Younger Homeowners Are More Likely to Have to Pay for Private Mortgage Insurance

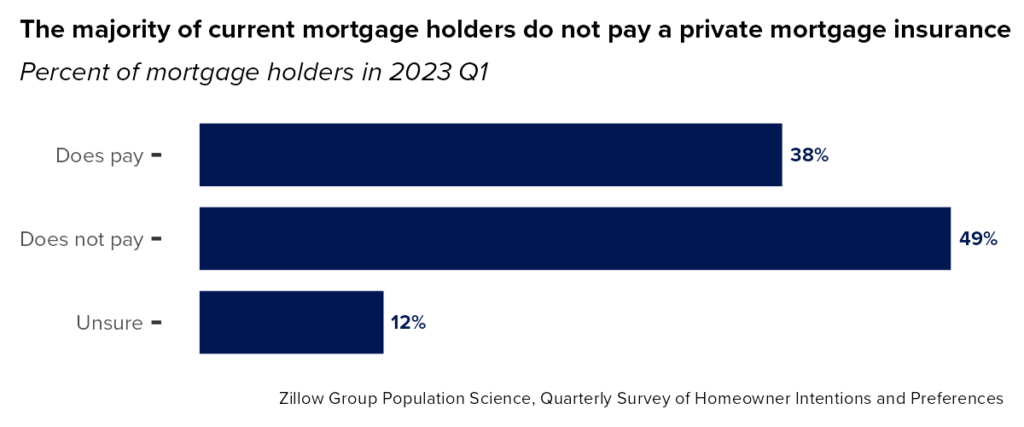

When prospective homebuyers are purchasing their new home, they may find themselves paying for private mortgage insurance. Private mortgage insurance, or PMI, is a common expense for home buyers who put down less than a 20% down payment on a conventional mortgage. PMI is insurance for the lender’s benefit and designed to safeguard the lender in case the borrower is unable to make their mortgage payments. Though lenders commonly ask for PMI, 12% of current homeowners do not know whether they pay for this mortgage insurance.

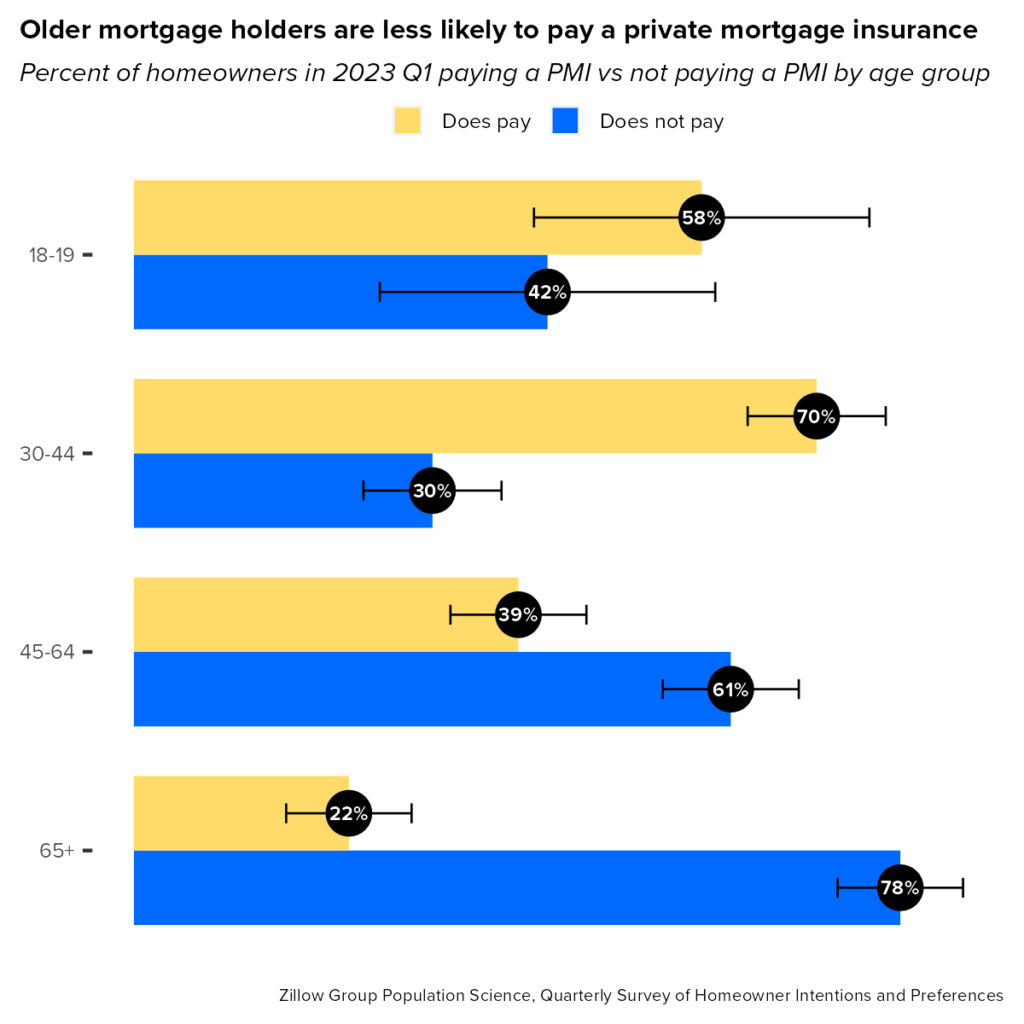

Of the 88% who do know, older mortgage holders were less likely to pay a PMI. In Q1 2023, only 22% of mortgage holders older than 65 paid a PMI, compared to 70% of mortgage holders ages 30 to 44. [1] Since homeowners with a PMI pay a monthly premium of about $30 to $70 a month for every $100,000 borrowed, younger homeowners are having to pay more on their mortgage than older homeowners.

This could be due to a variety of factors. Since PMI is often an expense for homeowners who purchase a home with less than a 20% down payment, the amount a homeowner is able to pay upfront will determine their accrued costs over time. Even accounting for income and length of ownership, older homeowners have had a longer time to accumulate savings (wealth) to put down a larger down payment. Similarly, older homeowners are more likely than younger ones to have owned a home previously (another source of wealth accumulation) and might be able to use their equity from a previous home on the down payment of their current home.

[1] Additional (regression-based) analyses show that age differences persist even accounting for differences in length of ownership, income, and homeowners’ current mortgage rate.

{kind=link}