- Experts predict home values will grow 19 percent cumulatively through 2019, with the median U.S. home value set to exceed $200,000 in April 2018.

- U.S. median home values are expected to surpass their bubble-era peak of $196,400 in October 2017.

- 64 percent of respondents said they expect mortgage credit access to ease over the next year.

When it’s all said and done, it will have taken more than a decade for U.S. home values to gain back all the losses incurred during the housing bust, according to a recent survey of more than 100 economists and real estate experts.

The 2015 Q2 Zillow Home Price Expectations Survey, sponsored by Zillow and administered by Pulsenomics, LLC, asked panelists to predict annual changes in the U.S. Zillow Home Value Index through 2019. Additionally, experts were asked for their opinions on credit access and trends in household growth. Overall, the experts said they expect both that home values continue to rise (though at a slower pace) and that mortgage access will ease over the next few years.

Panelists predicted home values to end 2015 up 4.3 percent year-over-year. The Zillow Home Value index rose 5 percent in 2014, according to the 2015 Q1 Zillow Real Estate Market Report. Experts predicted that home value appreciation will slowly level off beginning in 2016 (3.8 percent median annual expected appreciation) and through 2019 (3 percent median annual expected appreciation).

This trajectory would see home values rise above the April 2007, bubble-era peak of $196,400 in October 2017 – almost 11 years after the prior peak – and surpass $200,000 in April 2018.

Easier Mortgages May Not Mean More Homebuyers

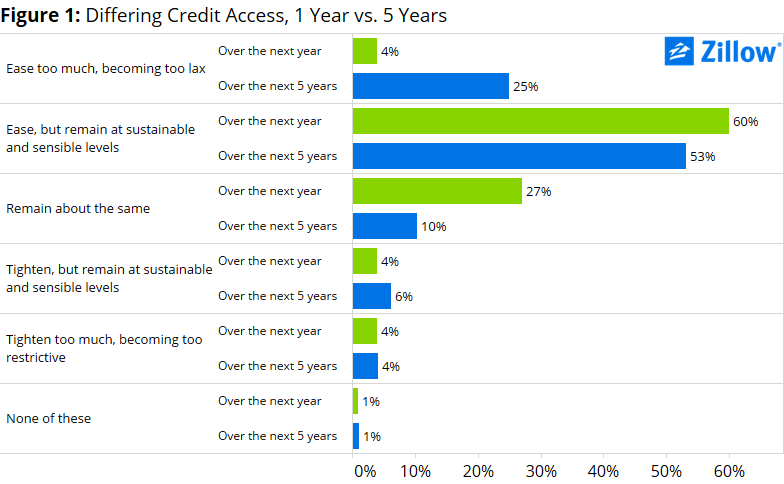

Panelists offered split opinions when asked what statement best reflects their views on the current state of mortgage credit access: 47 percent of panelists with an opinion said credit is too restrictive, and 46 percent said it is about where it should be. Another 7 percent said they feel that mortgage credit access is currently too lax.

Over the next year, the majority of panelists said they expect mortgage credit access to ease, with 60 percent saying credit will ease, but remain at “sustainable and sensible” levels. Only 4 percent of panelists with an opinion said they think credit access will ease too much over the next year, becoming too lax. When answering the same question, but over a five year period, five times as many panelists (25 percent) expressed concerns that mortgage credit access will ease too much and become too lax. Over the next five years, 78 percent of panelists with an opinion said they expected mortgage credit access to increase. Only 10 percent of respondents with an opinion said they expected mortgage credit access to tighten.

Over the next year, the majority of panelists said they expect mortgage credit access to ease, with 60 percent saying credit will ease, but remain at “sustainable and sensible” levels. Only 4 percent of panelists with an opinion said they think credit access will ease too much over the next year, becoming too lax. When answering the same question, but over a five year period, five times as many panelists (25 percent) expressed concerns that mortgage credit access will ease too much and become too lax. Over the next five years, 78 percent of panelists with an opinion said they expected mortgage credit access to increase. Only 10 percent of respondents with an opinion said they expected mortgage credit access to tighten.

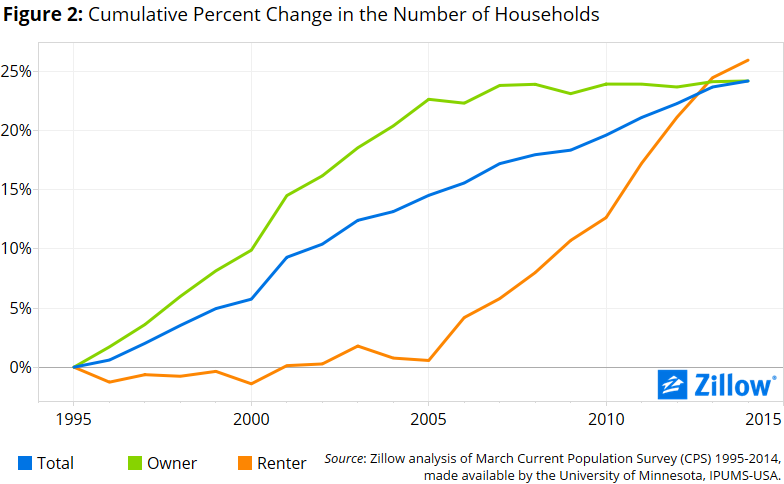

Over the past 10 years, growth in renter households has increased, whereas growth in owner households flattened after 2005 (figure 2). Panelists were asked if this trend was likely to continue over the next one to two years, or if household growth among owners would pick up.

Panelists were split between owners and renters, with 44 percent of respondents saying the current trend will continue, with renter-occupancy increasing at a significantly faster rate than owner-occupancy. But 42 percent of respondents said they thought owner-occupancy would rebound, and renter occupancy would slow. Another 11 percent of panelists with an opinion though that both owner- and renter-occupancy would increase at robust rates.

Panelists were split between owners and renters, with 44 percent of respondents saying the current trend will continue, with renter-occupancy increasing at a significantly faster rate than owner-occupancy. But 42 percent of respondents said they thought owner-occupancy would rebound, and renter occupancy would slow. Another 11 percent of panelists with an opinion though that both owner- and renter-occupancy would increase at robust rates.

Zillow predicts annual gains in rents to outpace gains in home values by the end of 2015.