Q2: Hot Markets See Runaway Rents Amid Dropping For-Sale Inventory

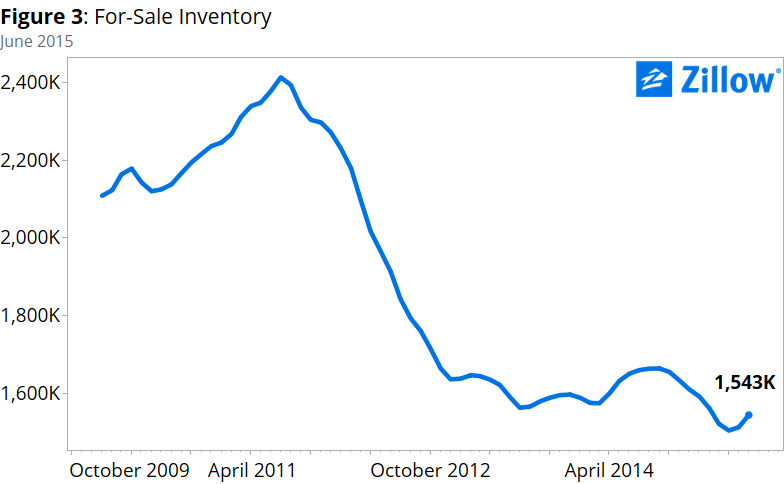

Increasing rents and declining affordability for rentals, along with low mortgage rates, are making homeownership attractive to prospective buyers. The only problem? There aren’t enough homes out there for all of them to buy. Nationally, inventory is down 6.5 percent from last year—but is down 36 percent from its peak of 2.4 million homes in July 2011. The country has had low numbers of homes for sale for almost three years.

Denver is one of the nation’s hottest markets for both real estate and rentals. Yet this city has a double-digit decline in for-sale inventory from last year, and inventory there is more than 70 percent below its post-bubble peak. This is an especially difficult problem for Denver as the metro has seen a rapidly increasing population. The markets with the largest gains in home values during Q2—San Francisco, San Jose, Dallas and Denver—are also among the markets with the biggest declines in for-sale inventory from peak levels.

Low interest rates, strong growth in rent prices, persistent negative equity and a lack of for-sale inventory continue to distort local real estate markets. But each market marching to the beat of its own drummer means each market is responding to fundamentals, in contrast to the last decade’s widespread bubble and bust.

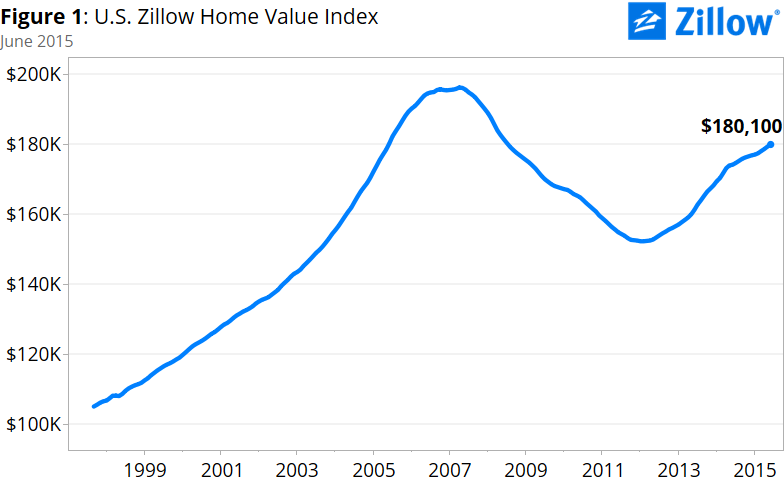

The 2015 Q2 Zillow Real Estate Market Report covers 515 metropolitan and micropolitan areas. In Q2, the median U.S. home value was $180,100, rising 1.1 percent from 2015 Q1 and 3.3 percent from 2014 Q2. Nationally, home values remain 8.3 percent below the peak in 2007 Q2 ($196,400 in April 2007).

The 2015 Q2 Zillow Real Estate Market Report covers 515 metropolitan and micropolitan areas. In Q2, the median U.S. home value was $180,100, rising 1.1 percent from 2015 Q1 and 3.3 percent from 2014 Q2. Nationally, home values remain 8.3 percent below the peak in 2007 Q2 ($196,400 in April 2007).

In Q2, four markets had double digit appreciation on an annual basis out of the top 35 metro areas. Denver continues to be red hot, with home values up 15.4 percent from last year. Also hot are Dallas (12.5 percent annual appreciation), San Jose (12.4 percent annual appreciation) and San Francisco (11 percent annual appreciation). Only Baltimore saw home values decline, albeit slightly, over the past year (-0.6 percent change in home values).

