Price Cuts on Newly Constructed Homes Becoming More Common

Home shoppers across the nation may have an easier time finding a deal on a newly constructed home than they did a year ago.

Home shoppers across the nation may have an easier time finding a deal on a newly constructed home than they did a year ago.

Home shoppers across the nation may have an easier time finding a deal on a newly constructed home than they did a year ago. In nearly all major metro areas, the share of newly-constructed homes for sale that had their price cut at least once increased in 2018, in some cases by substantial margins.

In the fourth quarter of 2018, more than a quarter (25.1 percent) of newly constructed homes listed for sale had their list prices cut at least once – up from 19.2 percent in the first quarter 2018. That’s far higher than price cuts in general. In November 2018, for instance, 16.3 percent of all listings – not just new construction – experienced a price cut.

Price cuts in general did become more common in 2018, especially at the high end of the market. Many newly constructed homes are listed in these pricier segments, in large part because of market dynamics including high and rising building costs.

Three major factors contributed to the increase in price cuts, particularly for new construction:

The cumulative build-up in home values and rising mortgage rates eventually caused housing demand to fall. Teamed with increases in housing supply, those factors appear to have impacted the housing market for both buyers and sellers. As home value growth slows, the prospect of buying a new home becomes less attractive, because the return on investment becomes less of a sure thing. This feeling is exacerbated by rising mortgage rates. As rates increase, homeowners are less likely to take on new mortgages and buy new homes, instead opting to stay put in their current homes at presumably lower rates.

Rising mortgage rates also affect affordability – the share of income that a homeowner must put toward a mortgage. Despite record-high home values (that by most measures have grown faster than incomes) that mean daunting down payments for many buyers, the share of income a typical U.S. homeowner spends on her mortgage remains below historic levels, as low rates have kept mortgage payments subdued. Rising rates would change that for the worse.

However, this phenomenon of price cuts could be short lived. Mortgage rates softened in the final weeks of 2018, offering some hope to both buyers and sellers. Should they stay put, these relatively lower rates will provide an important test of exactly how much higher interest rates weighed on home sales and added to the frequency of price cuts last year. What’s more, with single-family home starts having pulled back, there should be fewer new homes for sale in the coming months, resulting in a more competitive market that may push prices up.

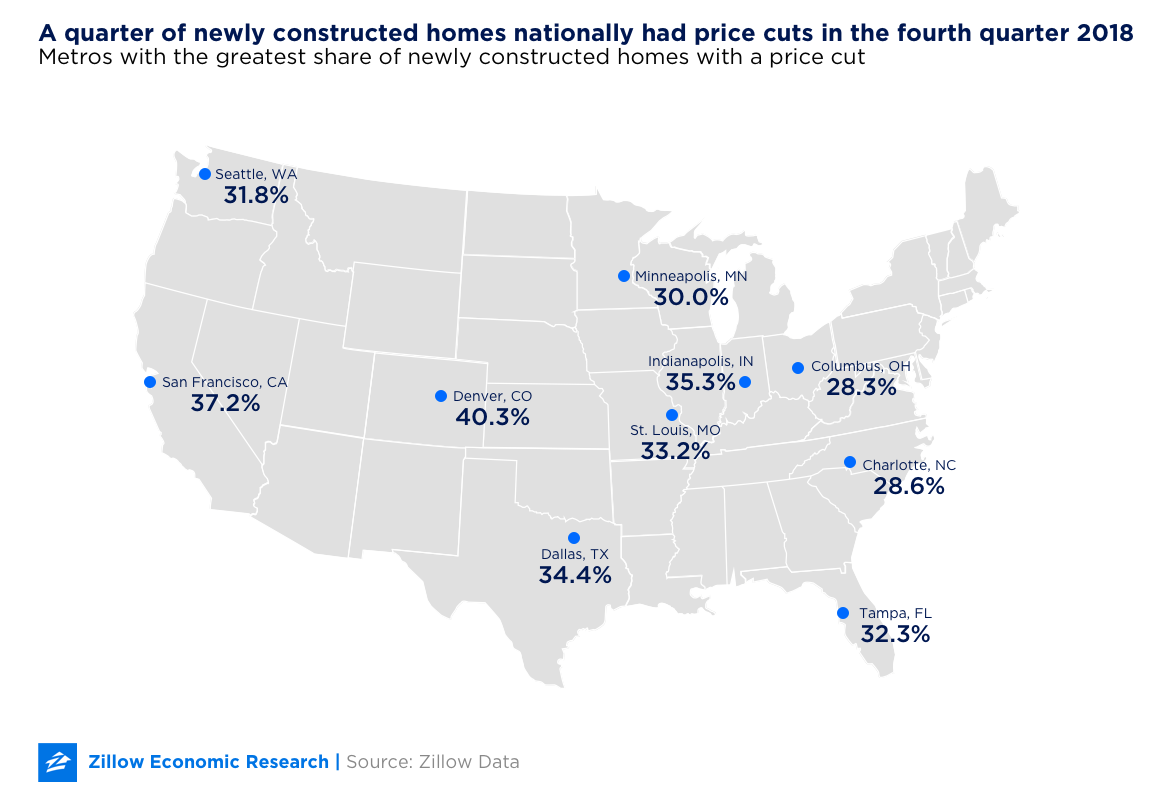

Of the nation’s 35 largest markets, the share of newly constructed homes experiencing a price cut increased the most in pricey tech hubs. In San Francisco, 37.2 percent of newly constructed homes on the market experienced at least one price cut in the last quarter of 2018, compared to 12.2 percent in the year’s first quarter — a 25-percentage point increase over the year. By comparison, in November 2018, just 13.3 percent of all listings in San Francisco had their prices cut at least once. Other technology hubs, including Seattle (+19.9 percentage points) and Denver (+19 percentage points), experienced similar trends. In the last quarter of the year, 40.3 percent of new construction listings in Denver had at least one price cut, the most of any metro at any time during the year.

Las Vegas also saw a sharp increase, with the share of new construction with a price cut spiking from 8.1 percent in the first three months of 2018 to 27.3 percent in the last three months.

Not all markets experienced this phenomenon, however. In Pittsburgh, San Antonio and Austin, Texas, price cuts on newly constructed homes were less frequent at the end of the year than they were at the beginning. Austin saw a sharp increase in this rate during the middle of the year, but it had fallen again by year’s end.

{kind=link}