Will Affordable Mortgages Ever Return?

Mortgage affordability has remained top of mind for home buyers, sellers and homeowners since mortgage rates started to rise in early 2022. The red-hot housing market of 2020 and 2021 that was largely influenced by artificially low rates allowed many shoppers to downplay the rising cost of housing, as mortgage payments remained affordable. Efforts from the Federal Reserve to try and keep the U.S. economy out of a major recession after the onset of the COVID-19 pandemic resulted in historically low mortgage rates. Easy financial conditions helped to stimulate spending and housing prices surged following the huge boost in demand. Throughout 2020, while home prices were at record highs and growing at a historically fast clip, monthly mortgage payments grew only modestly and remained within reach of those with enough means for a down payment and to win a bidding war.

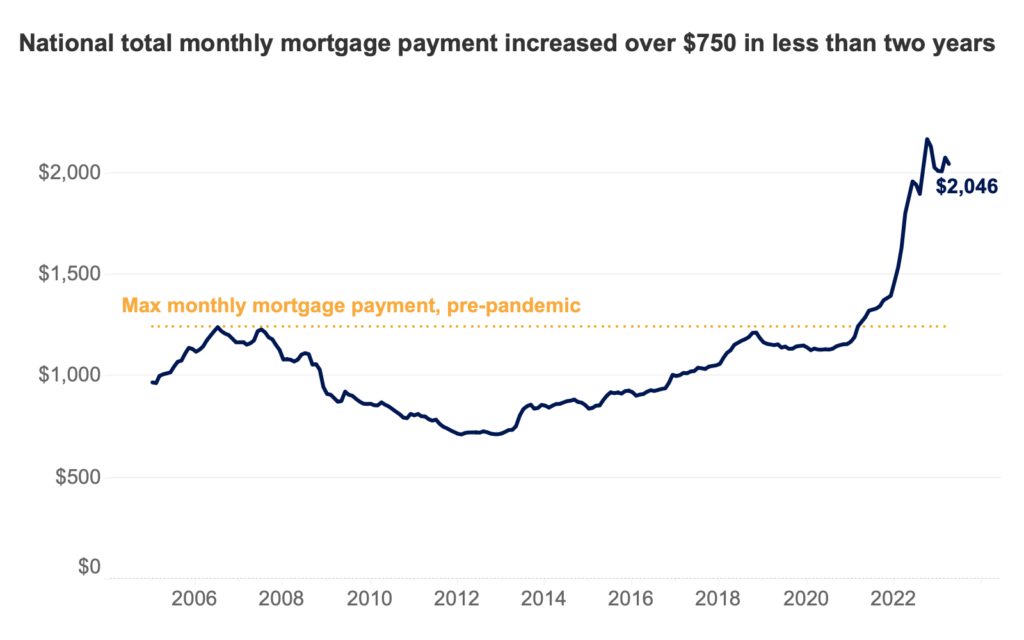

That dynamic shifted quickly in 2022 as mortgage rates started to rise. Inflation caught up to the stimulated economy and those ultra-low interest rates hit their end. As the Fed increased its benchmark interest rate and began offloading some assets from its balance sheet, mortgage rates followed and those 3% mortgage rates were soon replaced with rates over 6%. The reality that homes were now upwards of 30% more expensive than in early 2020 was now very apparent. The cost of a monthly mortgage payment (including taxes and insurance) topped $2,000 per month last fall for the first time ever.

While the cost of goods, including homes, was rapidly rising, incomes were not keeping up. And that started to impact home buyers’ ability to afford monthly mortgage payments, beyond the hurdle of saving for a seemingly ever-growing down payment. Mortgage affordability took the spotlight as the main focus and barrier for potential buyers, and sellers who are looking to buy again.

