- Differences in mortgage products and down payments could influence the number of quotes received and annual percentage rate (APR) charged to subprime and prime borrowers.

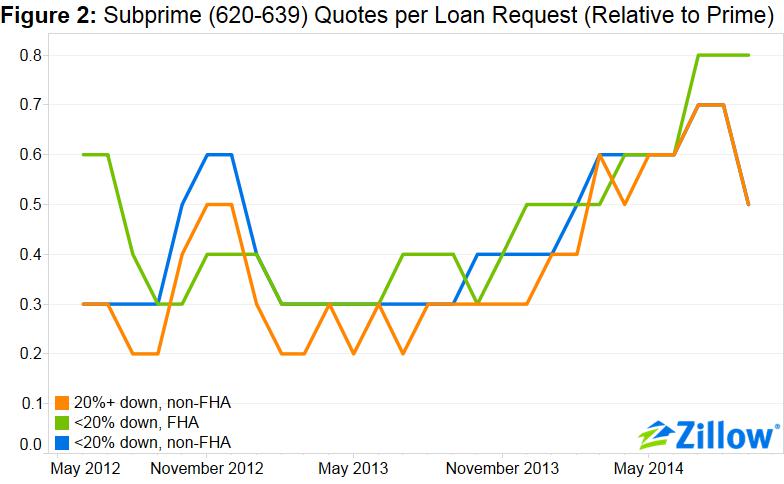

- Subprime borrowers are receiving an increasing number of quotes on Zillow, even after controlling for product and down payment.

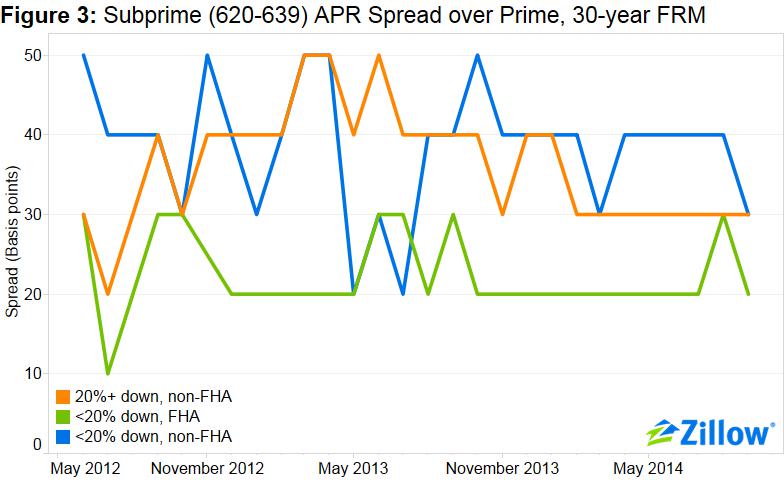

- The APR charged to subprime borrowers has been roughly flat after controlling for product and down payment.

Recent studies, including our own previous research, show a gradual and modest easing of credit to borrowers with lower credit scores. But are these trends being driven by differences in the mortgage products and down payment amounts chosen by low-credit-score borrowers?

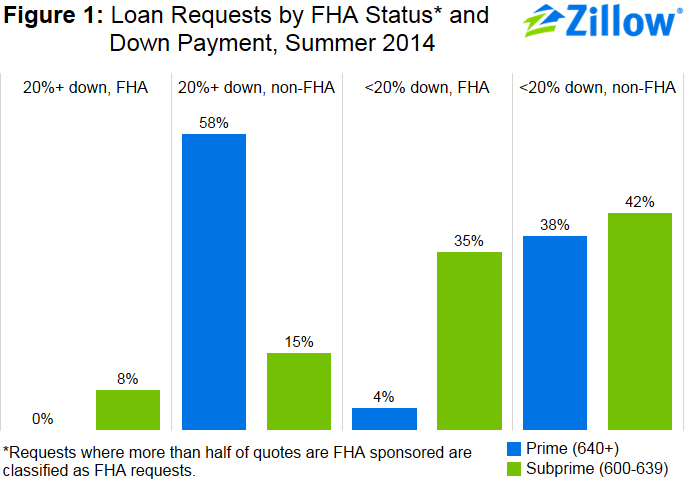

Compared to borrowers with higher credit scores, borrowers with low credit scores (as measured by their FICO score) tend to seek loans requiring smaller down payments and are more likely to receive quotes for loans backed by the Federal Housing Administration (FHA) (figure below).[1] These differences could drive some of the observed increase in quotes per loan request, as well as differences in the subprime annual percentage rate (APR) and prime APR noted in our previous analysis.[2]

Quotes per loan request

Controlling for FHA status and down payment, the gradual easing of credit to low-FICO borrowers that started earlier this year becomes more apparent. Relative to the number of quotes received by prime borrowers for similar products and down payments, borrowers with low FICO scores are increasingly attracting attention from lenders.

For instance, for every 10 quotes received by a prime borrower for an FHA-sponsored, 30-year, fixed-rate loan with a down payment of less than 20 percent, upper-tier subprime borrowers (FICO scores between 620 and 639) received eight quotes, twice the rate of a year ago. Upper-tier subprime borrowers seeking a non-FHA loan received about five quotes for every 10 received by a prime borrower in September, regardless of down payment, down from August but up from about three a year ago.

Interest rate spread

Examining the APR charged to subprime borrowers relative to the APR charged to prime borrowers, the spreads seem relatively flat in recent months after controlling for product and down payment.

Conclusion

As interest rates begin to rise from their historic lows, housing market activity has begun to slow with mortgage applications and refinancing activity down sharply over the past two years. Credit remains tight relative to most historic standards. Some market observers argue that the housing market will only sustainably recover once borrowers with riskier credit profiles are again able to access loans. The data presented above suggest that this is gradually beginning to occur.

[1] Borrowers must specify a down payment but can receive quotes for both FHA-sponsored and private loans. We classify as FHA loan request cases where more than half of the quotes received by a borrower are for FHA-sponsored loans. These data include only 30-year fixed rate mortgage loans for a home purchase.

[2] Given their small sample size, we drop borrowers seeking FHA loans with high down payments from the subsequent analysis. These loans accounted for 8 percent of all subprime loans and 0.04 percent of all prime loans in summer 2014.