- Self-employed mortgage shoppers earn roughly 80 percent more than non-self-employed shoppers and seek more expensive homes.

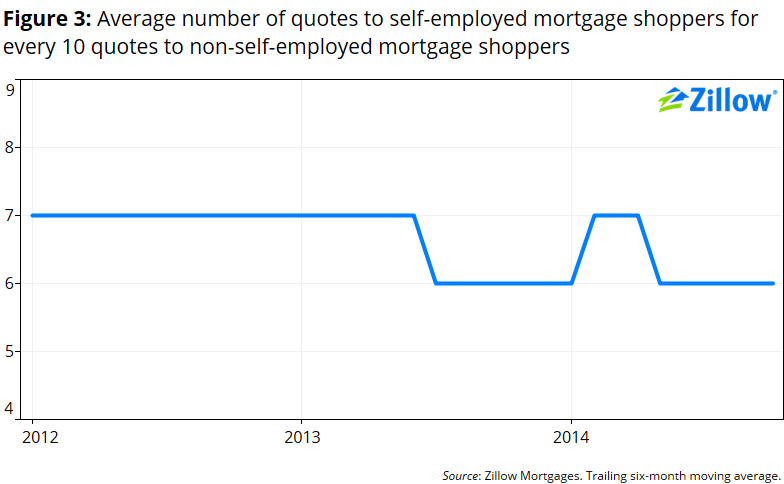

- But self-employed borrowers receive only six or seven quotes for every 10 mortgage quotes received by non-self-employed borrowers.

Self-employment offers enormous potential rewards. Some of the nation’s most successful entrepreneurs were successful precisely because they were willing to take on risks and venture out on their own to start new businesses. But these self-made entrepreneurs also represent an enormous risk for lenders, because while the self-employed tend to have higher incomes, their incomes can also be more volatile and difficult to document.

When it comes to buying a home, lenders frequently place great value on the predictability of income and the ability to document it. In addition, for some types of businesses—notably sole proprietorships and partnerships—personal and business liabilities can intermingle, making an individual’s financial fate vulnerable to the fate of their business. Because of these requirements and risks, the self-employed can encounter additional hurdles finding a mortgage.

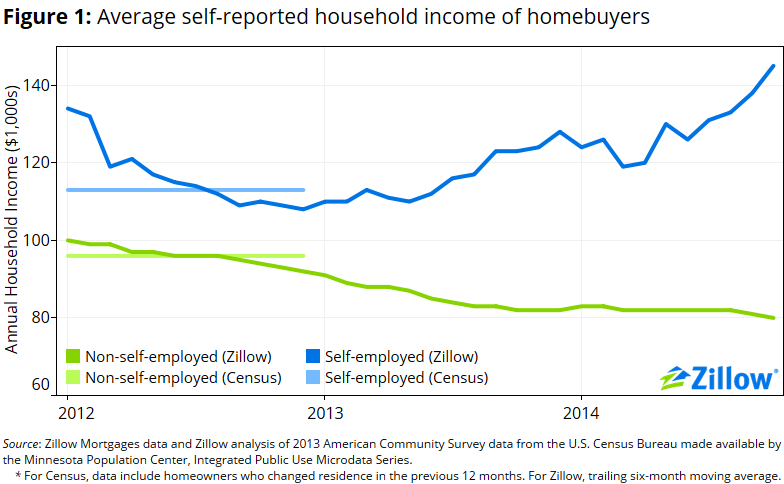

Self-employed borrowers shopping on Zillow tend to have higher incomes…

Self-employed mortgage shoppers on Zillow tend to have higher incomes than mortgage shoppers who are not self-employed. These findings were cross-validated by comparing data from home buyers inquiring about mortgage loans on Zillow to data reported by the Census Bureau’s 2013 American Community Survey.[1] The results from the two data sources are very similar.[2]

In October, self-employed mortgage shoppers reported an average household income of $145,000, more than 80 percent higher than the average household income of $80,000 reported by non-self-employed mortgage shoppers (Figure 1).

