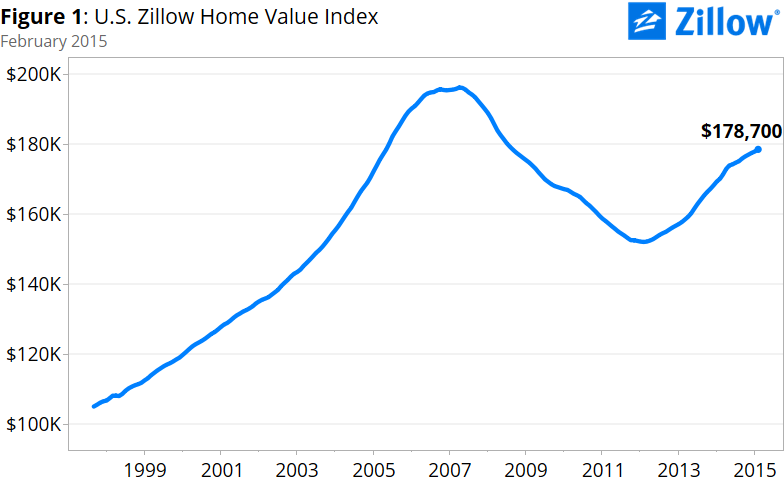

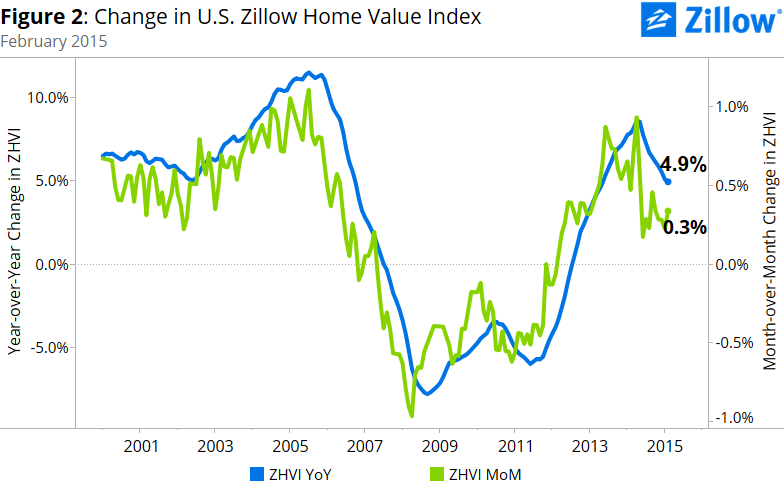

- In February, the U.S. median home value was $178,700, up 4.9 percent from February 2014.

- February represents the first month since May 2013 in which the pace of annual home value appreciation in a given month was less than 5 percent.

Historically, home values have grown at a relatively modest 3 percent per year, on average, give or take a few percentage points. Annual growth rates above 5 percent are generally the exception, not the rule – and often indicate something is out of whack. And for the past couple of years, something has definitely been out of whack in the housing market.

U.S. home values had been growing at more than 5 percent per year for 20 consecutive months. Until now. And that’s a good thing.

In February, the U.S. median home value was $178,700, up 4.9 percent from February 2014. February represents the first month since May 2013 in which the pace of annual home value appreciation in a given month was less than 5 percent.

On the surface, it may be tempting to wonder if this slowdown in appreciation is a bad sign, signaling that the robust recovery in home values we’ve been enjoying thus far is near an end. The truth is, this slowdown is in fact the next stage in the recovery, leaving behind the days of rapid double-digit home value appreciation that many markets across the U.S. saw, and there are few bad things about it.

It’s both abnormal and unsustainable to see rapid home value growth of the kind we’ve seen the past few years – peaking at 8.6 percent nationwide in April 2014, and exceeding 20 percent or even 30 percent annual growth in some local markets.

Rapid growth has been driven largely by high demand and low supply, external factors not typically associated with more balanced, healthy, “normal” markets. Demand came first from bargain hunters and investors eager to scoop up inexpensive properties in the wake of the recession, and is now being supplemented by first-time buyers and millennials as they enter the market in their prime home buying years. At the same time, the supply of homes for sale has remained depressed, both because builders have been struggling to get back up to speed post-recession, and because millions of homeowners are unable to sell because they are trapped in negative equity.

