

Black, Latinx, lower-income & renter households were more likely to report housing and economic challenges brought on by the pandemic.

Black, Latinx, lower-income & renter households were more likely to report housing and economic challenges brought on by the pandemic.

While the coronavirus pandemic created new challenges for all Americans, Black, Latinx, lower-income and renter households were more likely to report encountering housing and economic challenges, according to new Zillow research.

In partnership with the National Fair Housing Alliance, Zillow surveyed 10,000 adults in 20 major metro areas nationwide on topics ranging from the socio-economic impact of the coronavirus pandemic as it relates to housing, to overall knowledge around home buying. In addition to being more likely to report housing and economic challenges during the pandemic, Black, Latinx and renter households were also less likely to report feeling knowledgeable about key situations related to the homebuying process. Together, these have the potential to slow progress to close the racial wealth gap.

Around a quarter of households surveyed (27%) reported losing income because of the pandemic, and about one in seven (14%) said that at least one member of their household lost their job. Latinx (20%) and Black (16%) households were more likely than white ones (12%) to report a job loss in their household. Renters were also more likely to report a loss of income (32%) and/or job loss (19%) than homeowners (23% and 10% respectively).

Given that renters were more likely to report job and/or income loss due to the COVID-19 pandemic, it makes sense that renters were also more likely to say they encountered difficulty keeping up with their rent payments (16%) than homeowners with their mortgage payments (7%). Black and Latinx households were more likely to say that they were having difficulty keeping up with mortgage/rent payments (13% and 15% respectively, compared with 10% of white households). The case was similar for the share of households that reported having mortgage forbearance or a reduced rent agreement: Black (9%) and Latinx (10%) households were about twice as likely as white ones (4%) to report such a situation.

Among the metro areas sampled, approximately one in ten (11%) said their household was having difficulty keeping up with mortgage or rent payments and a similar 12% said they were afraid that they may lose their home due to foreclosure or eviction. This number was higher for renters (16%), lower-income households (18% for households making less than $50,000), Latinx (22%) and Black (16%) households. Households in the Las Vegas (17%), Miami (17%), Los Angeles (16%) and San Francisco (15%) metro areas were most likely to express such fears of foreclosure or eviction.

Among households with children, 77% reported that their children were being educated at home because of the pandemic. And while the share of households receiving education at home was similar among renters, homeowners, and by race and ethnicity, renters and households of color were less likely to be equipped with certain resources like personal computers, internet access, and tutors. Almost three in five households (58%) whose children were learning remotely said their children have their own computers to do school work. This number is lower for renters (53%) than homeowners (65%). White and Asian households were also more likely to report that their children have their own computers to do school work than Black or Latinx households (61% among white households, 67% among Asian households and 53% for both Black and Latinx households). Homeowners were almost twice as likely as renters to say that they hired a tutor to help with remote learning (13% versus 7%), and the same divide existed between white (13%), Black (7%) and Asian (7%) households.

Latinx households were also significantly less likely to say that their home had adequate internet access for their child to complete their school work (51%) than white ones (61%). Comparing results by metro area, the Minneapolis metro stood out from the others regarding adequate internet access: 71% of Minneapolis-area households said their homes had adequate internet access for their children to complete their school work – most similar to Phoenix (64%), Washington DC (64%) and Seattle (63%) and significantly higher than all others.

