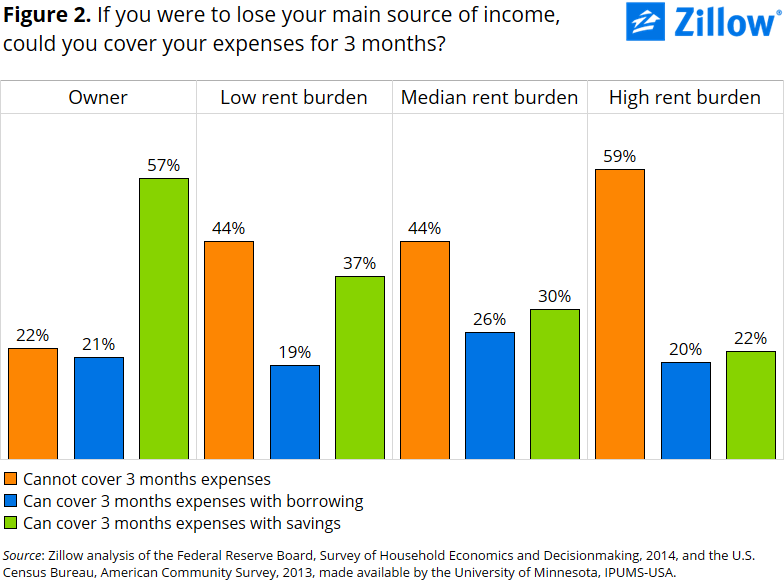

- Almost 60 percent of households with the highest rent burden could not cover three months’ worth of expenses in the event of a financial emergency.

- High rent burdened households are also more likely to sacrifice medical care to make ends meet than other households.

When rents rise faster than incomes, as they have in recent years, renters are forced to tighten their belts elsewhere. Case in point: foregoing “unnecessary” preventive medical care.

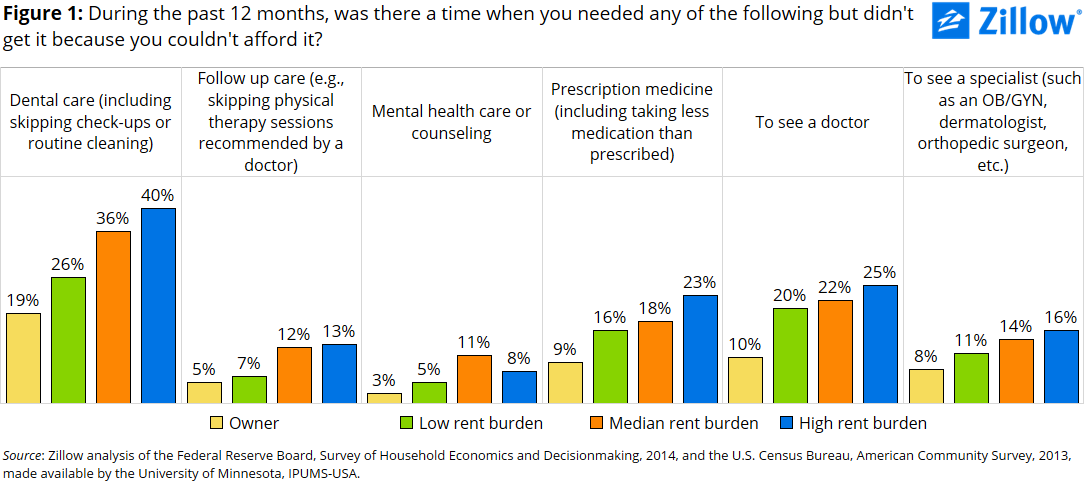

Households with the highest rent burdens[i] were much more likely to not seek medical attention because they were worried about the cost, according to the Federal Reserve Board’s October 2014 Survey of Household Economics and Decisionmaking (SHED) (figure 1). Dental care appears to be the most common sacrifice, followed by routine check-ups and prescription medication. Among the highest rent burdened households, 40 percent said they skimped on the dentist, compared to 26 percent of the lowest rent burden households.

Medical care isn’t the only sacrifice made in the name of paying rent each month. Savings account balances also take a beating.

Among survey respondents, the typical renter with a low or median rent burden set aside 5 percent of his or her income each month as savings. Among renters facing high rent burdens, the median savings rate was zero – they essentially spend all (or, in some cases, more than all if they borrow or use credit) of their incomes. Almost 60 percent of high rent burden households said they could not cover three months’ worth of expenses if they were to lose their main source of income, compared to 44 percent of renter households with lower rent burdens and 22 percent of homeowners (figure 2).

Today’s high rent burdens also have long-term ramifications. Among young adults, those with the highest rent burdens were much more likely to report having given no thought to financial planning for retirement. Even among those whose employers offer defined contribution retirement plans – for example 401(k) or 403(b) savings plans – high rent burdens translate into lower participation in retirement savings (figure 3).

Interested in analyzing the data yourself? Zillow’s code can be found here, and you’re welcome to use it as a starting point. Please let us know what you find!

[i] We calculate a rent burden by taking the ratio of monthly rent and monthly income. The top third of rent burdens are classified as “high rent burden” households, and the bottom third of rent burdens are classified as “low rent burden” households. For homeowners, the monthly mortgage payment is used instead of monthly rent. The SHED includes only tiered responses for household incomes, but we are able to impute household incomes by computing average incomes from the U.S. Census Bureau’s 2013 American Community Survey, including controls for age group, household tenure, income group and Census region. We use this imputed income to calculate rent burdens.