Q4 2016 Housing Affordability: Accelerating Home Values, Rising Rates Cause Rapid Deterioration

Rising mortgage interest rates and continued home value growth helped make mortgages less affordable by the end of 2016 than they’ve been in half a decade. And while mortgages remain “affordable” relative to historic norms, as growth in housing costs continues to outpace growth in wages, affordability should be expected to continue to rapidly deteriorate.

- At the end of 2016, a typical buyer purchasing the typical U.S. home could expect to pay 15.8 percent of their income on a mortgage – the highest share necessary in more than six years.

- Both home value acceleration and rising mortgage interest rates are causing mortgage affordability to suffer.

- The share of income necessary to afford a typical U.S. rental home fell in Q4, to 29.2 percent, but remains higher than both historic averages and the share needed to afford a typical mortgage.

Rising mortgage interest rates and continued home value growth helped make mortgages less affordable by the end of 2016 than they’ve been in half a decade. And while mortgages remain “affordable” relative to historic norms, as growth in housing costs continues to outpace growth in wages, affordability should be expected to continue to deteriorate.

At the close of 2016, home buyers purchasing the typical U.S. home could expect monthly mortgage costs of $758 (figure 1),[1] or 15.8 percent of the median household’s monthly income – up from 14.7 percent in Q4 2015 and the highest share necessary since mid-2010. The share of income needed to afford a typical home is still low relative to both the housing bubble years (2000-2007) and more normal times (1985-2000), when the typical household would need to spend 20 to 25 percent of their income on a mortgage, but it’s quickly worsening. And as mortgage interest rates rise and if homes appreciate in value as expected, affordability will deteriorate even more. At 5 percent mortgage interest rates, it will take 17.9 percent of monthly income to afford a monthly mortgage payment on the typical U.S. home; at 6 percent, that rises to 20 percent of monthly income.

But while deteriorating affordability itself is concerning, especially as we look ahead toward even higher rates, the core trend driving it is arguably even more troubling – and it’s happening now: Growth in mortgage payments is currently outpacing growth in household incomes. In 2016, typical U.S. household incomes grew 2.2 percent, a slowdown from growth of 3.3 percent in 2015. The mortgage payment on the average U.S. home, on the other hand, grew by 9.9 percent in Q4 2016,[2] up from 6.7 percent in Q4 2015.

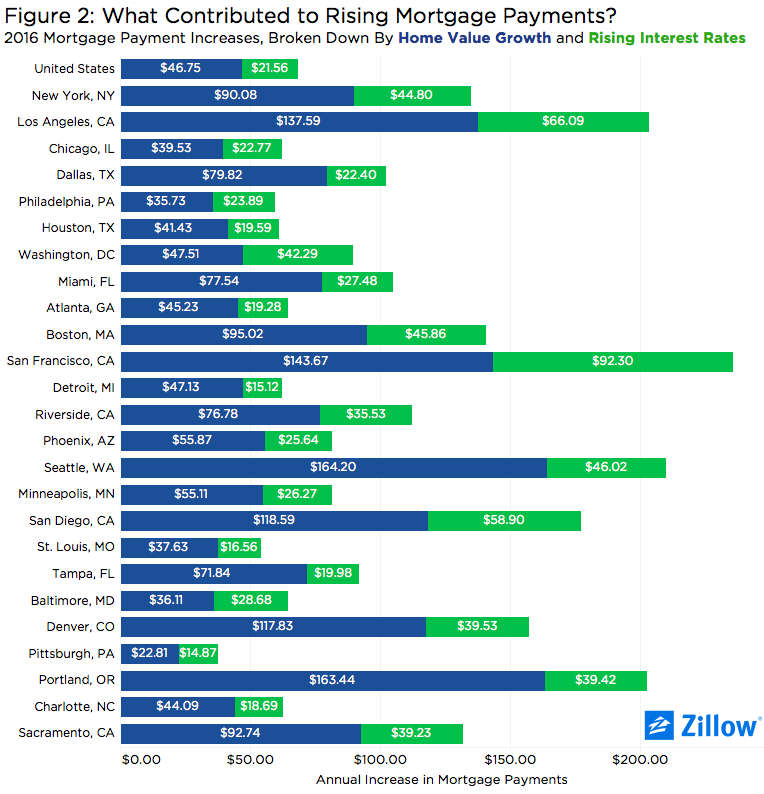

This increase in mortgage payments is driven by two factors. The Federal Reserve board voted to raise the federal funds rate target in Q4, which has a big influence on the mortgage rates offered by lenders. At the end of 2016, mortgage rates rose from the mid 3s to north of 4 percent. This increase in rates, however, was not met with a slowdown in home value appreciation. The median U.S. home appreciated 1.9 percent in the fourth quarter alone, the fastest quarterly growth recorded since the housing recovery began in earnest in early 2012. And higher mortgage rates coupled with more valuable homes means monthly payments will rise: compared to a year ago, the average mortgage payment nationwide grew from $690 to $758. Of that $68 increase, $47 comes from rising home values rising and the remainder is the result of higher mortgage rates (figure 2).

This increase in mortgage payments is driven by two factors. The Federal Reserve board voted to raise the federal funds rate target in Q4, which has a big influence on the mortgage rates offered by lenders. At the end of 2016, mortgage rates rose from the mid 3s to north of 4 percent. This increase in rates, however, was not met with a slowdown in home value appreciation. The median U.S. home appreciated 1.9 percent in the fourth quarter alone, the fastest quarterly growth recorded since the housing recovery began in earnest in early 2012. And higher mortgage rates coupled with more valuable homes means monthly payments will rise: compared to a year ago, the average mortgage payment nationwide grew from $690 to $758. Of that $68 increase, $47 comes from rising home values rising and the remainder is the result of higher mortgage rates (figure 2).

How long this trend can continue is an open debate, but at some point it seems certain that rising mortgage interest rates will begin impacting home value growth as affordability keeps getting worse and more home buyers balk at heftier price tags. A recent Zillow survey of more than 100 economists and real estate experts nationwide found that a majority expect rising rates to be the major trend influencing housing this year. And once rates hit about 5.5 percent, according to the panel, rising rates may impact not only affordability for new buyers, but also the ability or desire of current homeowners to list their home for sale and move into a new one, a phenomenon known as “mortgage rate lock in.”

For those looking for a silver lining, one could be found among the nation’s renters. While mortgage affordability deteriorated drastically in Q4, rent affordability actually improved somewhat as growth in rents flattened. The share of income needed to afford the median U.S. rental home was 29.2 percent in Q4, down slightly from 29.4 percent at the end of 2015. Still, this recent improvement is unlikely to generate much applause from the roughly one-third of U.S. households that rent. While rent affordability has improved very modestly over the past year, it is still much worse relative to historic averages – in the years between 1985 and 2000, renters could expect to spend about 25.8 percent of their income on rent.

Use the interactive tool below to explore mortgage and rent affordability in your market, how it has changed over time, and how it could change going forward as housing costs rise and rates change.

[1] Assuming a 20 percent down payment on the median-valued home, and a 30-year, fixed-rate mortgage at currently prevailing rates.

[2] Home prices may have risen even more in 2016 Q4, if mortgage rates had not increased.

{kind=link}