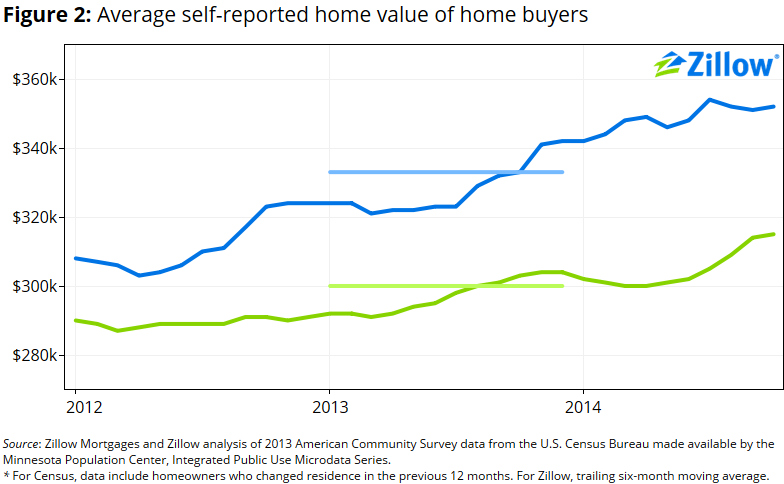

…And tend to seek more expensive homes…

In light of their higher incomes, it is perhaps unsurprising that self-employed mortgage shoppers tend to inquire about loans for more expensive homes (Figure 2). In October, self-employed borrowers sought loans for homes that cost about $351,000, compared to $315,000 for non-self-employed borrowers. Data from the ACS confirm that self-employed homebuyers tend to own more expensive homes than homebuyers who are not self-employed.[3]

..But receive less interest from lenders…

But despite their larger incomes and desire for larger loans, self-employed borrowers on Zillow tend to receive less interest from lenders. (Self-employed and non-self-employed borrowers tend to seek loans with very similar down payments.) For every 10 quotes received by a non-self-employed borrower, self-employed borrowers typically receive six or seven quotes (Figure 3).

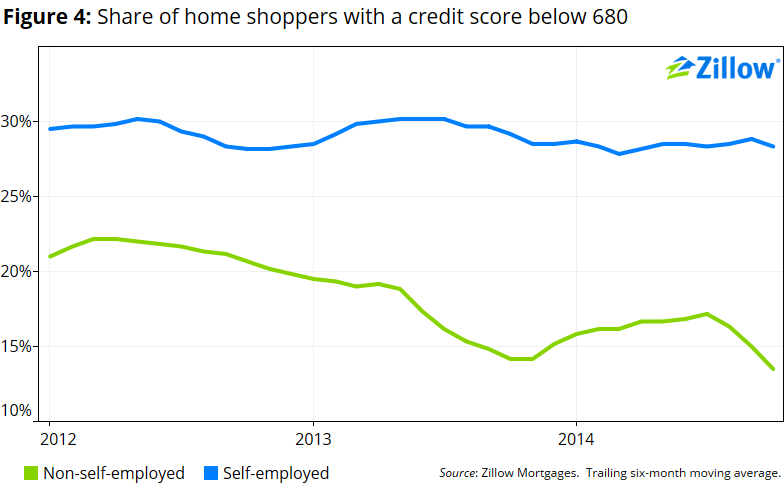

…Largely because of their credit scores.

Differences in credit backgrounds help explain a large portion of these differences. Self-employed mortgage shoppers are about twice as likely as non-self-employed shoppers to report a FICO score less than 680. In October, 28 percent of self-employed mortgage shoppers on Zillow reported a credit score less than 680, compared to 14 percent of non-self-employed mortgage shoppers (Figure 4). Controlling for credit score, the average number of quotes per loan request is very similar between self-employed and non-self-employed borrowers.

[1] Data made available by Steven Ruggles, J. Trent Alexander, Katie Genadek, Ronald Goeken, Matthew B. Schroeder and Matthew Sobek, Integrated Public Use Microdata Series: Version 5.0 [Machine-readable database] Minneapolis: University of Minnesota, 2010.

[2] For mortgage shoppers on Zillow, we report a trailing six-month moving average of household income. All analysis of Zillow data is for purchase loans only. For the American Community Survey (ACS) data, we report average household income of homeowner households who changed residence during the previous 12 months. Since the questions were administered in 2013, they correspond to household who bought homes during 2012.

[3] Similar to income, we report a trailing six-month moving average for home values in the Zillow data. For the ACS data, home values correspond to the estimates value of their current residence (which was purchased within the past year) so the data correspond to the year of the questionnaire—2013.