As a result, competition for those homes that are available has been fierce, and home values have gone up. This rapid appreciation has kept many potential buyers on the sidelines in rentals. This together with limited multifamily construction has been constraining rental supply and causing rental appreciation to skyrocket, contributing to a growing rental affordability crisis. What is normally a balanced market has been thrown off balance.

But the market is changing. As more inventory (slowly) comes on line and competition cools, particularly as investors exit the market, growth is being driven less by the kinds of external factors noted above and more by traditional fundamentals like job growth, wage gains and household formation. And a market driven by these fundamentals simply can’t sustain rapid appreciation north of 5 percent or more for very long, since typically growth in jobs, income and households just does not and cannot keep pace.

If we want a market driven by fundamentals and not by imbalances, which we do, then we should expect and welcome this slowdown. It allows everyone to catch their breath. It also injects, perhaps counter-intuitively, more confidence into the market. Our research shows that today’s renters – tomorrow’s buyers – tend to be more confident in their local housing market in areas where home values are growing more slowly. This confidence among renters, in turn, will likely push more of them into homeownership. Roughly 5 million current renters say they want to buy in the next year, up from 4 million at the same time last year. As more renters turn into homeowners, demand in the rental market will ease, helping to cool rapid appreciation and creating more vacancies that can be soaked up as more young households form.

The market is moving out of the bounce-off-the-bottom phase of the recovery and beginning to act more normally. It isn’t happening overnight, and it won’t always be easy for everyone, but overall this is great news.

Slow-and-steady, in housing as in life, really does win the race.

Home values remain steady

The median home value in the U.S. was $178,700 in February, up 0.3 percent from January. On an annual basis, home values were up 4.9 percent from February 2014. February 2015 marked the first month in which annual home values rose at an annual pace below 5 percent since May 2013. The annual appreciation rate in home values has fallen for the past 10 months. U.S. median home values stand roughly where they were in May 2005. Home values remain 9 percent below their April 2007 peak of $196,400.

The February Zillow Real Estate Market Report covers 478 metropolitan and micropolitan areas. In February, home values rose month-over-month in 336 of 478 metros (70.3 percent). In 196 metros, the annual appreciation rate exceeded that of the U.S. as a whole.

Among the nation’s largest 30 metro areas, 16 experienced annual appreciation rates of 5 percent or higher. Denver, Miami, San Jose, Las Vegas and Atlanta all saw double digit year-over-year appreciation in home values. None of the largest markets experienced annual declines in home values, but three (Detroit, Chicago and Cleveland) all experienced monthly declines. In Philadelphia, home values were flat from January to February.

Rents are on the Rise

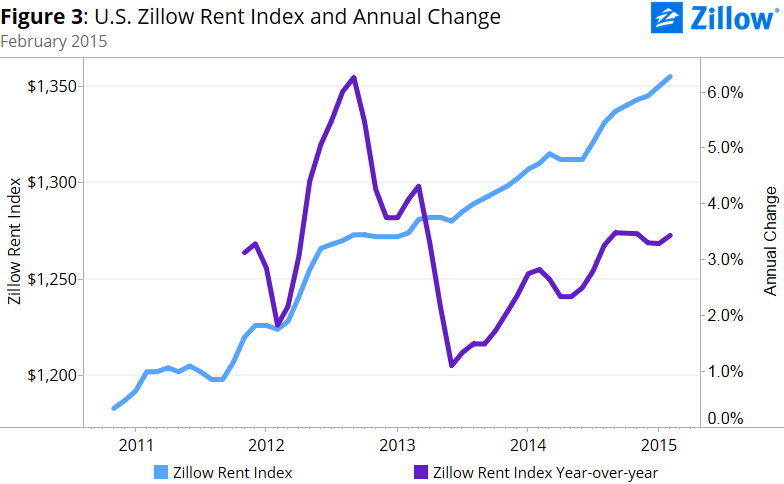

Of the 859 metropolitan and micropolitan areas covered by the Zillow Rent Index (ZRI), 597 (69 percent) experienced year-over-year rent increases in February. U.S. median rents rose 3.4 percent year-over-year in February, to a Zillow Rent Index of $1,355. Annual rental appreciation peaked in September 2012 at 6.3 percent.