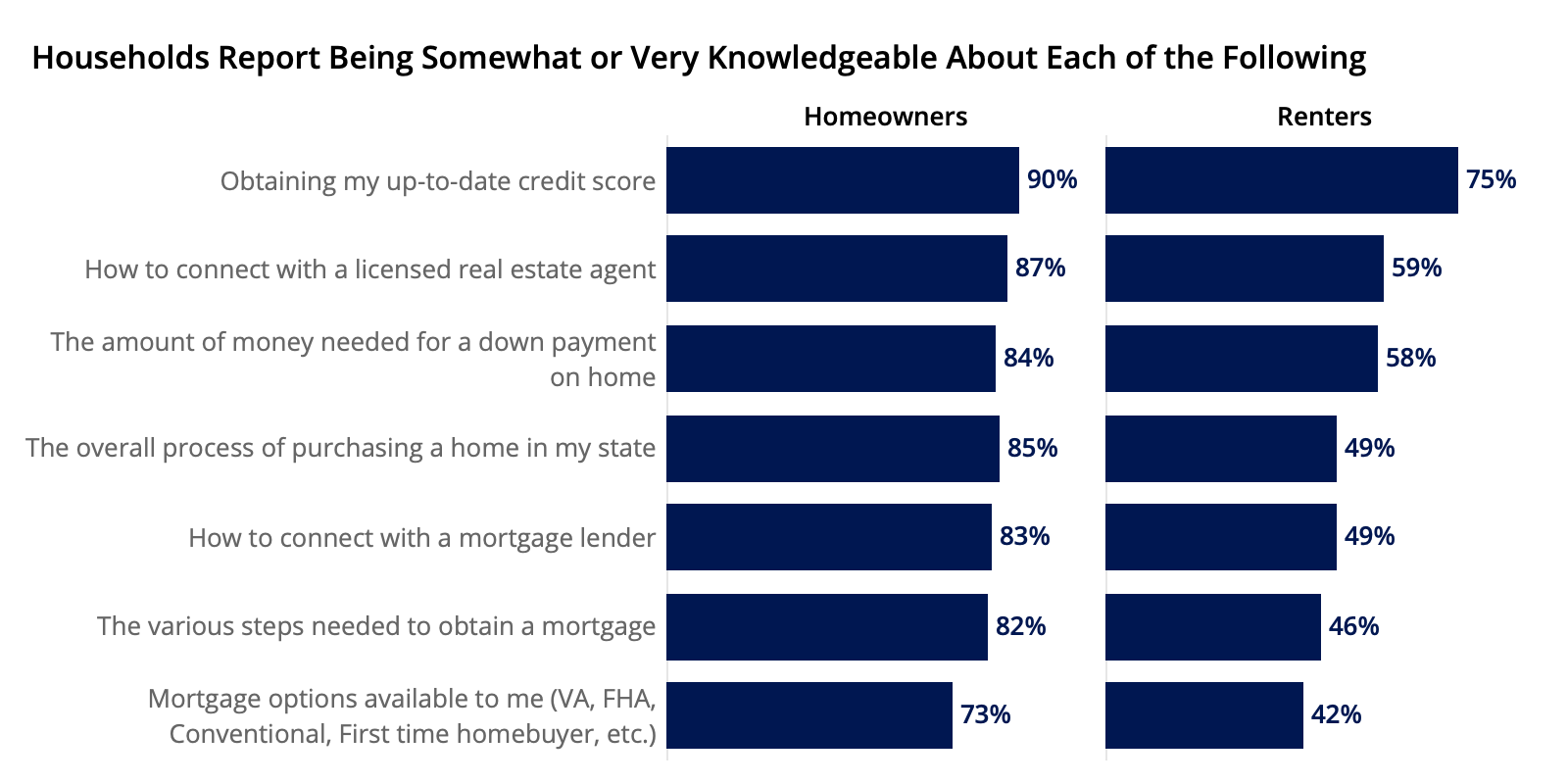

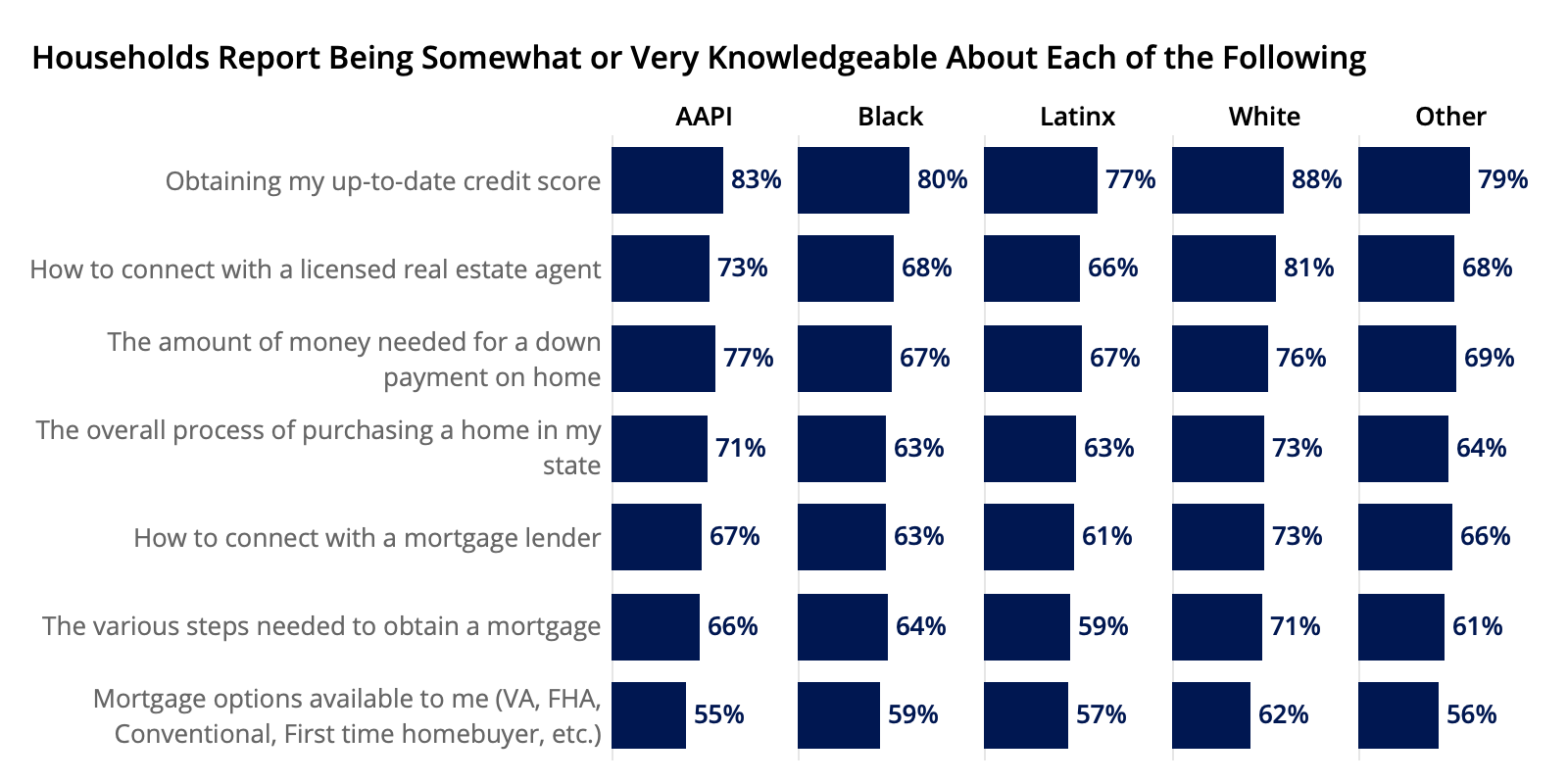

In addition to measuring the impact of the COVID-19 pandemic, respondents were asked a series of questions to gauge how knowledgeable they feel about key elements in the homebuying process. Respondents were most likely to report feeling somewhat or very knowledgeable about obtaining their up-to-date credit score (84%), followed by connecting with a licensed real estate agent (75%), the amount of money needed for a down payment (73%), the overall process of purchasing a home in their state (70%), connecting with a mortgage lender (68%), the various steps to obtain a mortgage (67%), and which mortgage options are available (60%).

White households were more likely than their Black and Latinx counterparts to report feeling somewhat or very knowledgeable about each situation. Unsurprisingly, homeowners were more likely than renters to report feeling somewhat or very knowledgeable about each situation.

To further understand home-buying knowledge, respondents were asked how much of a down payment they believe was needed in order to purchase a home. Among those who report being at least somewhat knowledgeable about down payments, respondents were most likely to say that they needed to put down 20% of the purchase price in order to purchase a home. Saying 10% was necessary followed (20%). Less than one in five (18%) said 25% or more was necessary, and 16% said they had to put down 5% or less.

Black households are more likely than white ones to report believing that they need to put down 25% or more (37% say so, compared to 23% of white households). The trend is similar among Latinx households – 32% of which say they need to put down at least 25%. The typical down payment on a mortgaged house is 10-19% the purchase price of the home.

Zillow partnered with market research firm IPSOS to collect representative samples of approximately 500 households in each of the following 20 U.S. metropolitan areas: Atlanta, Boston, Chicago, Dallas, Denver, Detroit, Los Angeles, Las Vegas, Miami, Minneapolis, New York, Philadelphia, Phoenix, St. Louis, San Diego, San Francisco, San Jose, Seattle, Tampa and Washington, DC.. The survey asked participants a series of housing-related questionss, including their knowledge of home financing, buying and selling, as well as their specific housing needs, aspirations and perspectives. Data collected in the January 2021 Zillow Housing Aspirations Report included additional questions on the impact of the COVID-19 pandemic.

{kind=link}