Are Local Real Estate Bubble Markets Re-Emerging? Experts Agree to Disagree

The national housing market on the whole is expected to cool off in coming years, even as conditions in a handful of hot markets have some experts worried about local real estate bubbles. And there is no clear consensus on the extent of the national cool-down, or the potential timeline for local bubble risks.

•

Dec 09 2015

•

Dec 09 2015

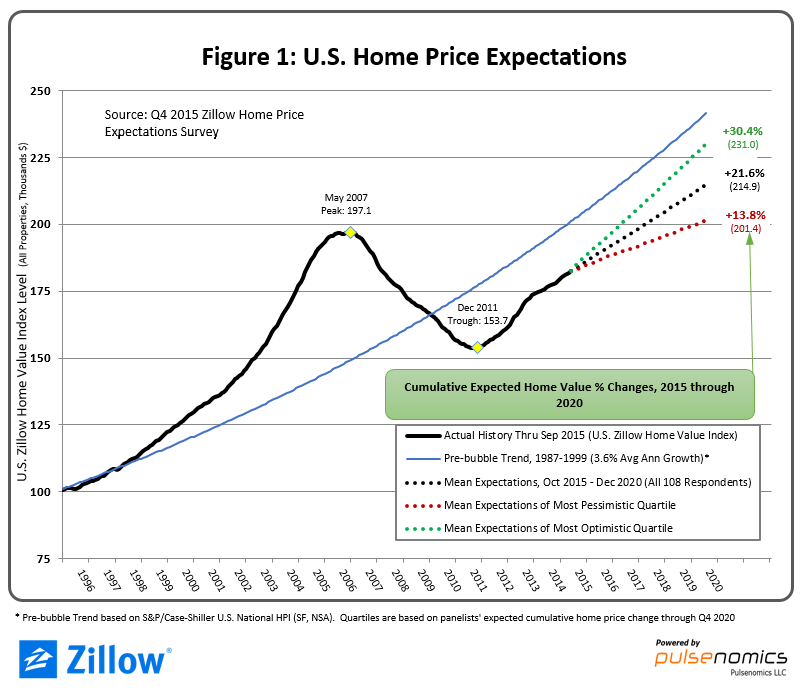

- U.S. median home values are expected to end 2015 up 3.9 percent year-over-year, on average, with annual growth falling to 3.4 percent next year and to rates just above 3 percent in each year through 2020, according to the Q4 Zillow Home Price Expectations Survey.

- The most optimistic quartile of panelists said they expected U.S. home values to rise 4.7 percent next year, while the most pessimistic quartile predicted growth of 2.3 percent in 2016.

- Most respondents agreed that the five-county San Francisco metro either was in a bubble, or was at significant risk in coming years.

The national housing market on the whole is expected to cool off in coming years, even as conditions in a handful of hot markets have some experts worried about local real estate bubbles. And there is no clear consensus on the extent of the national cool-down, or the potential timeline for local bubble risks.

Confusing? Yes. Alarming? Not particularly.

The fourth quarter Zillow Home Price Expectations survey, sponsored by Zillow and conducted quarterly by Pulsenomics LLC, asked more than 100 economists and real estate experts about their expectations for the national housing market and 20 large local markets nationwide in coming years.

Even as the majority of panelists agreed that U.S. home value growth overall should continue to slow in coming years, there’s a clear divide between the most optimistic and pessimistic experts. Additionally, the responses revealed that some experts are concerned about potential real estate bubbles in some of the nation’s hottest markets. But there is significant disagreement over the extent to which rapid home-value growth in those markets puts consumers at risk, and when.

The 108 survey respondents said they expect U.S. median home values to end 2015 up 3.9 percent year-over-year, on average, with annual growth falling to 3.4 percent next year and to rates just above 3 percent in each year through 2020. This scenario would result in a national median home value of more than $215,000 by the end of this decade. The average expected growth is down from projections of 4.1 percent growth through the end of the year and 3.4 percent average annual expected appreciation in coming years recorded in last quarter’s survey, and represents a three-year low for the panel.

