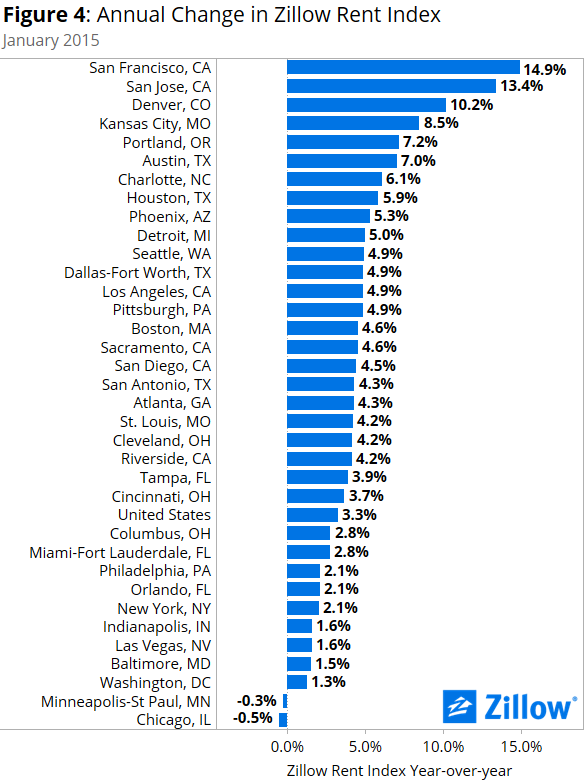

- January’s fastest growing rental markets included Denver, Kansas City, Nashville, Portland and Charlotte.

- U.S. rents were up 3.3 percent year-over-year in January, near the historical norm. But rents are rising much more rapidly in some markets. Annual rental appreciation peaked after the housing bust in September 2012 at 6.3 percent.

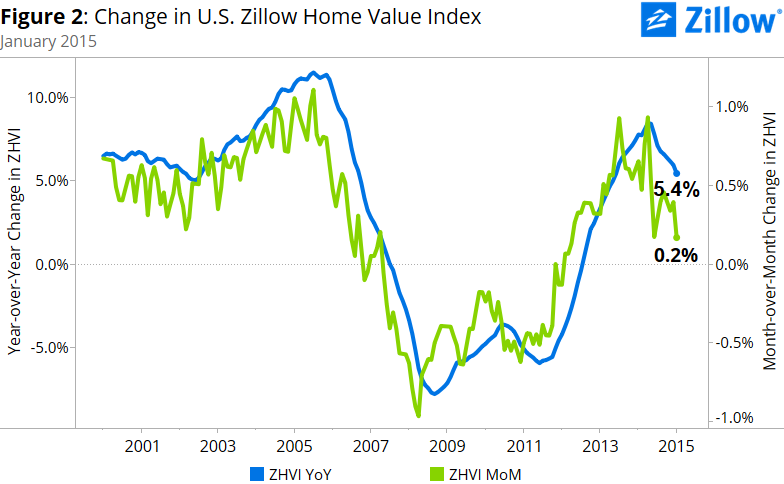

- In January, national home values rose at a slower pace, up 5.4 percent year-over-year, the ninth straight month of slowing growth.

High rents in places like New York City, Boston and the Bay Area are almost a given at this point. Increasingly, however, these old-guard markets for rapidly rising rents are having to share the spotlight with a host of smaller, less-heralded markets in the middle of the country that are becoming emblematic of a spreading rental affordability crisis.

In Kansas City, for example, barbeque isn’t the only thing cooking. The Zillow Rent Index (ZRI) in the Kansas City metro grew 8.5 percent year-over-year in January, more than twice the national pace and faster than larger places more commonly associated with high rent, including Seattle, Boston and Los Angeles. And cash-strapped renters in St. Louis, home to Budweiser, could probably use a cold one after watching rents grow 4.5 percent over the past year, just two years after rental growth was largely flat and even falling at times.

