Rising Single-Family Rentals Dampening Home Sales

Hundreds of thousands of homes that may have otherwise sold in a typical year over the past decade – particularly more-affordable homes – have instead been taken off the market and converted to single-family rentals, a trend that exploded in popularity in recent years and is only now beginning to level off.

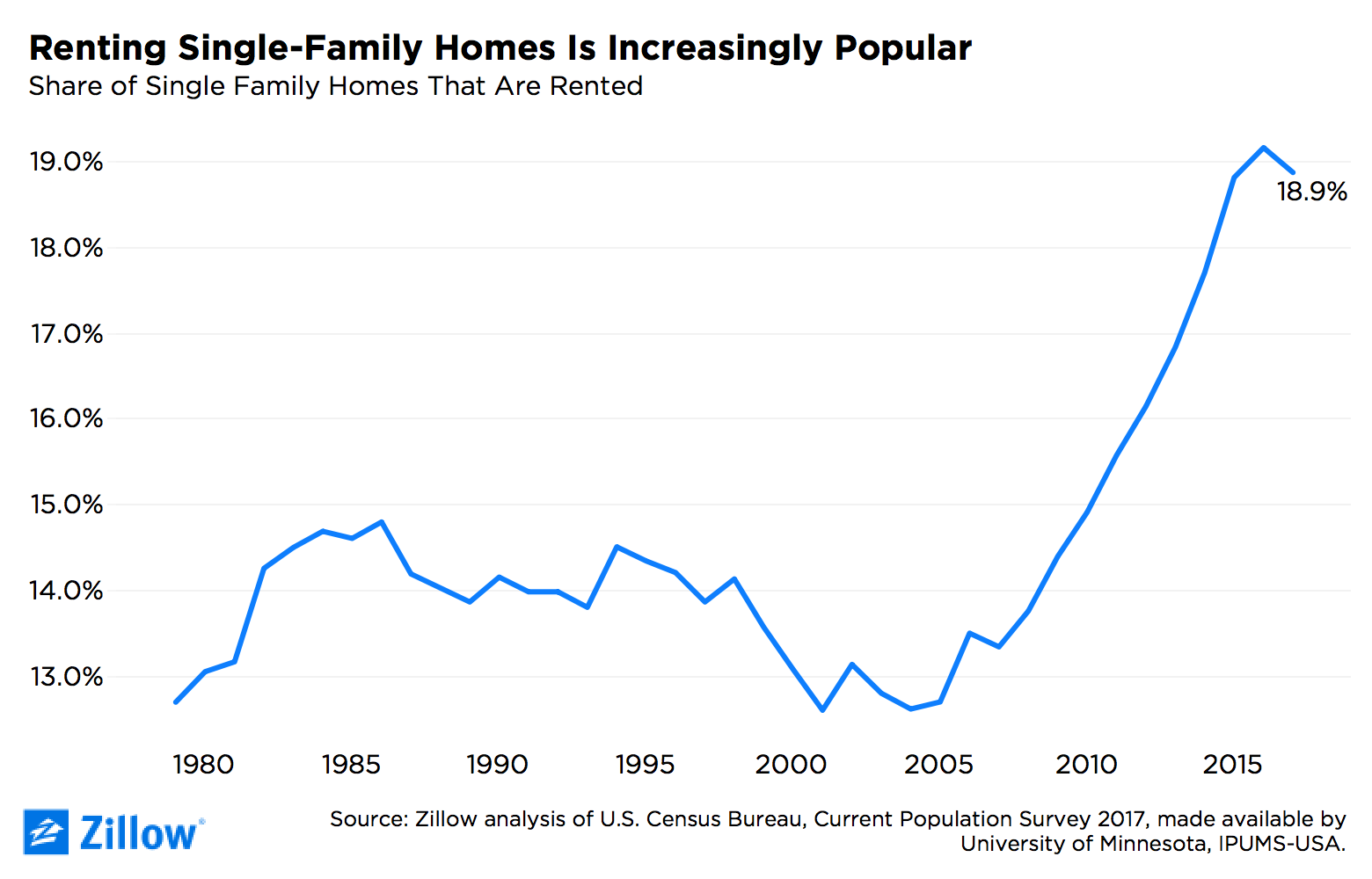

- After growing steadily for a decade, the share of single-family homes that are rented stabilized in early 2017.

- The typical SFR rental is worth $215,300, slightly more than the median-valued home nationwide, largely because rented SFR homes tend to be more concentrated than other SFRs in suburban communities.

