Since the financial crisis began in 2007, borrowers with low credit scores have largely been excluded from mortgage markets. In contrast to the years preceding the crisis, these borrowers—traditionally labeled “subprime” borrowers—have had an exceedingly difficult time obtaining mortgage credit. (The boundary between “prime” and “subprime” borrowers is fluid, and there are a number of more nuanced gradations. In this analysis, we identify “subprime” borrowers as having a credit score below 640. The results do not meaningfully change if the dividing line is increased to 660, another common threshold.)

Recent media reports suggest, however, that some lenders began cautiously relaxing standards for some higher-end subprime borrowers in early 2014. The more sensational of these stories have pointed to demand-side explanations—describing the trend as a return to the lax lending standards that prevailed prior to the financial crisis, in response to pent-up demand from borrowers who defaulted during the worst years of the crisis.[1] By contrast, other reports have pointed to supply-side explanations—principally tightening profit margins and lower mortgage origination volumes (especially refinance mortgages) leading banks to seek new revenue growth by extending credit to riskier borrowers.[2] More nuanced reports distinguish the risks and safeguards associated with loans now available to borrowers with poor credit histories from loans made to these borrowers prior to the crisis.[3]

Using a unique database of loan requests and responses through Zillow— an online marketplace that connects thousands of mortgage borrowers and lenders each day—we use three sets of metrics to assess the underlying demand and supply dynamics driving subprime mortgage markets over the period covering June 2011 through April 2014, and weigh the relative merits of the two narratives that have emerged in recent months:

- As an indicator of demand for mortgage loans across credit groups, we look at the number of unique borrowers requesting loans on Zillow;

- As an indicator of supply for mortgage loans across credit groups, we look at the number of lenders quoting borrowers; and

- As an indicator of the conditions associated with new mortgage loans across credit groups, we look at the average annual percentage rate (APR) on loans offered.

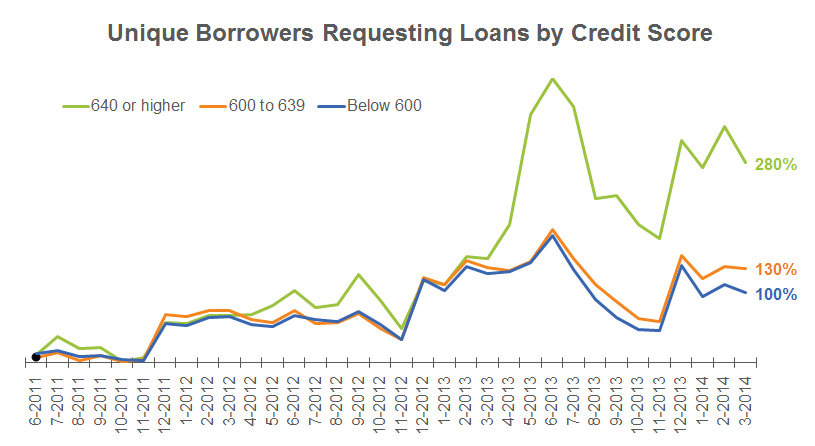

As the chart below illustrates, the number of unique borrowers seeking loans on Zillow displays some seasonality—rising during the spring/summer home shopping season—but has grown for all credit groups as increasing numbers of home shoppers seek mortgage loans online. However, demand has grown most dramatically among borrowers with higher credit scores (640 or higher), nearly tripling between June 2011 and April 2014. By contrast, demand among borrowers with slightly lower credit scores—those rated between 600 and 639 who are likely to benefit most if lending standards ease—has grown roughly in tandem with borrowers with credit scores below 600 who are largely excluded from mortgage borrowing regardless of the ease of credit.

With respect to mortgage loan supply, the number of lenders offering quotes through Zillow has grown over time and the number of lenders offering quotes to prime borrowers has always exceeded the number of lenders offering quotes to subprime borrowers. However, starting in late 2013-Q4 and accelerating in 2014-Q1, the number of lenders quoting borrowers with credit scores between 600 and 639 has started to catch up with the number of lenders quoting borrowers with credit scores above 640. As the figure below illustrates, by April 2014, for every 10 lenders quoting prime borrowers, six were quoting borrowers in the upper-tier of the subprime category. In contrast, the number of lenders quoting borrowers with the lowest credit scores, below 600, has essentially remained flat: Roughly two lenders are willing to offer quotes to the lowest subprime borrowers for every 10 that offer quotes to prime borrowers.

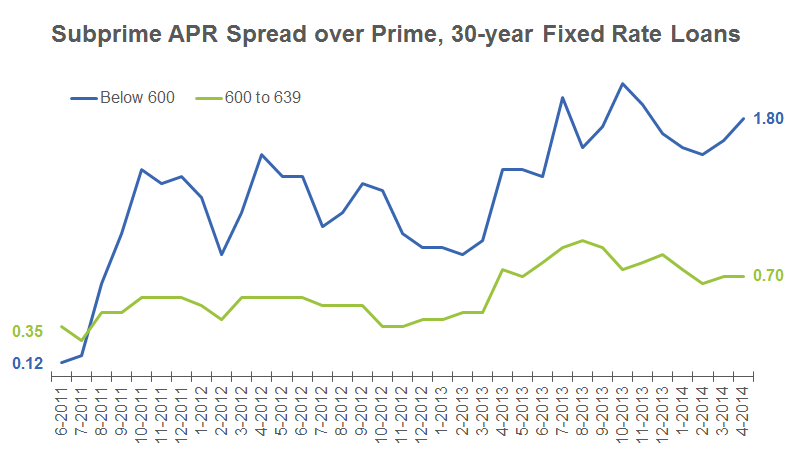

To assess the conditions associated with new mortgage loans, we compare the APR associated with 30-year fixed rate loans quoted to prime borrowers with the APR associated with loans to subprime borrowers. The difference between the two rates is known as the “spread,” with rates for subprime borrowers above rates for prime borrowers. By presenting the rates as a spread, we control for broader macroeconomic trends influencing mortgage rates. As the figure below illustrates, the premium that lenders are charging to subprime borrowers with credit scores between 600 and 639 has trended upward, roughly doubling from 35 basis points to 70 basis points over the past three years. (The premium charged to subprime borrowers with the lowest credit scores, below 600, has increased even more sharply, but should be interpreted with caution as these borrowers represent such a tiny fraction of all loans.)

These findings differ somewhat from the results of the Federal Reserve Board’s Senior Loan Officers Opinion Survey (SLOOS), which pointed to a slight tightening of standards for subprime mortgage loans in the first half of 2014. The SLOOS findings are based on a sample of seven responses from senior financial officers, while our results are based on approximately 16 million unique loan requests with responses from nearly 1,500 mostly small lenders over the course of 30 months. However, in aggregate, the data presented above suggest that over the past year, demand for subprime mortgage loans has been essentially flat; any expansion in credit to subprime mortgage borrowers has been driven primarily by supply-side considerations—some lenders actively displaying interest in borrowers with less than pristine credit histories, albeit for a growing interest rate premium.

[1] For example, Les Christie, “Subprime mortgage making a comeback,” CNNMoney, March 21, 2014.

[2] For example, Gillian Tett, “American subprime lending is back on the road,” Financial Times, April 10, 2014, and Suzanne McGee, “Banks return to risky business: lax standards and subprime loans,” The Guardian, April 24, 2014.

[3] For example, Nick Timiraos, “Another ‘Subprime’ Adventure? Behind Wells Fargo’s Move To East Mortgage Lending,” The Wall Street Journal, February 20, 2014.