How Much Is a Down Payment on a House?

Written by Jessica Rapp on April 19, 2024

Key takeaways

- Many buyers put 20% down to avoid private mortgage insurance (PMI), but minimums can be as low as 3% with certain loan programs.

- The majority of buyers save up for a down payment over time.

- A larger down payment can lower monthly payments and interest costs over time.

The typical down payment on a house is between 3% and 20% of the purchase price. The amount you’ll be required to put down may vary depending on the loan program you use to finance the home purchase. Government-backed loans like USDA and VA allow down payments as low as 0%. On the other end of the spectrum, jumbo loans may require minimum down payments of 10% or more.

According to a 2022 Zillow survey, the median home buyer put down 10-19% of the final purchase price on a home. To help visualize how much you’ll want to put down on a home and how that affects what home price you can afford, try our Down Payment Calculator. It considers your annual income, monthly debts, the interest rate on your mortgage, your loan term and other factors that may influence how much you’ll need to put down on a house.

What is a down payment?

A down payment is the cash payment you make at closing toward the purchase of a home. For most people, you combine your down payment with a loan to cover the total purchase price of the home. Down payments are expressed as a percentage of the total purchase price. For example, a $30,000 down payment on a $300,000 home purchase would mean you’re making a 10% down payment. If you’re like the typical home buyer, you’d borrow the remaining $270,000 and pay it back over time with monthly principal and interest payments.

Do you have to put down 20% on a house?

A 20% down payment is ideal, but you do not need to put down 20% of the purchase price in order to buy a home. In fact, 58% of mortgage buyers in 2022 reported that they put down less than 20% on the home they purchased.

While not required, putting down 20% does provide a few key benefits, including:

- Lower monthly payments, since you’re borrowing less money overall

- Better interest rates and loan terms

- No monthly private mortgage insurance (PMI) costs when using a conventional loan