- Compared to other homes in their metro areas and zip codes, SFR rentals tend to skew toward the lower end of the housing market.

- Assuming that about 5 percent of homes typically sell in a given year (roughly in line with historical norms), single-family home rentals over the past decade have lowered annual home sales by about 270,000 units, or about 5 percent of the 5.4 million units that have sold in a typical recent year.

Hundreds of thousands of homes that may have otherwise sold in a typical year over the past decade – particularly more-affordable homes – have instead been taken off the market and converted to rentals, a trend that exploded in popularity in recent years and is only now beginning to level off.

The share of single-family homes that are rented fell in early 2017, the first decline in a decade, according to the U.S. Census Bureau.[1] After increasing steadily from 13.4 percent in 2007 to 19.2 percent in 2016, the share edged down to 18.9 percent in early 2017 but remains near its highest levels since the data begin in 1979.

Several related trends are driving this phenomenon:

- During the housing bust, some homeowners lost their homes to foreclosure contributing to falling home values across the country. At the same time, the U.S. renter population grew rapidly.

- This combination of growing demand for rentals and falling home values provided an attractive opportunity for investors looking for properties they could buy at a discount and turn into rentals to meet the demand.

- In some communities hit hard by the housing bust, investor activity provided much needed demand and helped stem the free fall in home values and turn around the market.

- Today, as home values continue to recover around the country and rental demand remains strong, investors large and small continue to realize attractive returns holding homes as rental properties.

Location, Location

Nationwide, the median single-family rental is valued at $215,300, slightly above the national median home value of $201,900.[2] However, this is primarily driven by the markets where they are located. Single-family rentals (SFR rentals) are more likely than other SFRs to be in somewhat pricier suburban communities: 77.2 percent of rental single-family homes are in suburban communities and 9.4 percent are in rural communities. Among all single-family residences nationwide, 62.3 percent are in the suburbs and 29.5 percent are in rural communities. But compared to other homes in the ZIP codes where they are located, SFR rentals tend to valued 2.3 percent (about $4,500) less overall, and 1.5 percent less on a per-square-foot basis.

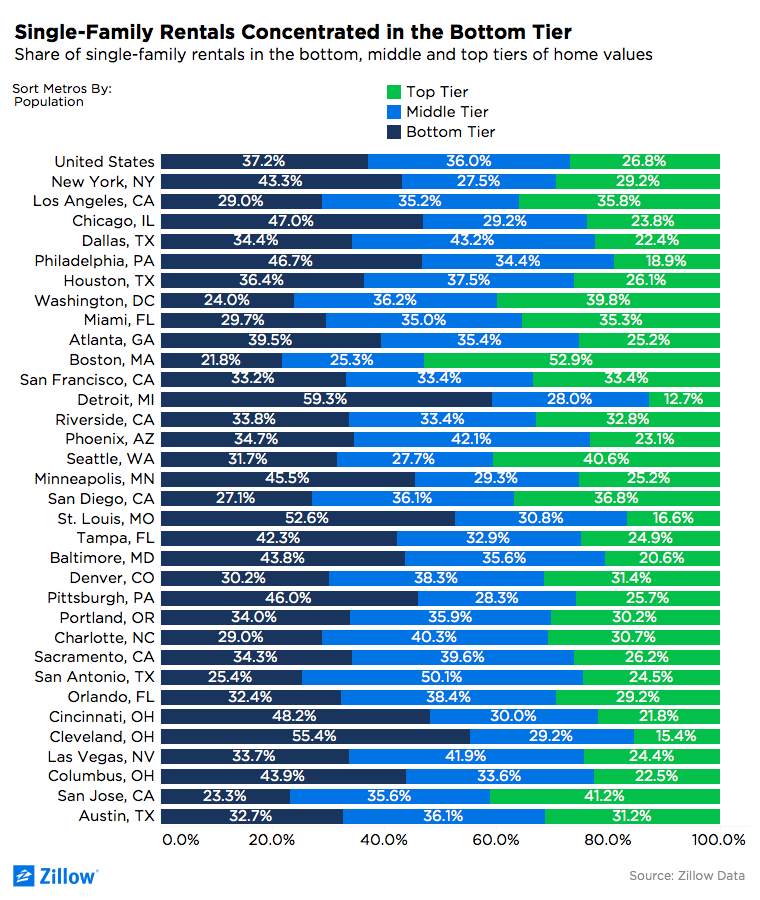

If single-family rentals perfectly mirrored the overall housing stock, one-third (33 percent) would fall into each home value tier. But overall, SFR rentals skew toward the lower end of the housing market. Nationwide, 37.2 percent of single-family home rentals are homes valued in the bottom-third of home values; 36 percent are valued in the middle-third of home values. The remaining 26.8 percent are in the top-third of homes ranked by home value.

