Last week the New York Times Magazine ran a story, “Are Subprime Mortgages Coming Back?” (Sept. 9, 2014), arguing that subprime mortgage lending has unfairly received a bad reputation in the wake of the Financial Crisis and that in many instances, loans that are classified as subprime allow households that do not meet traditional (some would argue outdated) lending criteria to become homeowners.

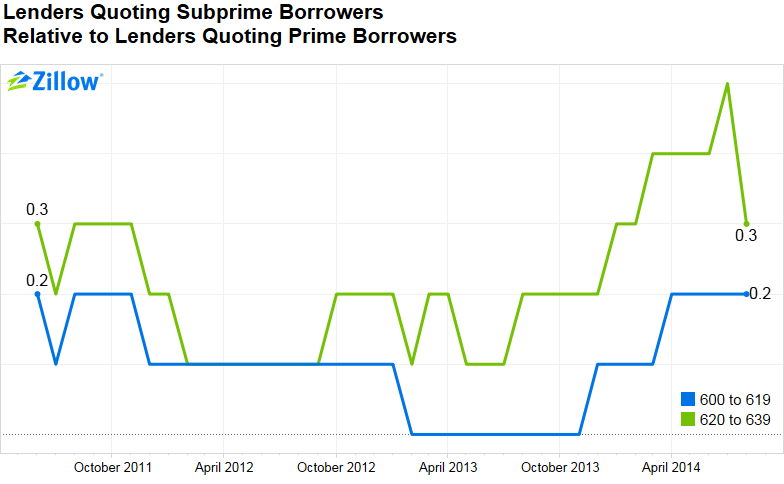

Several months ago we looked into this question using a unique Zillow database of online mortgage loan requests and responses (“Supply and Demand Dynamics in Subprime Mortgage Markets,” June 30, 2014). We recently updated this analysis through August 2014. For the most part, the story has not changed. The average number of quotes offered to the upper tier of subprime borrowers (those with credit scores between 620 and 639) continued to increase through the summer although it pulled back in August (chart below). By contrast, the average number of quotes offered to the lower tier of subprime borrowers (those with credit scores between 600 and 619) was still higher than a year earlier but was largely flat over the summer. Currently, for every 10 quotes received by a prime borrower, an upper-tier subprime borrower will receive three and a lower-tier subprime borrower will receive two.

(Note that these series are for slightly different credit groups and include slightly different controls than our earlier analysis.)

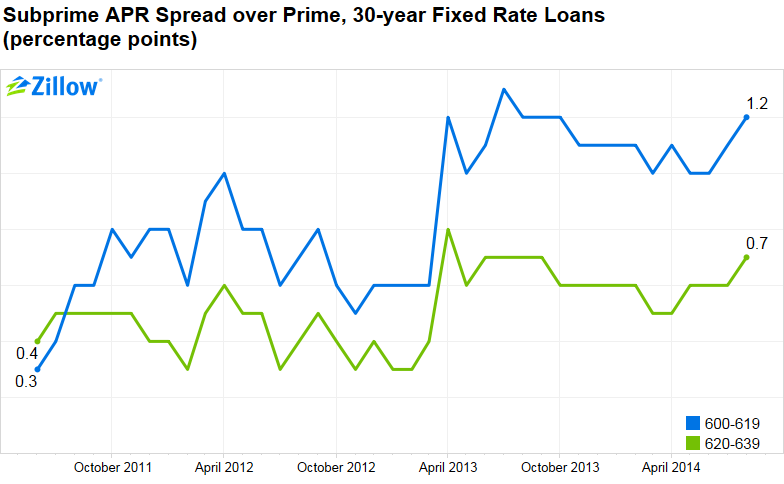

Similarly, premiums charged to subprime borrowers remain higher than in 2011 and 2012, but have been mostly flat in recent months (chart below). For a 30-year fixed rate purchase mortgage, upper-tier subprime borrowers pay 70 more basis points while lower-tier subprime borrowers pay 120 more basis points.

Of course, other considerations beyond credit score go into the determination of whether a borrower requires a subprime loan—for instance, documentation and regularity of income. However, overall, the data above suggest that credit continues to slowly and gradually ease for the upper tier of borrowers with credit scores that historically were labeled subprime.