What to Look for When Buying a House

Paying special attention to these 10 things could make home shopping easier.

Written by May Ortega on March 23, 2026

Edited by Jessica Rapp

Most home buyers start their search by admiring granite countertops and paint colors. But here's what you should really be looking at: the foundation, the roof, and the major systems that keep the home running. These are the factors that determine whether a house is a smart investment.

If you're looking to buy a home, here are the critical factors that can help you find one that will work for you now and later:

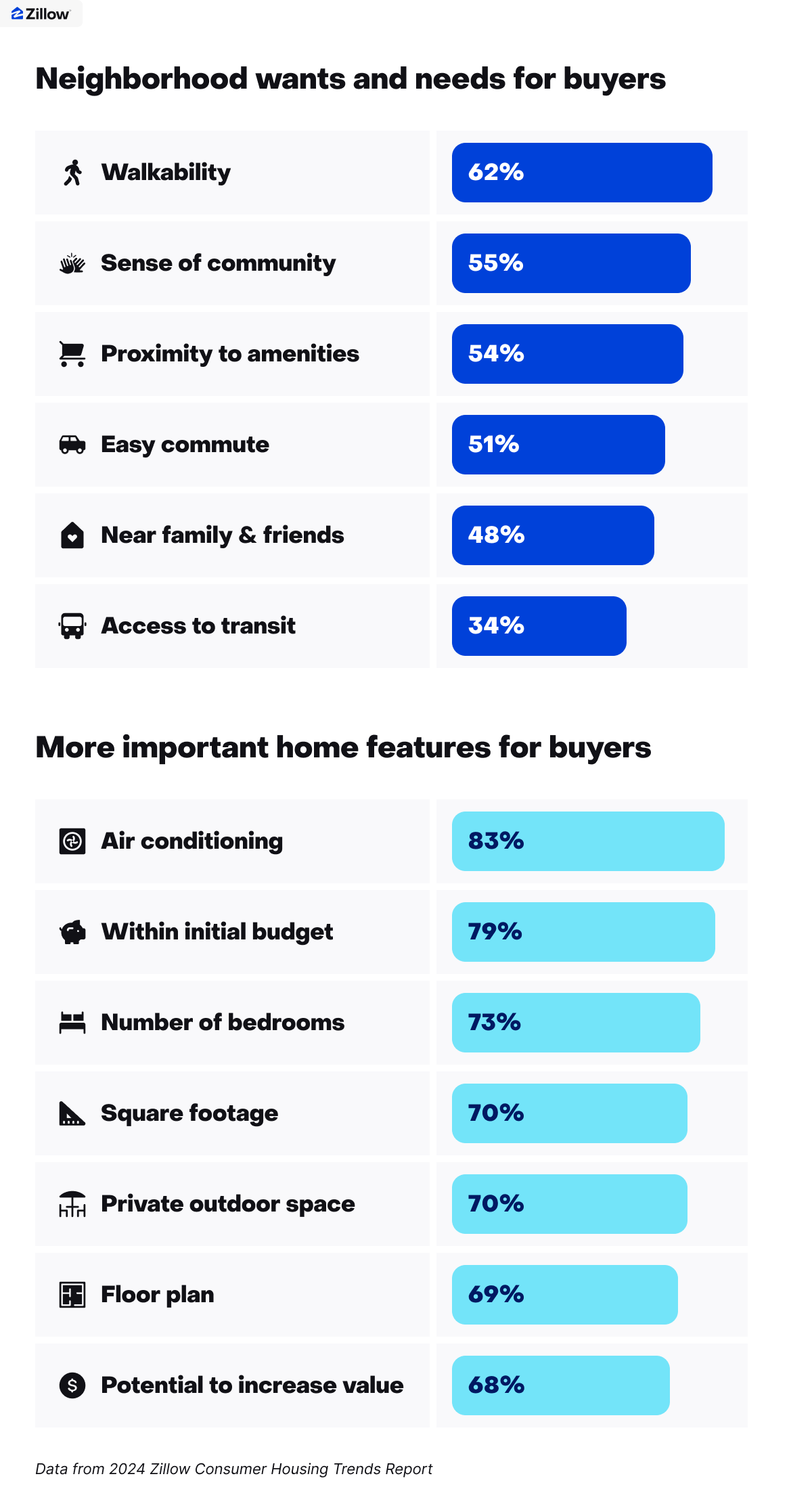

Top features buyers look for in a home

There are a lot of priorities to juggle when it comes to buying a home, but according to the Zillow Group Consumer Housing Trends Report 2024, some features stand out as very or extremely important to people looking to buy a home.

1. Price

Price will ultimately dictate what you can buy. While looking at homes above your price range can be fun and provide you with a sense of the market, it also can set you up for disappointment if you fall for a home outside your price range.

How to set your budget

Use Zillow Home Loan’s BuyAbility℠ tool. Discover your home buying budget based on your income, credit score, down payment and other details. Then find homes on Zillow that are within reach.