As with most things in real estate, there are differences across markets. Looking at the 35 largest housing markets, Detroit, Cleveland, St. Louis, Cincinnati, and Chicago have the highest shares of SFR rentals in the bottom third of the market. San Antonio, Dallas, Phoenix, Las Vegas and Charlotte have the largest shares of SFR rentals in the middle third of the market. Boston, San Jose, Seattle, Washington (DC) and San Diego have the highest concentration of single-family rentals in the top third of the housing market.

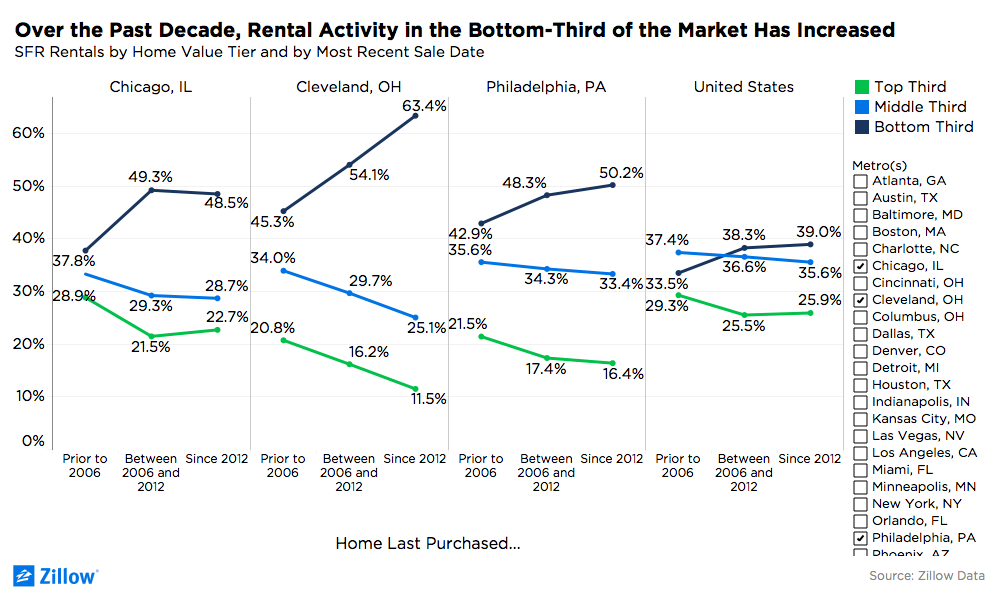

Over the past decade, rental activity in the bottom-third of the market has increased. Comparing single-family rentals by when they were last sold, 39 percent of SFR rentals purchased by their owner since 2012 are in the bottom third of the market, compared to 33.5 percent of single-family rentals last sold prior to 2006.[3]

More Single-Family Rentals, Fewer Sales

Together, the Zillow and Census data suggest that between 2006 and 2017, about 5.4 million single family homes transitioned from the owner-occupied to the rental stock. Among these homes, 2.4 million (45 percent) were homes in the bottom third of the housing market by home value, 1.8 million (33 percent) were in the middle third, and 1.2 million (22 percent) were in the top third of the housing market.

Assuming that about 5 percent of homes typically sell in a given year (roughly in line with historical norms), this would imply that the growth in single-family home rentals over the past decade have lowered annual home sales by about 270,000 units, or about 5 percent of the 5.4 million units that have sold in a typical recent year.[4] This includes about 121,000 units in the most affordable third of the market and 59,000 in the most expensive third of the market.

[1] Zillow analysis of data from the U.S. Census Bureau’s Current Population Survey, Annual Socio-Economic Supplement, March 1979 to March 2017.

[2] As of August 2017. This analysis includes only single-family homes that have ever listed for rent on Zillow, a relatively small portion of the overall single-family home rental market. The tier cutoffs are based only on single-family homes.

[3] These breaks correspond roughly to thirds of the distribution of single-family rentals by year of last sale.

[4] The calculations in this paragraph are approximate and should be interpreted as suggestive rather than definitive.

{kind=link}