- After 30 years, a borrower putting down 3.5 percent could save more than $14,700.

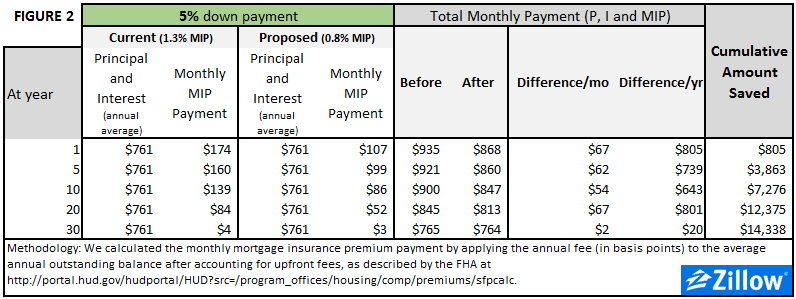

- After 30 years, a borrower putting down 5 percent would save more than $14,300.

An almost 40 percent cut to a key federally backed annual mortgage insurance premium, the heart of a renewed effort by President Barack Obama to make homeownership more affordable and accessible, could save typical homeowners and buyers thousands of dollars, according to a Zillow analysis.

In a speech in Phoenix Thursday, President Obama announced that the Federal Housing Administration (FHA) will reduce annual mortgage insurance premiums (MIP) by half a percentage point. Premiums for those borrowers putting between 3.5 percent and 5 percent down on their home will be lowered to 0.85 percent, from 1.35 percent. For borrowers with a 5 percent down payment or greater, the premiums will fall to 0.8 percent, from 1.30 percent.

FHA mortgage premiums are paid annually in 12 monthly installments, on top of principal, interest and insurance. For new FHA loans, the premiums must be paid over the entire life of the loan, unlike pre-2013 loans where mortgage insurance was waived after homeowners achieved 20 percent equity in their home.

Thousands in Potential Savings

Assuming a borrower is taking out a loan on a typical $175,000 home (roughly the national U.S. median home value, as of November), the savings for FHA-insured borrowers could be substantial. After 30 years, a borrower putting down 3.5 percent could save more than $14,700 over the life of a 30-year loan (figure 1). A borrower putting down 5 percent would save more than $14,300 (figure 2).

According to a statement released by the Obama Administration, the lowered premiums are expected to help more than 800,000 existing homeowners (through refinancing) and lure up to 250,000 new buyers into the market in the first year.

If the expectations come true (a big if), those numbers would represent a big boost to sales volumes that remain below historic norms, even as the housing market overall has recovered well since bottoming in late 2011 and early 2012. In November, sales of existing homes slowed substantially from October, to a seasonally adjusted annual rate (SAAR) of 4.93 million units, short of historic norms of more than 5 million (SAAR). New home sales in November were down 1.6 percent from October, to approximately 438,000 units (SAAR), also well below historically normal levels between 800,000 and 1 million units (SAAR).

The plan to lower FHA premiums is not without its critics. The FHA is required by law to keep a reserve fund with a capital ratio of 2 percent in order to cover any potential future losses from insured loans gone sour. During the housing crisis, this reserve fund was severely depleted, and FHA premiums were initially raised to help replenish the fund. The ratio currently stands at 0.41 percent, as of Sept. 30, still well below statutory levels.

The White House said it is betting that added volume from more borrowers attracted by lower premiums will offset the cuts, noting that premiums of 0.85 percent and 0.8 percent are still well above historic levels around 0.55 percent.

“This robust premium structure will more than cover the related estimated credit losses posed to the insurance fund from newly originated loans, continuing to strengthen the fund and protect taxpayers,” the White House said in a statement.

The call to reduce FHA insurance premiums was the most specific among a set of broader goals announced by President Obama intended to strengthen the broader housing market and keep housing near the top of the national agenda in advance of his Jan. 20 State of the Union address.

Secondary Goals

Among the secondary goals announced, among the most interesting was the Administration’s promise to strengthen access to affordable rental housing. Thanks to mortgage rates near record lows and home values that remain below their pre-recession peaks in most areas, buying a home is more affordable today than it was in the pre-bubble years from 1985. A typical buyer today should expect to pay about 15 percent of their incomes on the mortgage for the typical home (principal and interest only), compared to 22 percent historically.

But renters don’t have the advantage of low interest rates and below-peak prices. Since 2000, rents have grown by more than 50 percent, while wages have grown at only half that pace. As a result, renters today should expect to pay almost 30 percent of their incomes to afford their monthly rent, up from about 25 percent historically.

Because today’s renters are tomorrow’s buyers, the issue of rental affordability has broad impacts on the housing market overall. With an ever-increasing portion of income devoted to rent, it can be difficult for potential buyers to save up even a modest down payment, particularly for would-be buyers on an entry-level salary. Without specifying details, in a statement the White House promised to “continue its push for expanding support for affordable rental housing, and reducing barriers to housing development that increase housing costs.”

Another goal laid out by the White House was a continuation of efforts to cut red tape and clarify regulations. Many qualified buyers are being denied loans, the White House said, when their credit profiles suggest they shouldn’t. Anecdotally, a big reason for this is uncertainty surrounding when and how a lender might be forced to buy back a loan previously sold to a government sponsored entity like Fannie Mae or Freddie mac in the event it goes sour.

“HUD and independent agencies like the Federal Housing Finance Agency are working with stakeholders to clarify put-back and indemnification policies and enhance lender understanding of these policies to encourage originators to extend lending to all creditworthy families,” the White House said in a statement.

The President also re-iterated his calls for a Congressional plan to overhaul the nation’s mortgage finance system. Fannie Mae and Freddie Mac, the two government-sponsored mortgage giants that have been under federal conservatorship since 2008, are currently operating in a kind of limbo, even as they continue to insure the vast bulk of U.S. mortgage loans. A number of plans have been put forward to help change the system, but none have so far gained the bipartisan support necessary to advance through Congress.