Get pre-approved. Zillow Home Loans can help you get pre-approved for a mortgage up to a specific amount that’s based on your income, debt, and credit history.

Forecast your mortgage payment. Use Zillow's Mortgage Calculator to estimate your monthly payments. The calculator adds in estimates for taxes, homeowners insurance, and any HOA fees to get an accurate figure.

Account for one-time fees. Budget for closing costs (typically 2-5% of the purchase price) and moving expenses, which can add thousands to your upfront costs.

Leave room for repairs. Even move-in ready homes may need updates or repairs within the first year. Budget an extra 1-3% of the home's value for unexpected fixes.

Pro tip: If you can't find or afford a home in your ideal neighborhood, tell your real estate agent what’s most important to you in your next home. They can help suggest locations you may haven’t thought of that will suit your lifestyle, needs, and budget.

2. Location

Location is one of the most important things to consider when buying a home.

Here's why location matters so much: while you can renovate a kitchen or add a bathroom, you can't change where the house sits.

What to look for in a location

Test your commute

- Drive or take public transit at your regular travel time to see what crowds and traffic are like.

- How busy is rush hour? Is the home close to major highways, bus stops, or train stations?

- Consider both current commute needs and potential future changes, like routes to schools or doctors’ offices.

Community attributes

If you want to walk to restaurants and shops, see if you'll be close enough by walking or biking the distance to town. Spend time exploring the area, and checking out nearby parks and attractions.

If you prefer solitude and don't mind driving more, consider homes that offer more privacy, maybe in areas off the beaten path.

School district quality

A parent looking for a new home may want to do everything they can to ensure the best possible education for their child, and choosing a home that feeds into schools that support that goal is part of the home buying process. You could visit local schools to find out if they fit what you’re looking for. You can also search by school on Zillow, which features GreatSchools ratings.

Flood zone status

Homes located in high-risk flood zones require special insurance coverage beyond the typical homeowners policy, which can add hundreds of dollars to your monthly costs.

Home orientation on property

Think about what the daily experience of living in the home might feel like. Does it get enough sunlight? Are you a comfortable distance from the neighbors? Consider the distance and difficulty of traveling from the driveway to the front door and whether seasonal changes will turn features like a steep driveway into a hazard.

3. Condition

If you're a first-time buyer who has never undertaken a home project, you may want to steer clear of a home in serious disrepair, also called a fixer-upper. The costs can add up quickly, and if the home needs structural work, it could delay your move-in.

At the same time, if you find a home in great condition with the exception of an outdated kitchen or bathroom, you could update the space while living there, or move out briefly while the work is being done.

Understanding property conditions

Move-in ready: A move-in ready home is new, close to new, or has been recently renovated. Such homes also may be called "turn-key."

Needs minor repairs: A home that needs minor updates might have cosmetic issues you'd like to change, or have some dated systems that could be updated for energy savings. If you're curious, consult a contractor to get an idea if upgrades are affordable for you.

Needs major repairs: A home in need of major repairs is often priced lower than other similar homes due to the money and time it will take to improve it. Consider that the return on investment for a major renovation isn't always 100% and extensive repairs could delay your move-in date.

Check condition of costly systems

Regardless of a home's condition, make sure your inspector checks major systems and mechanicals in the home to ensure they're in working order. If the inspector finds issues, consider negotiating with the seller to repair them, or ask for a credit so you can fix them yourself.

Be especially alert for the following issues, which can cost thousands to repair or replace:

- Damaged roof: Roof replacement can cost between $5,000-$17,400, according to home improvement website Thumbtack. This makes a roof replacement one of the most expensive repairs. Make sure you figure out the age and condition of the home’s roof.

- Older furnace or HVAC system: Ask about installation dates and expected lifespan. Test heating and cooling systems if possible. Thumbtack data shows HVAC replacement can run anywhere from $3,700 to $20,400 depending on the size and type of system.

- Flooding, water damage, or mold: Sometimes water damage is easy to spot, but it can also hide behind walls or ceilings. Check for signs of moisture issues which can lead to mold problems. When mold spreads, cleanup can get pricey.

- Old insulation which may contain asbestos: Homes built before 1980 may have insulation containing asbestos, which requires professional removal.

- Plumbing issues and leaks: Check water pressure, drainage, and look for signs of leaks. Ask about the age of the plumbing system and whether pipes are copper, PVC, or older materials.

- Exterior damage: Take a close look at the home's foundation for signs of potential structural concerns. Do you see cracks, bulges or bowing in the foundation that could indicate a severe structural issue? Are there large trees near the house that might be sending roots into the foundation?

- Uneven floors: Uneven or sloping floors can indicate foundation settling or structural problems — issues that can cost $1,500-$6,700 to fix, according to Thumbtack.

- Inefficient windows: Single-pane or drafty windows can significantly increase your heating and cooling bills. Replacement windows are a worthwhile investment, but can cost $850 - $3,400+ per window.