Of the 859 metropolitan and micropolitan areas covered by the Zillow Rent Index (ZRI), 597 (69 percent) experienced year-over-year rent increases in February. U.S. median rents rose 3.4 percent year-over-year in February, to a Zillow Rent Index of $1,355. Annual rental appreciation peaked in September 2012 at 6.3 percent.

Among the 30 largest metro areas, annual rental appreciation in 21 exceeded the 3.4 percent national pace. The San Francisco metro experienced the highest annual rent appreciation among large markets, up almost 15 percent since February 2014. Coincidentally (or not), San Francisco also had the smallest increase in building permits over the same period, when normalized to population growth.

Inventory

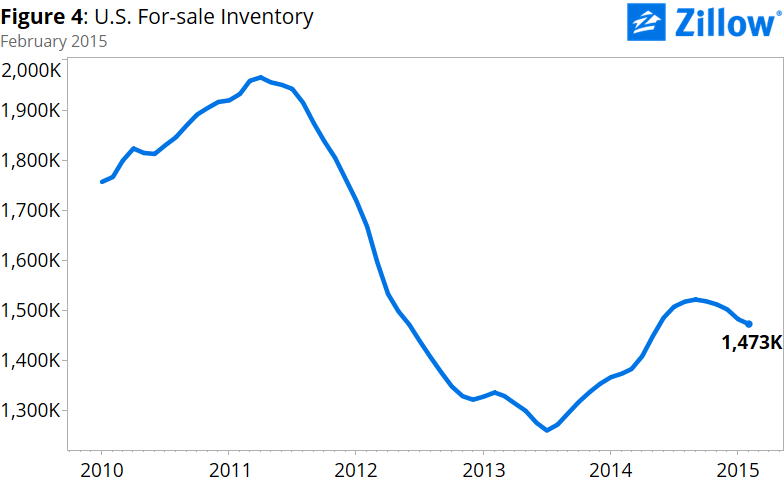

The number of homes listed for sale on Zillow was up 7.2 percent year-over-year in February, but has declined month-to-month for the past five months (seasonally adjusted). Among the largest 30 metro areas, 18 experienced monthly declines in the number of homes for sale; 11 of those 18 experienced year-over-year increases in for-sale inventory. Metro areas that experienced the largest increases in for-sale inventory year-over-year are Las Vegas, Washington, D.C., Orlando and Baltimore.

The number of homes listed for sale on Zillow was up 7.2 percent year-over-year in February, but has declined month-to-month for the past five months (seasonally adjusted). Among the largest 30 metro areas, 18 experienced monthly declines in the number of homes for sale; 11 of those 18 experienced year-over-year increases in for-sale inventory. Metro areas that experienced the largest increases in for-sale inventory year-over-year are Las Vegas, Washington, D.C., Orlando and Baltimore.

What Comes Next?

The Zillow Home Value Forecast predicts further 2.6 percent appreciation through February 2016, a rate even slower than today’s and a further sign that the market is normalizing and re-gaining some of the balance lost during the recession and subsequent recovery. But that normalization won’t happen overnight, nor will it be uniform. Another sign of a truly normal housing market is the absence of a uniform national market in which all local markets act the same. Real estate is local, and local dynamics have been and will continue to reassert themselves going forward. West Coast markets like the Bay Area and Seattle will likely continue to sizzle, driven by rapid growth in tech jobs and an influx of new residents. We’re beginning to see signs of a marked slowdown in Texas rental markets as energy-sector layoffs and low oil prices impact local economies. Home value appreciation in the densely populated Northeast Corridor will continue to plod along steadily, with the Boston, New York, Philadelphia, Baltimore and Washington, D.C., metros all expected to grow by less than 3 percent over the next year. The recovery is not over, it is merely entering a new phase that will bring us closer to normal every month.

Slowly, and steadily.