- A stronger offer in a competitive real estate market

- More equity in the home you’re buying

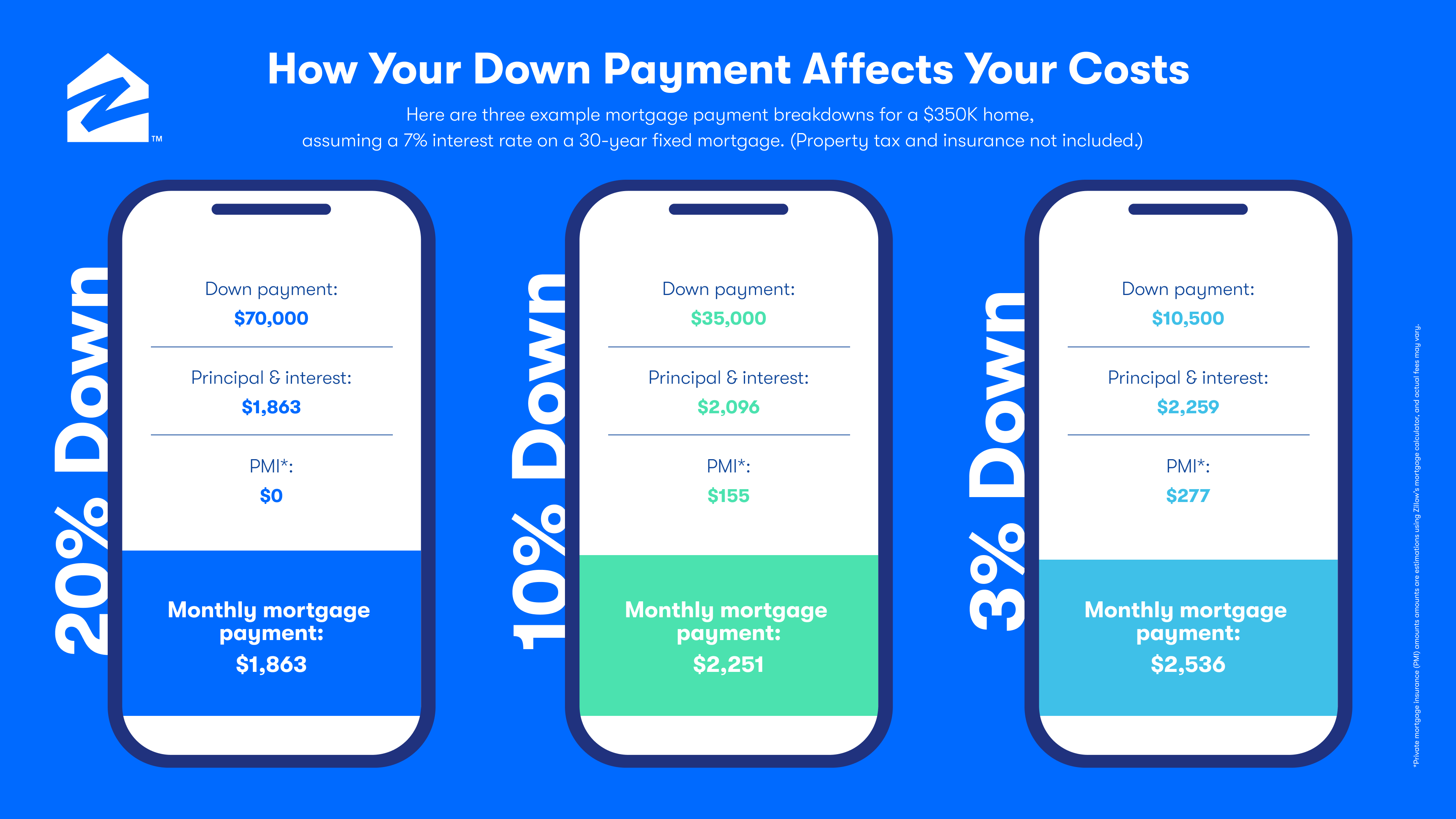

Take a look at the down payment difference between putting 5% down versus 20% down on a $350,000 home, assuming you use a 30-year fixed-rate mortgage with a 5% interest rate. A 20% down payment could potentially save you from spending over $700 a month more than if you'd put down just 5%.

Minimum down payment for a house

The minimum down payment required when buying a house depends on the type of home and the loan you're using to make the purchase. Some mortgage buyers may qualify for a government-backed home loan with 0% down, but the more common conventional loan usually requires a down payment of at least 3-5%. Down payments of 3% are more common among first-time homebuyers or credit-worthy, low-income borrowers who qualify for mortgage programs like HomeReady and HomePossible. All other borrowers typically must make at least 5% down payment on a conventional loan.*

The table below shows minimum down payment amounts for each major loan type when purchasing a primary residence, secondary home or investment property. Keep in mind that minimum down payment requirements can vary based on location, lender, loan type, credit history and more.

| Primary home | Second home | Investment property | |

|---|---|---|---|

| Conventional loan | 3-5%* | 10% | 20% |

| Jumbo loan | 20% | 25% | 25% |

| FHA loan | 3.5% | FHA loans can’t be used on second homes | FHA loans can’t be used on investment properties |

| VA loan | 0% | VA loans can’t be used on second homes | VA loans can’t be used on investment properties |

| USDA loan | 0% | USDA loans can’t be used on second homes | USDA loans can’t be used on investment properties |

How much should you put down on a house?

While the median mortgage buyer puts down 10-19% on a house, 16% of mortgage buyers in 2022 reported putting down just 3-5% of the final purchase price. The truth is there is no single right answer for every home buyer. When saving money for a house, consider how long it will take you to save for a down payment versus changes in the housing market and your overall timeline to get into a home. Even though a 20% down payment can lower your mortgage payments and save you some interest in the long run, that may not be a realistic goal for every home buyer. Spend some time playing around with a down payment calculator to find a scenario that works for you and your budget.

We sat down with Ashley Feinstein Gerstley, Founder and CEO of The Fiscal Femme, and asked this exact question, “How much should you put down on a house?” Listen to what she had to say in this quick video:

Keep these things in mind when considering how much you should put down on a house:

How much cash will you need to close? You’ll need cash to cover upfront costs like closing costs, prorated taxes, title fees and more.

Do you have money reserved for home maintenance and upkeep? You may want to leave some money for ongoing homeownership costs.

Will the home need repairs and upgrades? You may want to make some repairs or improvements on the home after you move in.

Do you qualify for down payment assistance? You may qualify for down payment assistance programs that can cover all or some of the down payment.