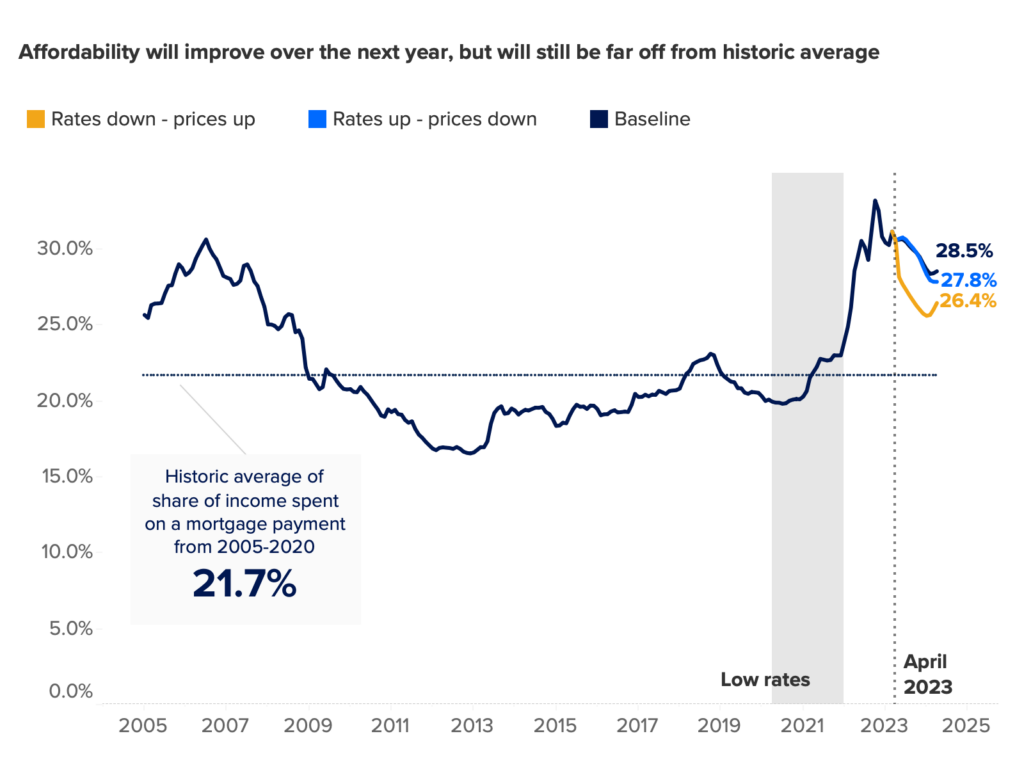

In October 2022, at the peak of unaffordability, a household buying the nation’s typical home would have been expected to spend 33.2% of its income on a total monthly mortgage payment (including taxes and insurance) — and that’s with a 20% down payment that we know most buyers don’t have. This was far beyond the historic average – as measured from 2005 to 2020 – of 21.7% of income spent on a mortgage and above the widely-cited 30% threshold used to gauge whether a household can afford their monthly housing payments.

Since then, falling rates (at least falling from the peak above 7%) and stabilizing home prices have helped affordability improve and further, albeit modest, improvements are likely over the next year. Our baseline expectation (dark navy line in the above graph) is that, by the end of 2023, prices will moderate and rates will stabilize below their 7% peak, a combination that will result in improved affordability for home shoppers.

A higher than expected uptick in mortgage rates (blue line) would likely cause prices to fall, but low levels of for-sale inventory would likely cap any meaningful price decline and ultimately minimize the impact on affordability. What’s more, mortgage rates have a larger impact on monthly payments than prices, so the uptick in rates in this scenario would outweigh the benefits afforded by modestly-falling prices.

Conversely, a decline in mortgage rates would likely stoke home buyer demand and encourage prices to start climbing again (gold line). This scenario of falling rates but accelerated price growth would likely improve affordability some of the next year, but it’s almost a certainty that the share of income spent on a total monthly payment will remain far higher than the historic average.

All told, regardless of any realistic path forward for mortgage rates and home prices, mortgage affordability will remain a barrier for many potential home buyers and sellers.

Some markets have seen prices moderate enough to make a significant impact on mortgage affordability. In some typically more affordable markets, such as Baltimore and Chicago, projected affordability a year from now in each of the scenarios described above is right around the historic average. This means potential buyers in these markets have seemingly lower hurdles to jump over for affordability. However, as home prices in these two markets only just recently passed the previous peak from the pre-2008 financial crisis, lower levels of home equity and thus household wealth could make affordability more challenging for some.

Other more expensive markets, like Los Angeles and Sacramento, are also projecting affordability in line with historic averages in the next year. But in Los Angeles, for example, the historical average share of income spent on a mortgage is over 50%. So coming back to normal doesn’t necessarily mean coming back to affordability.

In other markets, the super-charged price growth over the past three years has created a significant imbalance in mortgage affordability that isn’t projected to improve in a meaningful way over the next year. Salt Lake City is one such market, where prices have risen nearly 40% since pre-pandemic, leading to a massive spike in the share of income needed for a monthly mortgage payment – something that is unlikely to change in the next year.

