Rate, Price Drops Won’t Substantially Improve Affordability

Key takeaways:

Affordability for home buyers has improved slightly nationwide over the last year. Price growth has flattened out, mortgage rates have been marginally lower and income growth has forged ahead. But affordability challenges are still holding back buyers, especially those without equity from a previous home to fund their next purchase.

Zillow expects home values to tick down nationwide, ending the year about 2% below where they started. That small decline won’t be much of a setback to most homeowners’ equity following the 49% increase since 2019. It also won’t move the needle very far for first-time buyers priced out of the market.

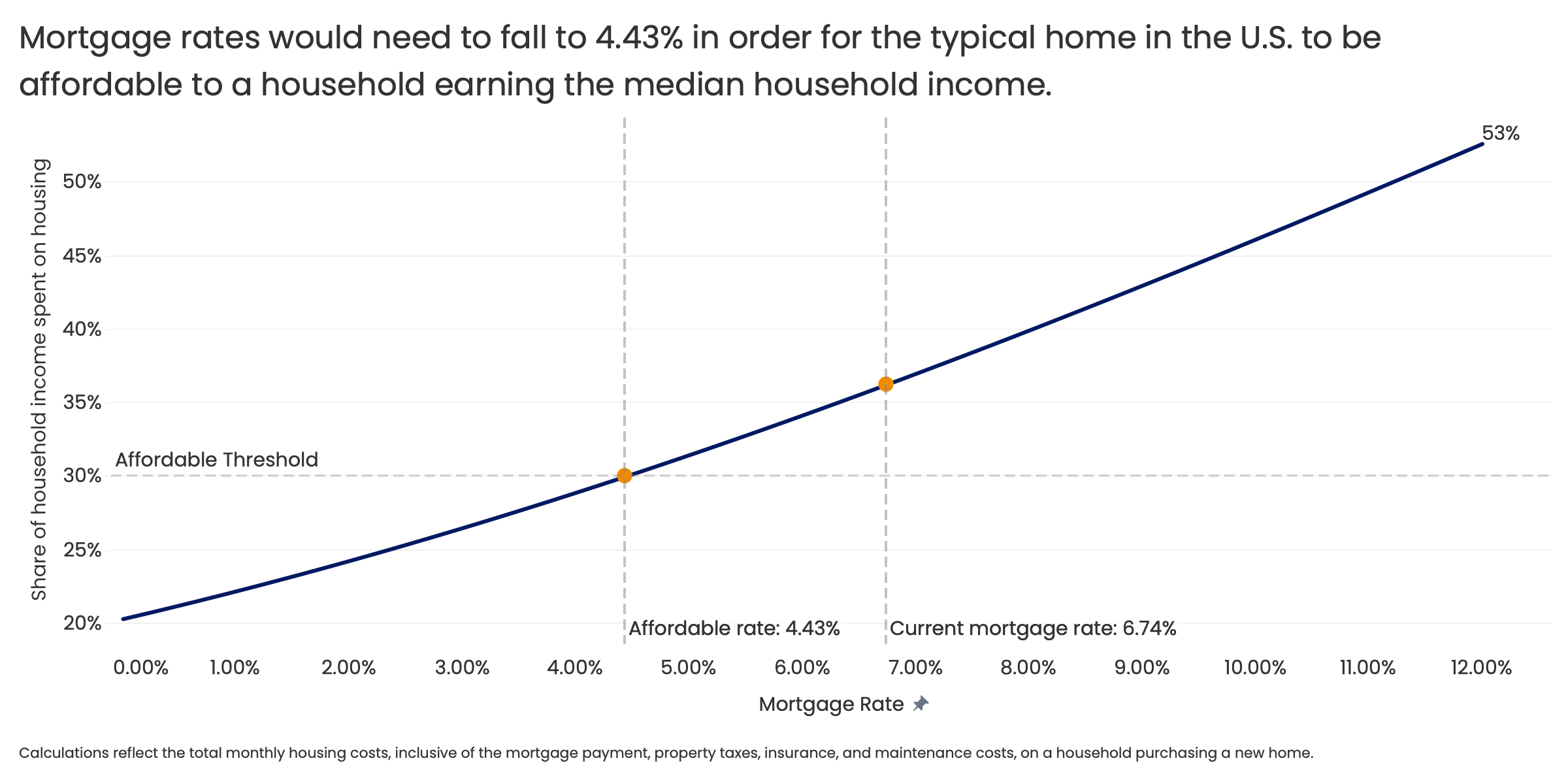

Home prices and/or mortgage rates would need to drop by massive amounts to make a typical home affordable for a median-income family.

Holding incomes, home prices and all other housing-related costs equal, mortgage rates would need to drop to 4.43% in order for a typical home to be affordable to a buyer making the median income, assuming they put 20% down. That kind of a rate decline is currently unrealistic.

