Homeownership Up Among People Under 35 (Q2 2019)

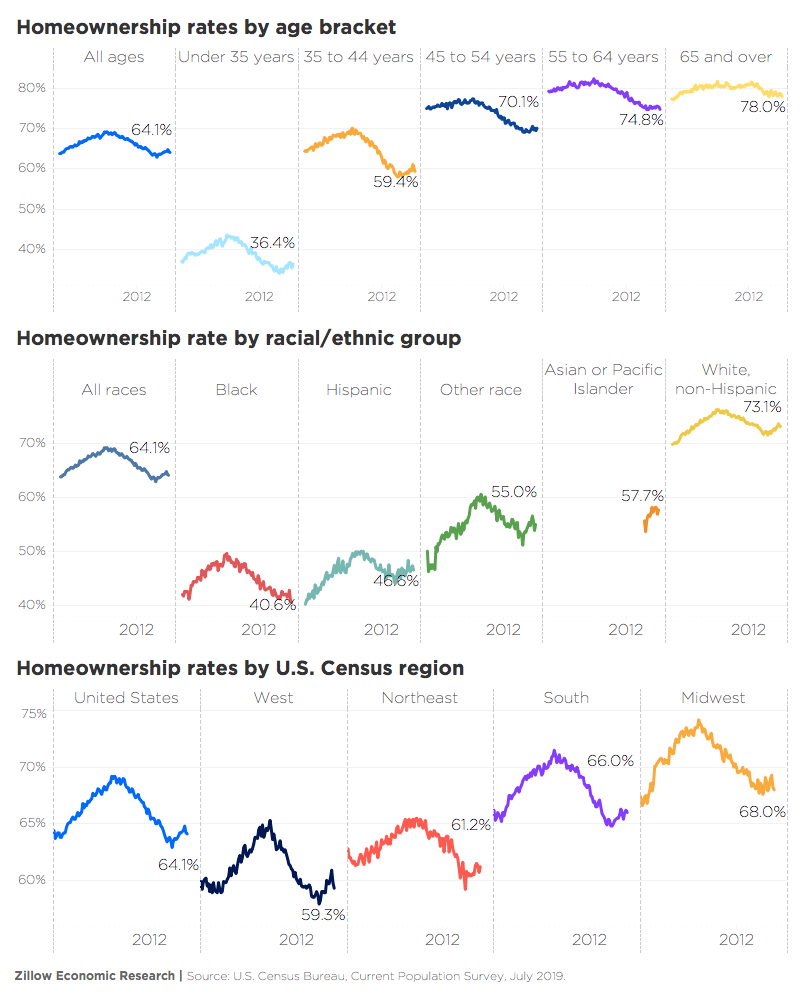

In a surprising turn, while their older peers have apparently been pulling back, the homeownership rate in the under-35 age bracket increased.

In a surprising turn, while their older peers have apparently been pulling back, the homeownership rate in the under-35 age bracket increased.

Homeownership rates repeated the declines of the previous quarter, albeit less dramatically. The declines we’ve seen in recent quarters are erasing gains we started to see in 2016. The continued decline was more dramatic in older age brackets. In a surprising turn, while their older peers have apparently been pulling back, the homeownership rate in the under-35 age bracket increased.

This goes against the abrupt slowdown in home value appreciation in the entry-level market: As home values exploded over 2017 and 2018, incomes were dwarfed. By 2019, some buyers simply couldn’t save enough for a down payment and pulled back from the market, causing sales and home value appreciation to slow dramatically. Given the affordability challenge of saving for that down payment, this could be a testament to the ambition of younger households to break into homeownership.

While last quarter the Hispanic homeownership rate was the most stalwart — the only racial/ethnic group to see increases — this quarter erased all those gains.

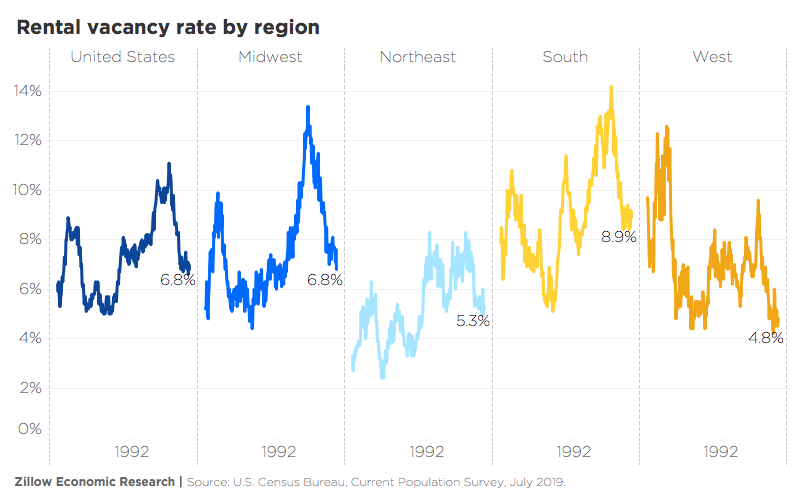

As buyers pull back from the for-sale market, they’re remaining in rental markets for longer. All that recent apartment building, while taking off the pressure within principal cities (building was generally concentrated downtown), it still wasn’t enough to help renters in the suburbs and more rural areas, where rental construction has been missing.

If the declines in the homeownership rate in the first quarter were a harbinger of a housing market slowdown, the very modest decrease in the second quarter of 2019 is a signal that the slowdown is not the end of the world. It’s a momentary breather, an acknowledgement that the home value appreciation of 2017 and 2018 was not sustainable and that 2019 could net out as a much more sane year.

While the market is on the right track toward becoming healthy and sustainable, “more sane” doesn’t mean fully recovered. It’s been several years since home values started growing again from those low, low levels during the housing bust, and a few since the homeownership rate started rising again. It’s tempting to think we’re back. We’re not.

In most age brackets, homeownership rates are nowhere near their levels of the late 1990s, before the housing bubble. This is particularly true for 35- to 44-year-olds, whose homeownership rate remains over 5 percentage points below the rate in June 1995 (59.4% versus 65.1%). The only two age groups that approach or exceed pre-bubble years are the ones lucky enough to have dodged the mother of all boom and bust cycles:

For those generations that bore the brunt of the housing bust, the road to recovery is long, and likely even longer given the fast return of home prices. If you foreclosed on your property, you didn’t benefit from home price recovery, yet the down payments are as expensive as they’ve ever been.

A look within racial/ethnic groups shows distinct winners and losers. For whites and Hispanic households, the current homeownership rates exceed those of the mid-’90s. The story for black households is much more bleak. Having fallen more during the housing bust, black homeownership shows little to no signs of recovery. The gains made at the end of 2018 were erased in the first quarter of 2019. This second quarter shows black homeownership declining further still. These patterns strongly suggest that something real needs to change to put us on the path toward parity. As it stands, inequities between white and black continue to get worse, not better.

{kind=link}