When Up Means Down: What Happened with Mortgage Interest Rates After the Fed’s Hike?

Why, when key benchmark interest rates as set by the Federal Reserve rose, did mortgage interest rates fall? The answer is two-fold.

Why, when key benchmark interest rates as set by the Federal Reserve rose, did mortgage interest rates fall? The answer is two-fold.

In mid-March, the Federal Reserve announced a much-anticipated increase in key short-term interest rates. Generally, this kind of announcement would have caused mortgage interest rates charged by home lenders to also increase – or at least remain flat. But instead, mortgage rates fell.

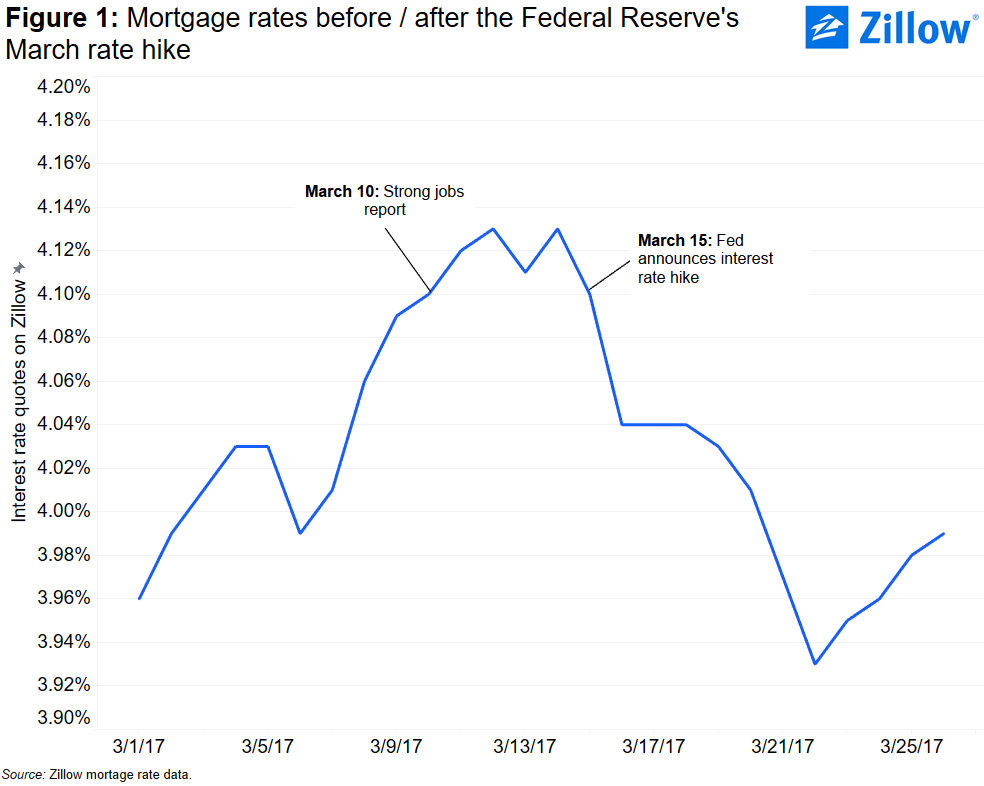

And mortgage rates didn’t just dip slightly. Rates on conventional 30-year, fixed-rate mortgages as quoted on Zillow (the type of mortgage used by the majority of U.S. homebuyers) fell almost 10 basis points following the Federal Reserve’s rate hike. The proceeding drop represented the fastest pace of decline this year, and erased the gains that followed a strong jobs report earlier in March (figure 1).

So what gives? Why, when key benchmark interest rates as set by the Federal Reserve rose, did mortgage interest rates fall? The answer is two-fold.

First, most lenders were already very confident that the Federal Reserve would raise rates, and so corresponding rate increases were incorporated into market pricing even before the Fed officially announced their rate hike. On March 10, a strong jobs report solidified expectations that the Federal Open Market Committee (FOMC) – the branch of the Federal Reserve Board in charge of determining monetary policy, including interest rates – would increase rates. Because the Fed’s rate hike was already priced into mortgage quotes offered to borrowers, there was little need for lenders to increase their interest rates even more.

The second driving force behind the seemingly contradictory swings in interest rates was increased uncertainty about the Fed’s confidence in the U.S. economy. Prior to the announced Federal Reserve rate hike, markets expected a unanimous Fed would implement a more aggressive schedule for future rate hikes than in 2016. Markets were already beginning to account for the likelihood of more rate hikes to come in longer-term bond markets, which often dictate mortgage rates. But in a surprise, Federal Reserve Bank of Minneapolis President Neel Kashkari voted against the hike, injecting a small amount of pessimism among those trying to gauge the Fed’s overall feelings on the strength of the economy as a whole and the possibility of future rate hikes to come.

This one-two punch of lenders having already priced higher Federal Reserve interest rates into mortgage rates and the small but largely unexpected sign of less-than-full confidence in the economy as displayed by Kashkari had the effect of pushing mortgage rates down, and not up.

Related:

{kind=link}