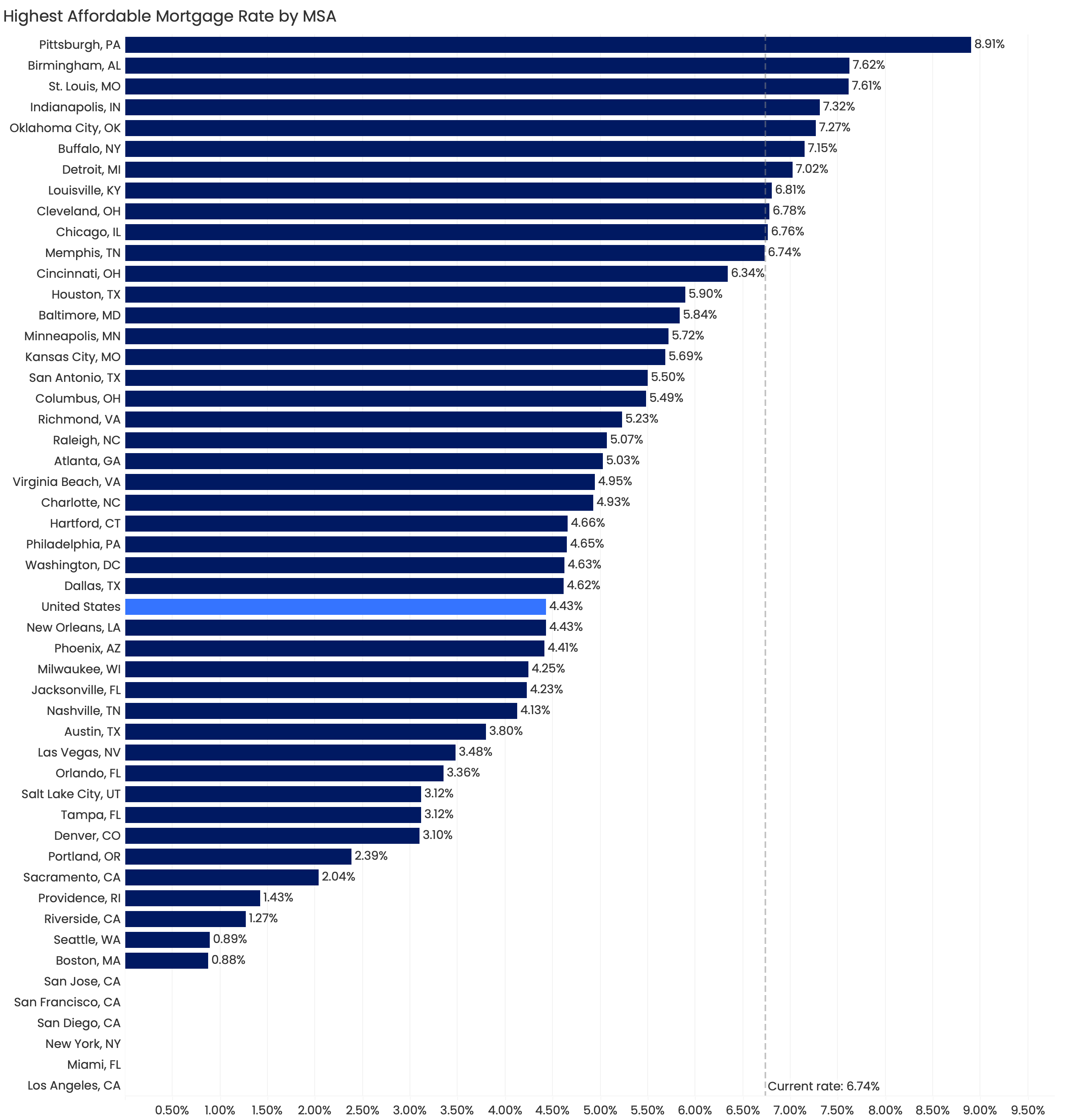

Not even an interest-free loan would make the typical house affordable in some expensive coastal metros without a substantial down payment. This is the case in New York, Los Angeles, Miami, San Francisco, San Diego, and San Jose. In these metros, even just taxes, insurance, and maintenance can cost over 10% of the median income. These high additional costs limit how much families can pay toward the mortgage at all, while keeping housing costs under 30% of their income. Some other metros are on the cusp of this “impossible to afford” scenario. In Boston and Seattle, the affordable rate would have to be less than 1%.

Across the Midwest and Inland South are a few metros where homes are still affordable with rates above 6.7%:

Declining home values would be another way to reach affordability, and slight declines are expected in the months ahead. But this path to affordability is extremely unlikely to pay off. If rates and other factors held steady, home values would need to drop 18% for the typical home to be affordable for a median-income family.

If buyers are waiting for big drops in mortgage rates or prices to help affordability, they’re in for a rude awakening. Just like falling rates, that kind of correction in house prices won’t happen without a serious slowdown in economic growth and income growth, and a rise in the unemployment rate.

Rather, the only sustainable solution to the affordability crisis is not through a fall in prices or mortgage rates, but through building enough to close the housing deficit.

{kind=link}