How to Compare Mortgage Loan Estimates

Written by Vivian Tejada on June 23, 2026

Edited by Alycia Lucio

A mortgage loan estimate is a standardized document across mortgage lenders that provides important information about the loan, including the total cost of borrowing, principal amount and repayment terms. In the process of obtaining a mortgage for a home purchase or refinance, comparing loan estimates from multiple lenders can help you decide which lender offers the best deal.

Borrowers who seek out multiple quotes from different lenders could save $600-$1,200 a year on mortgage costs, according to Freddie Mac. Yet, the typical home buyer reported in a 2024 Zillow survey that they were pre-approved by only one lender (45%).

Here, we’ll break down how to read and compare mortgage loan estimates, and what to consider before committing to a loan offer.

What is a mortgage loan estimate?

A loan estimate is a three-page document outlining proposed terms and conditions of a mortgage offer, including the interest rate and closing costs. A lender is required by law to provide a loan estimate within three business days of receiving your completed mortgage application.

The loan estimate doesn’t guarantee you’ll be approved for the mortgage. If anything about your credit or financial situation changes that affects the loan estimate — like a change in income, employment or a low home appraisal — you’ll need a new loan estimate. Additionally, loan approval is subject to a variety of other factors, including a clear title report and satisfactory appraisal of the home.

How to read a mortgage loan estimate

The first thing you should read on a mortgage loan estimate is the top left corner of page 1. Here, you’ll see the names of the loan applicants and the home’s address and sale price. Make sure this information is correct before proceeding. Note that the sale price may be tentative pending the appraisal.

From there, here’s how to read a mortgage loan estimate by page:

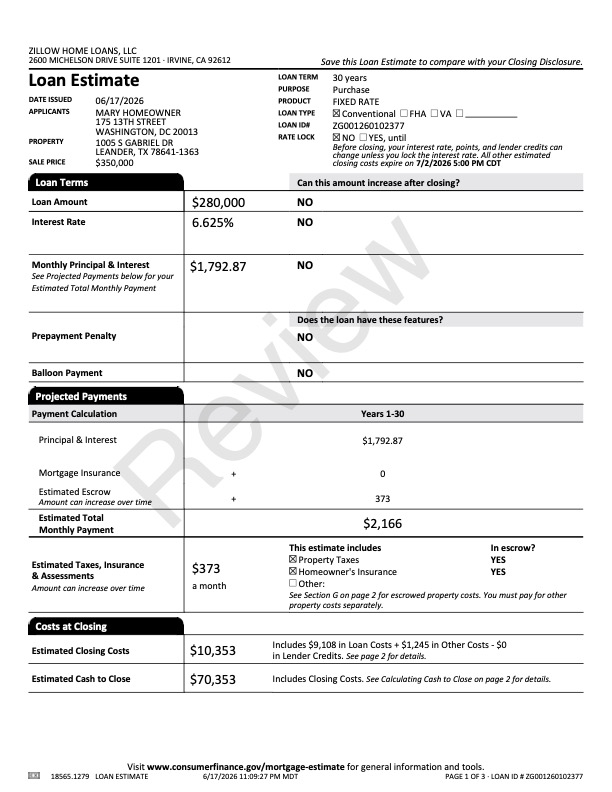

Page 1 of loan estimate

*The above image is a sample for illustrative purposes. It does not reflect your actual costs.

Aside from the identifying information, the first page of a loan estimate outlines the loan terms, interest rate and estimated payments and closing costs.

Section 1: Loan overview

The top right section of page 1 of the loan estimate includes:

- Loan term: Number of years to pay off the mortgage

- Purpose: Purchase (for buying a home) or refinancing (for exchanging your current mortgage for a new one)

- Product: Fixed or adjustable interest rate

- Loan type: Conventional, FHA, VA or other

- Rate lock: Indicates whether your rate is locked and for how long

Section 2: Loan terms

The first middle section of page 1 of the loan estimate includes:

- Loan amount: How much you’re borrowing (loan principal) and whether that can change after closing

- Interest rate: The percentage rate you’ll pay to borrow the mortgage and whether that can change after closing

- Monthly principal and interest: The estimated monthly mortgage payment (not including homeowners insurance and property taxes) and whether that can change after closing

- Prepayment penalty: Whether there’s a fee for prepaying or paying off the mortgage early

- Balloon payment: Whether the loan requires a balloon payment, typically a large lump sum due at a specific time

Section 3: Projected payments

The second middle section of page 1 of the loan estimate includes:

- Payment calculation: Breaks down principal, interest, mortgage insurance and estimated escrow (homeowners insurance premiums and property taxes)

Section 4: Costs at closing

The bottom of page 1 of the loan estimate summarizes the estimated cash you’ll need to pay for closing day.