While mortgage affordability as a whole might not have an optimistic outlook for the next year, there are many policies and products that can help potential buyers step over the financial hurdle and land in homeownership.

Tap into down payment assistance

Down payments used to take the spotlight when talking about for-sale housing affordability, and with the recent jumps in home values, down payments are still a significant challenge for many aspiring homebuyers. However, help is available. Thousands of down payment assistance programs exist across the country that many potential buyers don’t know they qualify for.

Even if a potential buyer has enough money for a down payment, utilizing available down payment resources can still be really beneficial. Many buyers struggle with pre-existing debt, like student loans, which can increase their debt-to-income ratio and make it more challenging to qualify for a mortgage or more likely that they will be quoted a higher mortgage rate. Using down payment assistance funds to make that initial payment, and turning existing savings to paying off other debts, might help some buyers find their footing in this market.

Pay down your mortgage rate

Another way extra cash up front can save money in the long run is by purchasing points, which many buyers already turned to in 2022. Paying for points on a mortgage is essentially paying to lower the mortgage rate. Each point costs 1% of the loan value and lowers the mortgage rate by 0.25 percentage points. So on a $300,000 loan with a 6.5% rate, a point would cost $3,000 and lower the rate to 6.25%, saving roughly $50 a month. In 2022, nearly 45% of successful mortgage buyers [1] purchased points, compared to 29.6% in 2021, 28.4% in 2020 and 27.3% in 2019. As interest rates started rising, many buyers jumped on the opportunity to save on their monthly payment.

Consider different mortgage products

Many lenders offer mortgage products to help buyers achieve affordability. Two common examples of such products are 2-1 buydowns and adjustable-rate mortgages. Rate buydowns are often negotiated to be given by the seller, where the seller would offer a concession at closing to essentially pay the difference in a monthly mortgage payment with a rate that is two points lower for the first year and one point lower in the second year. Buyers win with these products because their upfront payments are lower for the first two years, and sellers win because they walk away with more money than if they had dropped their price to achieve the same level of affordability for buyers.

Adjustable-rate mortgages – which allow borrowers to lock in a slightly lower rate for 5-10 years before adjusting to the market rate – can make a significant difference in monthly payments. These loans have much stricter regulations and are more transparent than they were earlier this century. In 2022, 12.5% of successful mortgage buyers [2] used adjustable-rate mortgages to help lower their initial rate, and the median time from loan origination to when the interest rate would change was seven years. So mortgage buyers in 2022 who used adjustable-rate mortgages have until 2029 to refinance or face a higher or lower rate on their mortgage, depending on what the market is doing, which is a long period to benefit from the lower upfront rate today.

While the market might not be in seemingly anyone’s favor and high level mortgage affordability isn’t likely to return to normal healthy levels anytime soon, there are ways that buyers and sellers can utilize existing resources to make affordability work for them. Other avenues to consider beyond the available mortgage products and resources might be to branch out to different property types. A single-family home is not the only viable or desirable option for many buyers, which is another reason why zoning reform (i.e., making it easier to build homes and to build higher density homes) would have a big impact on affordability. But in a volatile market like the one we are living in now, where day-to-day rate fluctuations can be the difference between getting approved for a mortgage and being turned away, being financially prepared and having a strong local agent on hand for when the right moment presents itself is as crucial as calling on the various policies and products available to alleviate affordability constraints.

The mortgage affordability data used both Zillow and public data sources. Zillow data was used for historical home values via the Zillow home value index, as well as forecasted home values from the Zillow Home Value Forecast. Public data from Freddie Mac’s Primary Mortgage Market Survey, accessed via FRED at the St. Louis Fed, was used for historical interest rates and merged with mortgage rate forecasts from Moody’s. Similarly, household income data was used from the American Community Survey for historical data, and was extrapolated forward using core CPI growth and forecasted core CPI growth from Moody’s. The mortgage affordability metric is calculated as the share of income spent on a mortgage payment.

[1] Successful buyers here are defined as conventional home purchase mortgage borrowers who had a loan originated on a primary home, from the Home Mortgage Disclosure Act database data pulled on 04/17/2023.

[2] Successful buyers here are defined as conventional home purchase mortgage borrowers who had a loan originated on a primary home in 2022, from the Home Mortgage Disclosure Act database data pulled on 04/17/2023.

{kind=link}