Has Energy Uncertainty Changed our Housing Market Outlook for 2026?

We started 2026 forecasting very modest growth in housing — specifically, an increase in existing home sales of 4.3%. While that of course would not be a strong market, it would represent a market that had turned a corner, with 2026 acting as a ‘reset’ year. However, new uncertainty has emerged via energy prices and inflation concerns, adding fresh complexity to our outlook.

The housing market has been bouncing along the bottom for three years, and we entered 2026 with data-driven optimism that the market would start to improve, with a modest increase in existing home sales and the year ending with a typical home affordable to the median household in 20 of the 50 major metro areas.

More uncertainty has entered that outlook, with elevated mortgage rates likely to act as a slight drag on the spring season, already removing about a third of the year-over-year affordability gains we’ve seen. However, markets can move quickly and it’s possible for the outlook to improve or worsen. Given this new uncertainty it is useful to shift one’s view of the potential 2026 outcomes from a singular forecast to a set of possible scenarios, each with their own path-dependent possibilities.

To model a few different scenarios, we examined two key mechanisms:

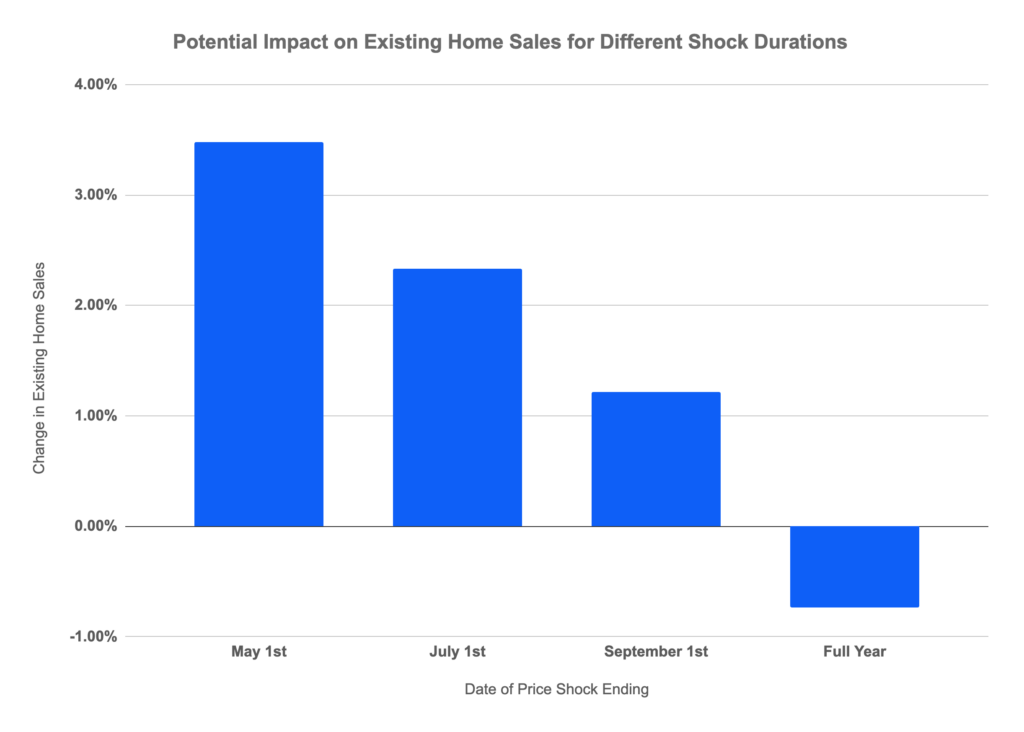

One must be careful at over interpreting the full-year effect of something that does not persist for a full year. The challenge here, of course, remains that no one knows precisely when elevated energy prices will subside; the futures market for oil can offer some clues about investor expectations, but nothing is certain.

We have modeled the outcome if the current 50 basis-point (bps) increase in mortgage rates persists for the full year alongside a slight 20 bps increase in the unemployment rate.

If that dual shock of higher rates and unemployment persists through the end of April, we forecast 2026 existing home sales would still rise 3.48% over the previous year. If the shock ran through June and ended on July 1, existing sales would rise 2.33% on the year. If the shock persisted through the peak home shopping season, ending September 1, then sales would only rise by 1.21%. If mortgage rates remained elevated by 50 bps from their counterfactual path and unemployment also rose by 20 bps for the rest of 2026, then we expect existing home sales would decline slightly by -0.73%.

| Shock Ends May 1st | Shock Ends July 1st | Shock Ends Sept 1st | Shock Lasts Full Year |

| 3.48% | 2.33% | 1.21% | -0.73% |

Methodology note

We modeled this as a linear binary shock to the housing market, rather than modeling additional parameters for rapid recovery and catch up sales (which would make the model more optimistic) or for downstream impacts on sentiment and intent (which would make the model more pessimistic) . Given the uncertainty involved, we opted to err on the side of simplicity.

{kind=link}