Rent vs. Buy: The Full Decision for 2024

When mortgage rates are near 3%, the majority of buyers break even and start building up a windfall relative to a renter making financial investments fully (but conservatively) within a few years. With mortgage rates above 6%, home buying is for households making a long-run financial decision again.

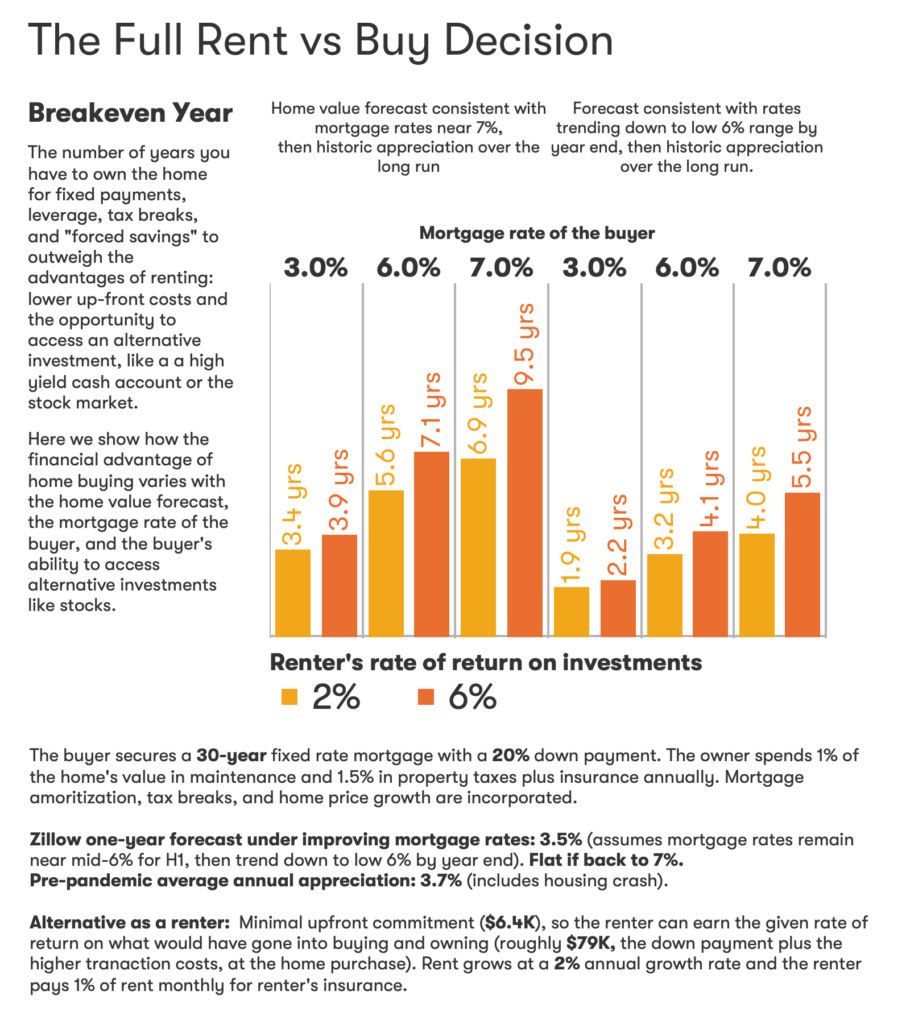

Zillow Research has abundant analyses describing the rising barriers to becoming a new homeowner. Here however, rather than ask “Can the typical household own a home?” we seek to answer “Should they?” We strip the decision down to its financials by estimating comparable for-sale prices and asking-rate rents on the typical home and then simulating transaction costs, home values, rents, insurance, property taxes, maintenance expenses and mortgage dynamics into the future to determine if the household is financially better off renting or buying the same home. (Not considered in this paper are cases in which properties available to purchase are not really available to rent.)

If you’re a risk-loving, stock-savvy individual who loves living in a different city every few years and never wants to paint a wall, you’re a “lifestyle renter.” If you want to shape your home into your legacy over many decades, you’re obviously a buyer.

We’re talking about the household that is somewhere in between: a typical risk-averse household unfamiliar with stock markets beyond retirement funds. The household is interested in the lifestyle that buying a home has to offer, but its members aren’t certain they will want to (or be able to) stay in the house they can afford for decades. What is that cutoff point? In other words, how much time is needed for the financial advantages of buying with a fixed-rate mortgage in the U.S. to overcome the large transaction costs of becoming an owner?

In this white paper and over the following weeks, we’ll be diving into the different components of the rent-versus-buy decision.

Our goal is to go beyond just the breakeven year that our simulation produces, and work toward helping our audience really understand the decision and its tradeoffs. When we report one number that supposedly summarizes so much complexity, we ask the audience for significant trust and hide a lot of detail. Each breakout is still fairly complex, but much less so.

There is also value in the details, especially for individual households, each with different concerns. Renting versus buying, depending on where you are in the country or on your credit profile, can be nuanced. It can be good for affordability and stability into the future, but bad as a real estate investment, for example. Breaking down the rent-versus-buy decision into three components goes a step beyond a black-box-style number to help customers make decisions according to what matters to them.

Stay tuned.

{kind=link}