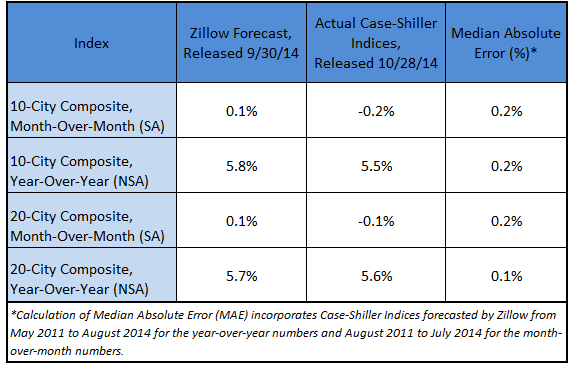

Today, the S&P/Case-Shiller Home Price Indices showed that the non-seasonally adjusted (NSA) August 10- and 20-City Composites rose 5.5 and 5.6 percent, respectively on a year-over-year basis, in line with Zillow’s forecast released last month. On a seasonally adjusted (SA) monthly basis, the 10- and 20-City Composites fell 0.2 and 0.1 percent, respectively, from July to August. The table below shows how Zillow’s forecast compared with the actual numbers.

“After several months in a row of slowing home value growth, it’s fair to say now the market has officially turned a corner and entered a new phase of the recovery. We’re transitioning away from a period of hot and bothered market activity, characterized by low inventory and rapid price growth, onto a more slow and steady trajectory, which is great news,” said Zillow Chief Economist Dr. Stan Humphries. “In housing, boring is better. As appreciation cools and more inventory comes on line, buyers will start to gain a more competitive advantage, after years of sellers being in the driver’s seat. More sedate home value growth, coupled with interest rates that remain incredibly low, will also help housing stay affordable, which is critical to drawing in the next generation of younger, first-time buyers that had been sitting on the sidelines.”

Our forecasting model incorporates previous data points of the Case-Shiller series, as well as Zillow Home Value Index data and national foreclosure resales. To see how Zillow’s forecast of the July Case-Shiller indices compared, see our research brief from last month.