- Estimated closing costs: How much you can expect to pay for closing (minus any lender credits), covering things like the loan origination fee, escrow payments and prepaid costs

- Estimated cash to close: How much you can expect to pay to finalize the transaction, including closing costs, the earnest money deposit and down payment

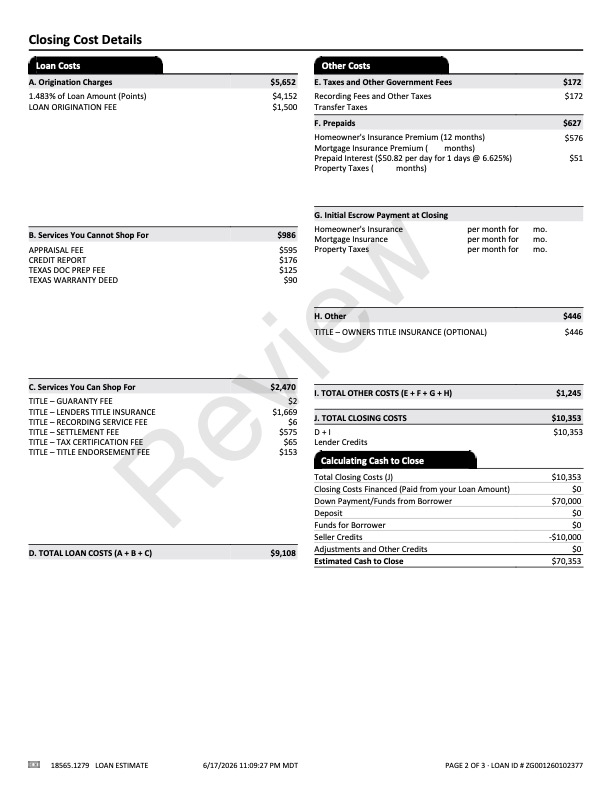

Page 2 of loan estimate

*The above image is a sample for illustrative purposes. It does not reflect your actual costs.

The second page of the loan estimate contains more detailed information about your estimated closing costs and cash to close. This page also clarifies which loan costs you can shop for, such as your title company, and which you cannot.

Section 5: Loan costs

The first section on the left side of page 2 includes a breakdown of the costs to create and fund your loan:

- Origination charges: The fee charged by your lender for creating the mortgage, plus any application, processing or underwriting fees

- Services you cannot shop for: The fees that have a fixed price, such as the appraisal and credit check fees

- Services you can shop for: The fees that you can comparison-shop for, such as title search and insurance fees

Section 6: Other costs

The right side of page 2 of the loan estimate tallies up other costs:

- Taxes and other government fees: Recording fee (to record the deed and loan with the local records office) and transfer taxes, if any

- Prepaids: Any prepaid homeowners insurance premiums, property taxes, per diem interest and other expenses that need to be paid in advance of closing

- Initial escrow payment at closing: How much is needed to fund the escrow account

- Other: Additional or optional costs, such as an owner’s title insurance policy

- Lender credits: Any discounts provided by the lender

Section 7: Calculating cash to close

The final section on the second page of your loan estimate lists every cost needed for closing, totaled up as cash to close. It includes the closing costs, down payment, earnest money, lender credits and seller concessions (if any).

