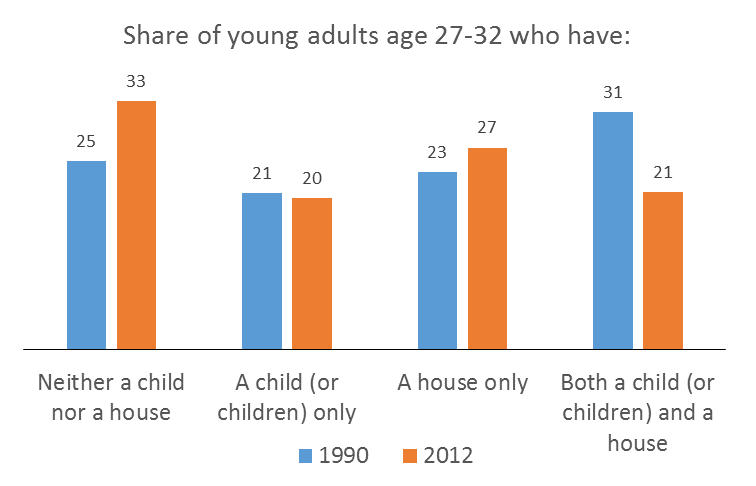

On Tuesday morning the Federal Reserve Bank of New York published the results of their 2013 Consumer Credit Panel, which shows that over the course of the recession, homeownership has dropped among young adults irrespective of student loan debt. There is widespread agreement that due in part to the recession, young adults have delayed many of the traditional hallmarks of adulthood—such a buying a home or starting a family. To look into this question a little deeper, Zillow Research used Census Bureau data to compare the share of young adults age 27-32 in 1990 and 2012 who owned a home, had at least one child or both.

The results are displayed in the graph below. In 2012, about two-thirds of young adults had achieved one or both of these hallmarks, compared with three-quarters a generation ago. Unsurprisingly, the share with both a house and children has plummeted from 31 percent in 1990 to 21 percent in 2012. What is striking, however, is that when it comes to choosing either a house or children, more young adults seem to be opting to become homeowners: The share with children but no house fell slightly from 21 percent to 20 percent, while the share with a house but no children actually increased from 23 percent to 27 percent.

Sources:

Brown, Meta, Sydnee Caldwell, and Sarah Sutherland. “Young Student Loan Borrowers Remained on the Sidelines of the Housing Market in 2013.” Federal Reserve Bank of New York, Liberty Street Economics. May 13, 2014.

1990 Decennial Census (5 percent Sample) and 2012 American Community Survey. Steven Ruggles, J. Trent Alexander, Katie Genadek, Ronald Goeken, Matthew B. Schroeder, and Matthew Sobek. Integrated Public Use Microdata Series: Version 5.0 [Machine-readable database]. Minneapolis: University of Minnesota, 2010.