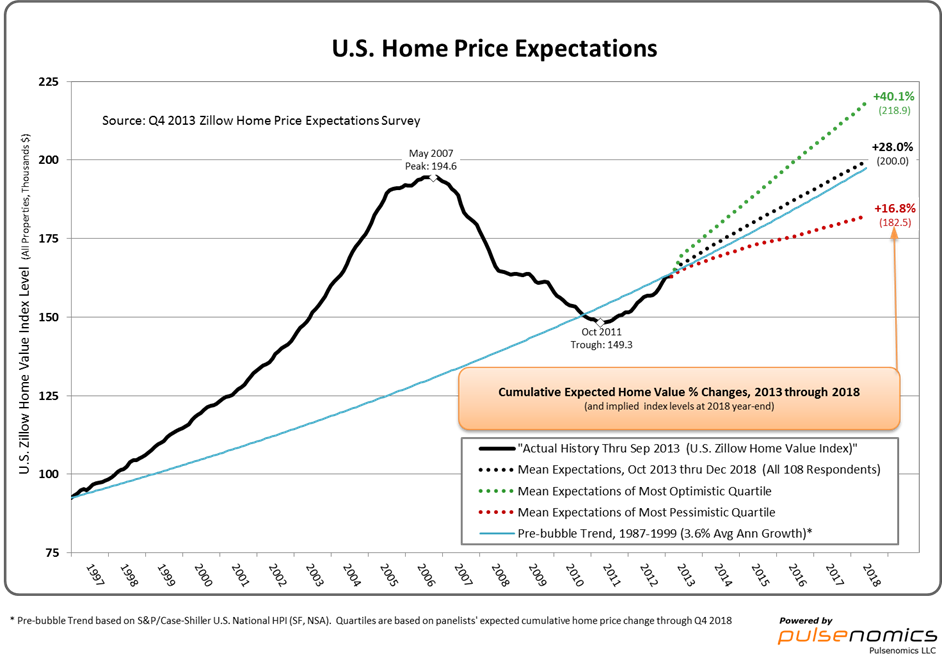

Our most recent Zillow Home Price Expectation Survey (ZHPES) results were released last week on Nov. 7. The survey asks professional forecasters to provide predictions for housing market growth in the near term. The average prediction for annual appreciation in 2013 is 6 percent, down from 6.7 percent the last time the survey was conducted in August. The lowest projection predicted 1.4 percent depreciation for 2013 and the highest predicted 15.6 percent appreciation. This edition of the survey was compiled from 108 responses, including the projections of economists, market and investment researchers and real estate experts.

For 2014, the panel predicted, on average 4.3 percent annual appreciation in home values with a low of 5 percent depreciation and a high of 8.4 percent appreciation. For 2015, the average predicted appreciation is 3.8 percent, and for 2016 it drops to 3.5 percent. Overall, in the next five years, experts predict 4.2 percent annual appreciation, which amounts to a total 28 percent gain in home values.

Figure 1 shows the predicted appreciation in home values through 2018 by quartile. The survey mean predicts above average home price appreciation until the end of 2018, when the median U.S. home value is expected to be $200,000. The survey predicts that national home values will surpass their 2007 peak in 2018. The most pessimistic survey quartile expects home values to be $182,500 by the end of 2018, a 16.8 percent gain from current values. The most optimistic quartile expects home values to rise to $218,900, 40.1 percent above today’s levels.

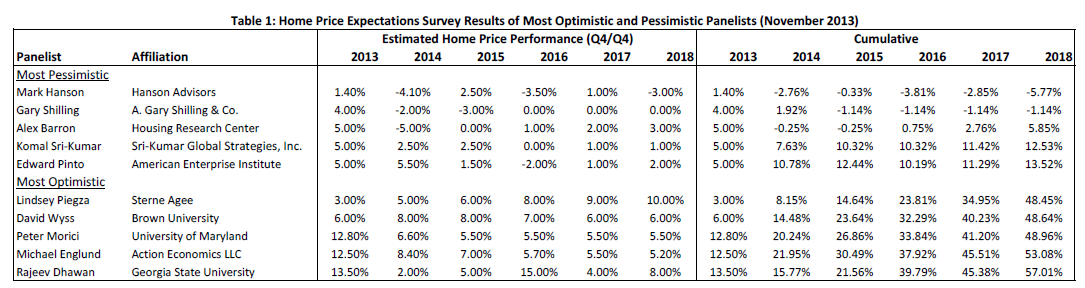

Table 1 shows the most optimistic and pessimistic predictions by cumulative appreciation through 2018. The most pessimistic forecast was from Mark Hanson of Hanson Advisors, who was also the most pessimistic last quarter. The most optimistic forecast was from Rajeev Dhawan of Georgia State University.

Table 1 shows the most optimistic and pessimistic predictions by cumulative appreciation through 2018. The most pessimistic forecast was from Mark Hanson of Hanson Advisors, who was also the most pessimistic last quarter. The most optimistic forecast was from Rajeev Dhawan of Georgia State University.

A number of public and private plans for overhauling the nation’s mortgage finance system and reforming government-sponsored enterprises Fannie Mae and Freddie Mac have been proposed, all of which seek to reduce and redefine the government’s role in the mortgage market to some degree. As these policy conversations begin, panelists were asked how involved they think the federal government should be in any re-imagined mortgage system. Among those panelists expressing an opinion, the majority (58.4 percent) said the federal government’s involvement in the conforming mortgage market should be “somewhat significant,” “significant” or “very significant.” Only 8 percent of respondents said the federal government should have a “non-existent” role in the conforming market.

Panelists were also asked to define an appropriate level of government-backing for mortgage loans going forward. Among those panelists expressing an opinion about what maximum percentage of all new mortgages should be backed by the federal government, the median response was 35 percent, roughly the level seen in 2006 at the height of the housing bubble.