On a quarterly basis, Portland joined the red hot markets with more than 3 percent home value appreciation. Both Denver and San Jose had home values grow more than 4 percent in the last quarter, while Dallas, Portland and San Francisco saw quarterly growth of more than 3 percent. From Q1 to Q2, Philadelphia, Washington, New York and Baltimore saw small declines in home values.

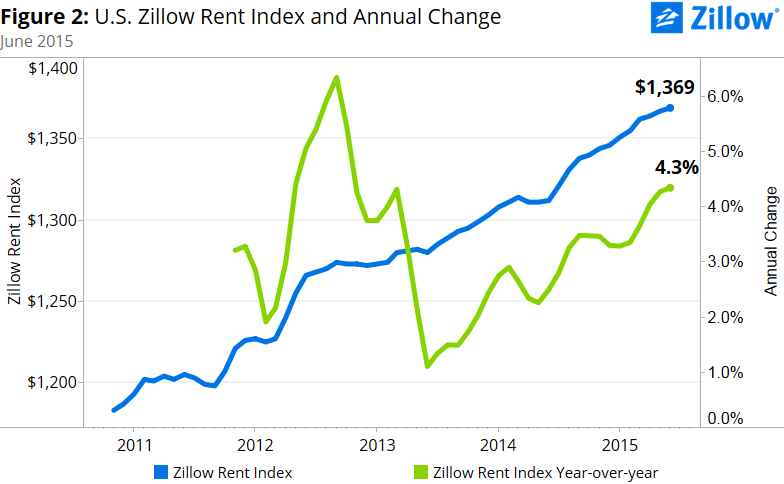

Nationwide, rental growth surged past a 4 percent annual pace in June, up 4.3 percent to a median U.S. rent of $1,369 per month. In Q2, rent growth outpaced home values growth in just under half of the nation’s 35 largest metro areas.

Nationwide, rental growth surged past a 4 percent annual pace in June, up 4.3 percent to a median U.S. rent of $1,369 per month. In Q2, rent growth outpaced home values growth in just under half of the nation’s 35 largest metro areas.

The top movers and shakers for rentals were markets also red hot on the for-sale side, seeing strong home value appreciation. San Francisco led annual increases in rents for Q2, at 14.5 percent. Denver wasn’t far behind, with rent up 13 percent year-over-year. Rent in San Jose grew 12.5 percent in the past year while Portland rents were up 10.8 percent. From Q1 to Q2, rents in Denver and both large Bay Area metros grew 3 percent or more. Metros that are seeing strong appreciation in rents, as well as home values, are experiencing healthy increases in demand with often thriving job markets and sometimes tight inventory supply.

Of the 863 metropolitan and micropolitan areas covered by the ZRI, 645 saw annual growth in rents in Q2. 527 metro areas saw rents increase from Q1 to Q2.

As rents have steadily increased to dizzying new heights, renters have aspired to become homeowners – in fact 5.2 million of them would like to make the switch. However, they face considerable hurdles along the way. If they manage to save up enough for a down payment and qualify for a mortgage, they are now faced with the added complication of actually finding a house they like. Nationally, the inventory of for-sale homes declined 6.5 percent from the second quarter of 2014 (seasonally adjusted). Of the nation’s largest 35 metros, 19 saw annual declines in inventory. Of the 668 metro areas covered by Zillow, 421 saw declines in for-sale inventory on an annual basis.

As rents have steadily increased to dizzying new heights, renters have aspired to become homeowners – in fact 5.2 million of them would like to make the switch. However, they face considerable hurdles along the way. If they manage to save up enough for a down payment and qualify for a mortgage, they are now faced with the added complication of actually finding a house they like. Nationally, the inventory of for-sale homes declined 6.5 percent from the second quarter of 2014 (seasonally adjusted). Of the nation’s largest 35 metros, 19 saw annual declines in inventory. Of the 668 metro areas covered by Zillow, 421 saw declines in for-sale inventory on an annual basis.

Over the next year, home value growth is expected to slow even further, to 2.4 percent through 2016 Q2, according to the Zillow Home Value Forecast. Over the past year, home values grew 3.3 percent. Continued steady growth in the real estate market shows signs that the market is maintaining stability after going through the housing bubble and bust of 2007 through 2012. The recovery in local markets has been uneven, with home values exceeding some markets, such as Denver and the Bay Area, having home values that have exceeded their bubble-era peaks.

Harder-hit markets like Las Vegas and Orlando are still 30 percent or more below their respective 2006 peaks in home values. Zillow expects continued growth in those markets and continued affordability for homebuyers, even with moderate increases in interest rates (5 or 6 percent mortgage rates).

In the future, with strong economic fundamentals like job growth, increasing household formation and stronger income growth, the housing market should be able to overcome the headwind of rising mortgage rates.

{kind=link}