How to get a down payment for a house

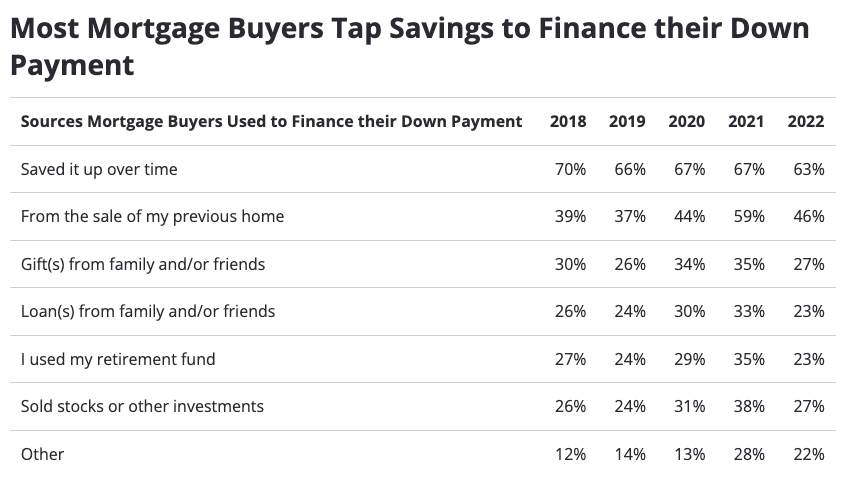

63% of mortgage buyers said they saved up for a down payment over time and 46% reported using money from the sale of their previous home.

While saving for a down payment can take time and discipline, some first-time home buyers have found success using more creative ways to fund their down payment like picking up a side hustle or setting aside tax return income each year. More traditional ways are also still common, including the use of financial gifts and selling stocks or other investments like retirement funds and crypto currency.

Source: Results from the Zillow Consumer Housing Trends Report 2022.

How much is a down payment for a $300k house?

When using a mortgage to buy a $300,000 home as a primary residence, here are the minimum down payment amounts you’d need based on each major loan type:

- Conventional loans require at least 3% down, putting your down payment on a $300,000 house at $9,000.

- FHA loans require a down payment of at least 3.5%, meaning you’d need to put down $10,500 on a $300,000 home purchase.

- USDA and VA loan down payments are typically 0%, so you likely wouldn’t need to put any money down on a house — regardless of the price. However, USDA loans do have loan limits on the amount you can borrow.

Buyers with lower credit scores may be required to make a higher down payment. The lender you choose to work with can help you weigh your options.

Can you get a loan for a down payment?

Loans can be used to cover down payment costs, if they are secured by personal or real property. Unsecured loans, like credit cards, cannot be used to cover a down payment. While this option used to be more commonly accepted among lenders, it is less common today and usually not done on a traditional home purchase.

Since the loan payment will be included when calculating your debt-to-income (DTI) ratio, using a loan to finance your down payment could impact your ability to qualify for a mortgage. You’ll also be required to document the secured loan in the promissory note to show proof that you’ll repay the loan. Nowadays, you may only see jumbo loan borrowers use a home equity loan against the property they are buying to skirt the minimum down payment requirements for their primary mortgage.

Can you buy a house with no money down?

There are a few zero down payment mortgages that will roll all costs into the mortgage, like VA and USDA home loans. These specific zero down programs are not available to everyone. You’ll need to meet certain eligibility requirements in order to qualify depending on the loan you’re interested in using.

Down payment assistance programs are also available to first-time home buyers and those who haven’t owned a home for at least the past three years. These programs are often offered by state, county or city governments that provide DPA support in the form of a grant or a second mortgage to cover the cost of the down payment, sometimes with benefits such as 0% interest and deferred payments.

When do you pay the down payment on a house?

Your down payment is collected along with closing costs on the date you close on your home. Your earnest money deposit will be counted as a portion of your down payment at that time.

Your title or closing agent is responsible for collecting and disbursing all funds to the appropriate parties during the closing process. This includes paying the seller the total purchase price of the home, that includes the down payment amount.

Do you need a down payment when refinancing?

No, you do not need a down payment when refinancing your mortgage. This is because you’ll already have equity in the home.

How much home can you afford?

At Zillow Home Loans, we can pre-qualify you in as little as 5 minutes, with no impact to your credit score.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Get pre-qualifiedHow much home can you afford?

See what's in reach with low down payment options, no hidden fees and step-by-step guidance from us at

Zillow Home Loans.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Calculate your BuyAbility℠

Loading

LoadingRelated Articles

Thinking about buying but not sure where to begin?

Start with our affordability calculator.

See what you can afford