Average annual home value growth in the 3 percent range is in line with historic, pre-bubble (1987-1999) U.S. norms of 3.6 percent. But there is little agreement among the experts on the actual path of home value growth. The most optimistic quartile of panelists said they expected U.S. home values to rise 4.7 percent next year, and to surpass their May 2007 peak levels in April 2017. But the most pessimistic quartile said they expect only 2.3 percent appreciation in 2016, and even more subdued appreciation in following years, potentially keeping the market from surpassing pre-bust peaks until September 2019 (figure 1).

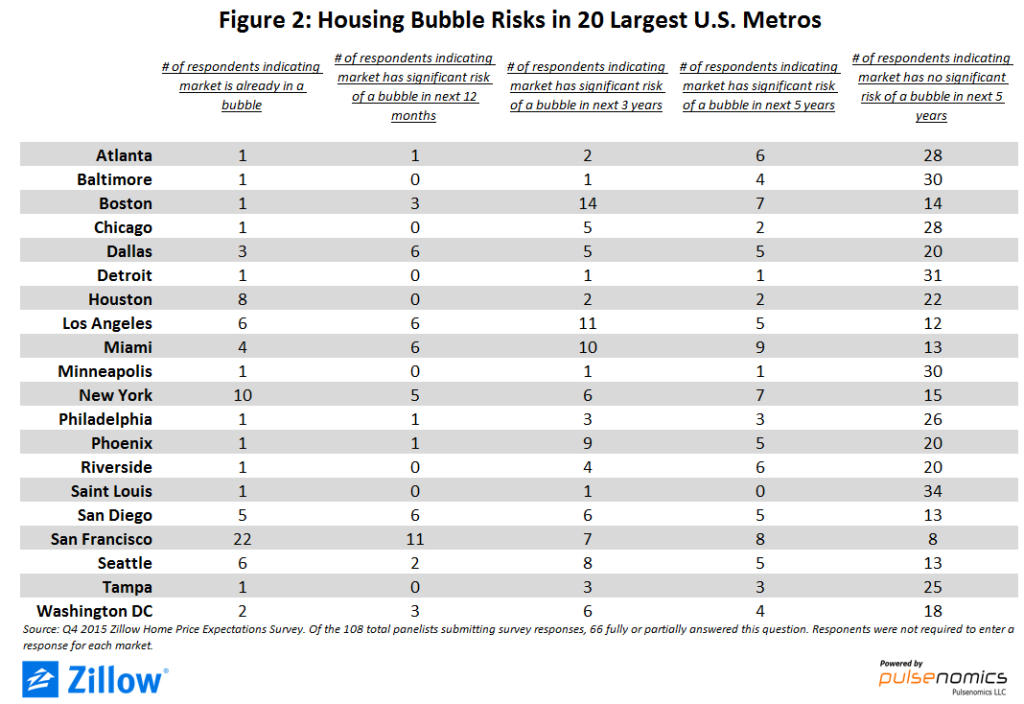

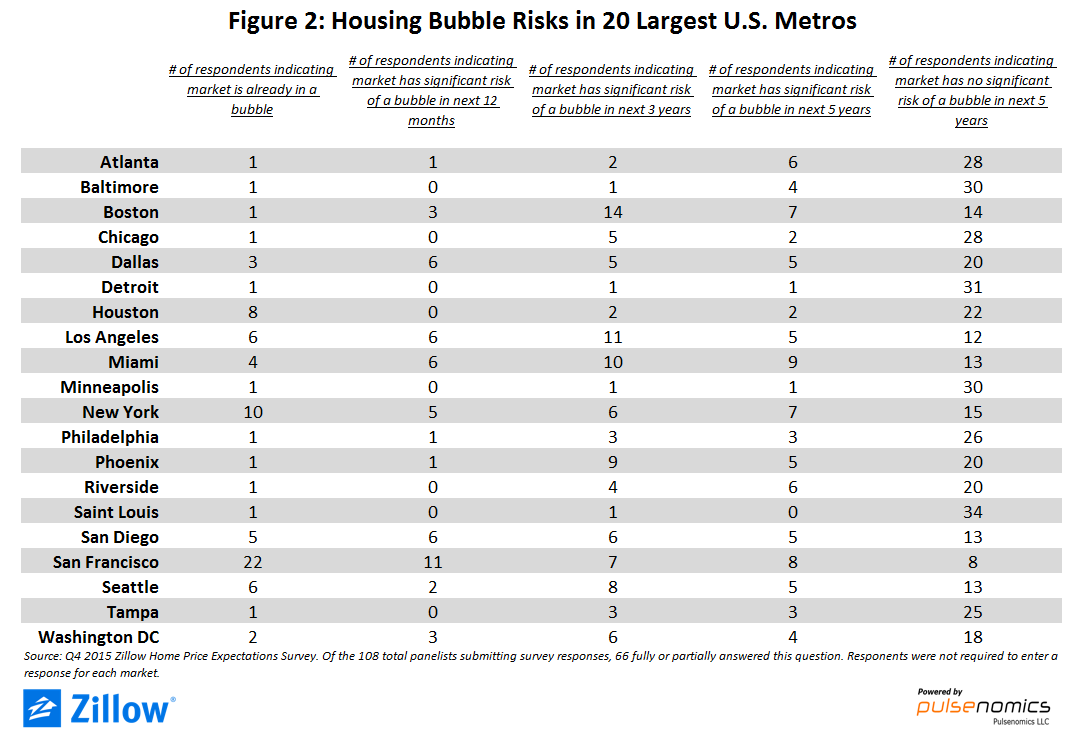

And according to the experts, the local picture is not any clearer than the national picture. Panelists were asked to assess local housing conditions in the 20 largest U.S. metro markets and offer their opinions on if those markets were currently, or were at significant risk of entering a real estate bubble in one, three or five years.

And according to the experts, the local picture is not any clearer than the national picture. Panelists were asked to assess local housing conditions in the 20 largest U.S. metro markets and offer their opinions on if those markets were currently, or were at significant risk of entering a real estate bubble in one, three or five years.

Most respondents agreed that the five-county San Francisco metro either was already in a bubble, or was at significant risk in coming years (figure 2). And that’s largely where agreement stopped. Several respondents indicated that the New York, Miami and Los Angeles markets also presented some bubble risk, though more indicated no risk in these markets in the next five years. And just as many respondents (14) said Boston was at risk of entering a bubble in the next 3 years as indicated Boston had no significant risk in the next five years.

So, what to make of these contradictory results? The overall takeaway is that identifying a bubble is difficult, even for professional economists. The impact of these potential local bubbles is also difficult to determine, but it’s possible that local home values in particularly hot areas may begin to fall somewhat as more residents are priced out amidst rising affordability concerns, especially when interest rates rise.