Don't skip the home inspection

A professional home inspector can catch things you might overlook — from structural issues to code violations. Even in a competitive market, skipping the inspection is a risky move that could cost you tens of thousands in unexpected repairs.

4. Long-term features

Zillow research shows that the typical homeowner stays in their home for 14 years before selling. When shopping for a home, think beyond your immediate needs and make sure it can accommodate your long-term goals. Here are the long-term features to think about:

Number of bedrooms and bathrooms

If you plan to grow your family, make sure the new home can accommodate your plans, whether it's an extra room for a new child, an in-law suite for parents, or a guest bedroom for visitors.

If you work remotely, consider whether you need a designated office space or a flexible space where you can work. If you're transitioning to retirement, think about how much space you'll want for your interests or relaxation.

Outdoor space

Do you want a place for parties, kids, and pets? How about a garden? Do you want private space or close proximity to a park or community garden? Make sure the home's yard or outdoor spaces meet those needs — and that you're prepared for the maintenance.

Potential to personalize

Lots of buyers like to add some personal flair. If you want to infuse the home with your own style, you might want to avoid homes that can't be changed enough to fit your preferences, or those with recent upgrades that are selling for top dollar.

For example, a home with a brand-new chef's kitchen featuring marble countertops, and high-end appliances might be priced accordingly — but if your dream is a cozy farmhouse aesthetic with butcher block countertops, you'd essentially be paying a premium for features you'd want to remove.

Lifestyle amenities

You may want your new home to enhance your lifestyle — and are probably envisioning what life in a new home might look like. As you evaluate homes, consider your hobbies and what makes you happy. For example, if you love to cook, pay special attention to the kitchen. If you like to run for exercise, are there trails or pleasant streets nearby?

5. Not the little things

No house is perfect, so try not to get hung up on little imperfections. For example, don't remove a home from your list because you don't like the interior paint color. Cosmetic changes are fairly easy and relatively affordable.

Cosmetic repairs and updates generally include:

- Paint

- Hardware

- Furnishings (the seller's furniture typically leaves with them)

- Landscaping

6. Your must-haves

There's a big difference between your wants and your needs when shopping for a home, so it might help to create a list for each. For instance, a shorter commute might be a must-have, but smart home features are a nice-to-have.

Needs (Non-negotiables):

- Shorter commute

- Specific number of bedrooms and bathrooms

- Designated parking

- Within budget (including repair costs)

Nice-to-haves (Can compromise):

- Kitchen island

- Smart home features

- Finished basement

- Specific architectural style

You may be that lucky buyer who finds a house that checks all the boxes, but chances are you'll have to make some compromises. If you do, make sure you've got your needs covered.

Pro tip: Sometimes compromising might mean doing so with your shopping partner. Read a therapists’ advice on how to handle it.

7. Layout

Think about how the home's layout will support your daily routine:

- Is there a good focus space for anyone working from home?

- Is there a bathroom on each floor for convenience?

- If you plan to age in this home, is there a first-floor bedroom?

8. Storage space

Think about whether the home has enough practical storage:

- Are there enough closets? What about a pantry?

- If there's an attic or basement, is the space usable?

- Is there any outdoor storage for tools, bikes, or seasonal items?

9. Parking

Consider how parking will affect your day-to-day routine:

- Is a garage a must-have?

- How much space will you need for additional vehicles or hosting guests?

- If street parking is the only option, see how many spaces are usually available.

Pro tip: Imagine living in a certain home and hauling in your largest grocery order on a rainy day. Are you OK with that trip?

10. The HOA

The home you’re exploring falls under an HOA — short for homeowners association. If this is the case, look into the HOA’s rules before buying a house so you can decide if the community’s standards and monthly fees fit both your lifestyle and your budget.

If HOA fees cover maintenance and amenities like a shared gym or playground, a townhome can be a worthwhile tradeoff. You might even hang onto it as an investment property if you decide to upsize or downsize.

The bottom line: Focus on what you can't change

When buying a home, focus on the factors you can't change (easily) later: location, structural integrity, and major systems. Everything else — from paint colors to kitchen updates — you can tackle over time.

Make sure your future home:

- Has solid bones (foundation, roof, major systems in good condition)

- Is in a location that works for your lifestyle and commute

- Fits your budget with room for unexpected repairs

- Can accommodate your life over the next 10-15 years

- Passes a professional home inspection

Focus on these critical factors, and you'll make a smarter investment that serves you well for years to come.

Design by Fernanda López, Zillow

How much home can you afford?

At Zillow Home Loans, we can pre-qualify you in as little as 5 minutes, with no impact to your credit score.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Get pre-qualifiedA great agent makes all the difference

A local agent has the inside scoop on your market and can guide you through the buying process from start to finish.

Learn moreRelated Articles

Download the Zillow App

Don’t miss out on the right home for you — browse up-to-date listings, refine your search and more.

Download the free app