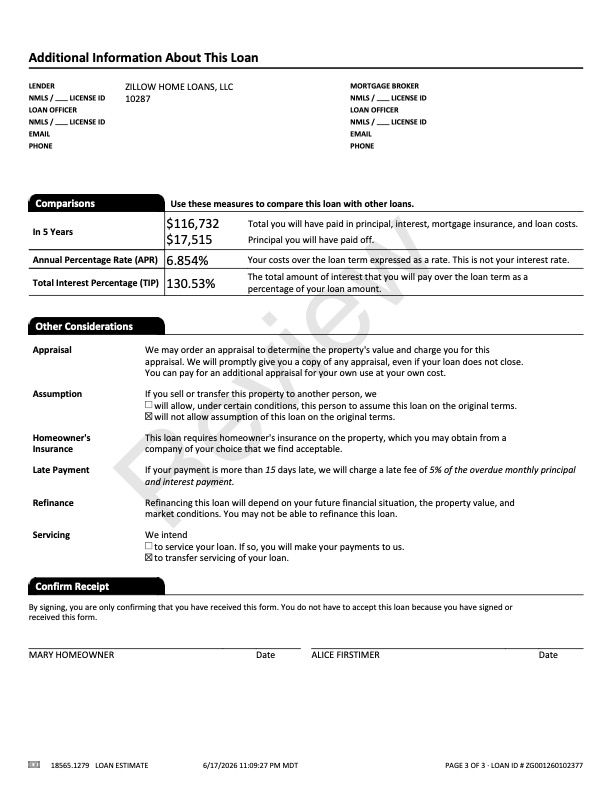

Page 3 of loan estimate

*The above image is a sample for illustrative purposes. It does not reflect your actual costs.

The last page of the loan estimate features other important details about the mortgage, as well as key numbers to compare against other loan estimates.

Section 8: Comparisons

When comparing loan estimates, look at this section to understand the cost of borrowing the mortgage.

- In 5 years: On average, borrowers keep a mortgage for about 5 years before selling their home or refinancing. The first number in this section shows the total dollar amount you’ll pay in the first 5 years of the mortgage (excluding homeowners insurance premiums and property taxes). The second number shows how much of the principal you’ll have repaid after five years. To calculate your 5-year cost of borrowing, subtract the second number from the first number. Use this amount to compare loan estimates.

- Annual percentage rate (APR): The APR is the cost of borrowing over the life of the loan, expressed as a percentage. (This is not the same as your mortgage interest rate). When comparing loan estimates, look for a lower APR.

- Total interest percentage (TIP): TIP represents the amount of interest you’ll pay over the life of the loan, expressed as a percentage of your loan amount. When comparing loan estimates, a lower TIP means you’re spending less on interest.

In addition to finding a lender that saves you money, choose a mortgage lender you can trust. Our loan officers at Zillow Home Loans* have an average 4.9-star rating and offer total transparency to keep you informed every step of the way.

Section 9: Other considerations

Page 3 of the loan estimate explains requirements and other things to expect with your loan, including appraisal and homeowners insurance requirements; whether the mortgage can be transferred to a non-relative third party (a process known as assumption); late payment penalties; and whether the mortgage will be serviced by the lender or a separate entity.

What should you look for on a mortgage loan estimate?

There’s a lot of information to consider in a mortgage loan estimate, but it can help to focus on the areas where lenders differ, such as APR and other loan costs. Here are some questions to consider when comparing loan estimates:

- Interest rate (Page 1): How does this rate compare to average mortgage rates overall?

- Loan amount (Page 1): Can I get the house I want with this amount of money?

- Estimated total monthly payment (Page 1): Am I comfortable with this mortgage payment for the long term?

- Origination charges (Page 2): How much is this lender charging to create the mortgage? Does another lender charge less or fewer fees? Do these estimated costs require paying mortgage points?

- Lender credits (Page 1 or 2): Am I getting lender credits to help offset closing costs?

Final thoughts on comparing mortgage loan estimates

When comparing mortgage loan estimates, zero in on your Total Loan Costs on page 2 of the loan estimate, as well as the loan amount, interest rate and APR to get a sense of how much you’d save with one lender versus another. It may also be a good idea to calculate your 5-year borrowing cost if you plan to sell your home or refinance in the near future.

If you have any questions about your loan estimate, contact the loan officer right away. You can find their information on page 3 of the loan estimate.

How much home can you afford?

At Zillow Home Loans, we can pre-qualify you in as little as 5 minutes, with no impact to your credit score.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Get pre-qualifiedHow much home can you afford?

See what's in reach with low down payment options, no hidden fees and step-by-step guidance from us at

Zillow Home Loans.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Calculate your BuyAbility℠

Related Articles

Get a mortgage with Zillow Home Loans

Go from dreaming to owning with low down payment options, competitive rates and no hidden fees. A dedicated loan officer will guide you until you have your keys in hand.

Zillow Home Loans, NMLS #10287. Equal Housing Lender.