So, what to make of these contradictory results? The overall takeaway is that identifying a bubble is difficult, even for professional economists. The impact of these potential local bubbles is also difficult to determine, but it’s possible that local home values in particularly hot areas may begin to fall somewhat as more residents are priced out amidst rising affordability concerns, especially when interest rates rise.

The typical homebuyer in the Bay Area, for example, can currently expect to pay 41 percent of their income on a mortgage payment for the area’s median home, up from 37 percent historically. And that’s with mortgage interest rates currently hovering near historic lows. If and when mortgage interest rates hit 5 percent, San Francisco home buyers could expect to pay almost half (48 percent) of their income to a mortgage. It’s possible, even likely, that many potential home buyers may balk at this, causing home values themselves to fall.

But while there is some risk of a highly localized dip in some markets, there is virtually no risk of the larger U.S. housing market collapsing in coming years like it did last decade. The mid-2000s housing boom and bust was driven largely by speculation and a glut of borrowers taking on loans at terms that virtually guaranteed they would not be able to re-pay them down the road. Today, lending restrictions are much tighter and lenders are more cautious, and home value growth itself in most local markets is driven by traditional fundamentals like household formation and local job and income growth.

Still, it’s important that some experts are discussing bubble risks at all. It shows that even eight years after the bust, the larger U.S. housing market has yet to fully heal, even as significant risks have re-emerged within certain large housing markets.

The wide variety of opinions also serves to reinforce the broader trend the market has been experiencing over the past few years, and is expected to continue experiencing as the recovery marches on. Unlike during the real estate crash that began in 2007, and the recovery which started in 2012, local markets largely aren’t moving in unison – first down during the crash, then up during the recovery. Local markets are reacting to local conditions, with some growing rapidly as their jobs markets grow, and others still trying to build themselves back up to pre-recession levels. The national housing market is, by definition, a collection of local markets behaving independently.

{kind=link}