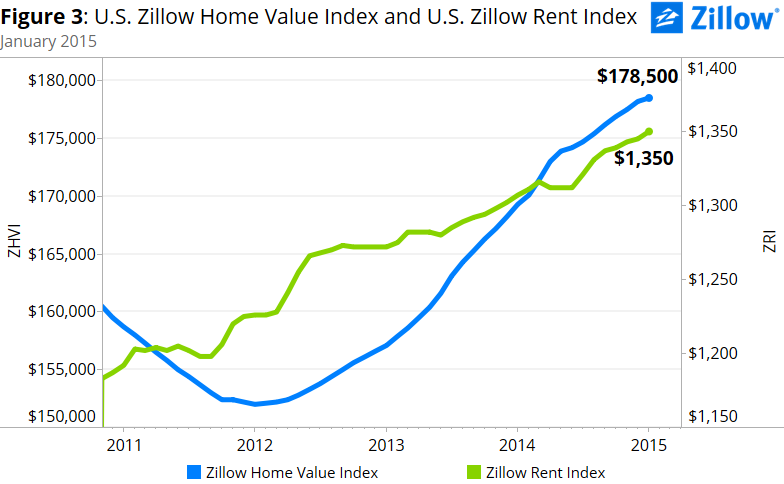

U.S. rents grew 3.3 percent year-over-year in January, to a ZRI of $1,350. The ZRI covers 859 individual metro markets nationwide, almost three-quarters of which (72 percent) experienced annual rental growth. In 367 metros, annual rental growth exceeded that of the nation as a whole, including 247 where the pace of annual rental growth was 5 percent or higher.

On its own, annual rental growth in line with the current national average is not automatically a cause for concern. What’s worrisome is that income growth has not kept pace with growth in rents. Since 2000, rents have grown at roughly twice the pace of wages, and as a result, the share of income necessary to afford typical rents in an area is rising.

Historically, U.S. renters making the national median income could expect to pay about 25 percent of their income on a typical apartment. Today, renters should expect to spend roughly 30 percent of their income on the median apartment nationwide, and more in many areas, including perhaps unexpected markets like Boulder, Colorado; Ann Arbor, Michigan; and Portland, Maine.

Widespread rental affordability challenges will have an undeniable impact on the broader housing market as a whole. Today’s renters are tomorrow’s buyers, but with more income devoted to rents, less is socked away in savings accounts for an eventual down payment on a home. This trend is particularly worrisome because for those that can find an affordable home, qualify for a loan and scrape together even a modest down payment, buying a home – in direct contrast to renting – has largely never been more affordable.

Homebuyers benefit from mortgage interest rates near historic lows and home values that remain below their pre-recession peaks in most areas. Renters have neither of those advantages – interest rates don’t impact rents, and rents never really fell to begin with, even during the recession.

And to top it off, the rental affordability crisis will likely get worse before it gets better. According to the most recent Zillow Home Price Expectations Survey, the majority of the economists and real estate experts surveyed by Zillow (51 percent) said they expected rental affordability to continue to deteriorate for at least the next two years.

So, how about that cold one?

Home Values

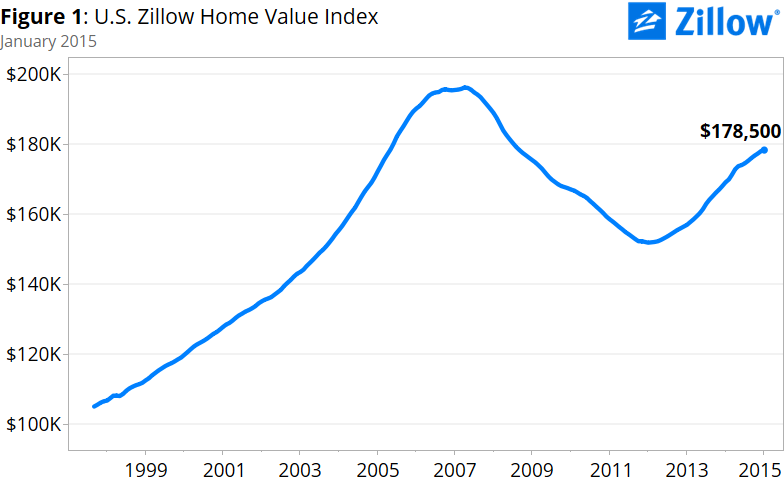

Median U.S. home values in January grew 0.2 percent from December and 5.4 percent year-over-year to a Zillow Home Value Index of $178,500. The last time national home values were at this level was in May 2005. Home values remain 9.1 percent below April 2007 peak. Annual growth in home values peaked at 8.5 percent in April 2014 and has fallen in each of the nine months since. Home values are predicted to grow 1.9 percent through January 2016.

As home value growth continues to moderate, we will see a more sustainable recovery in home values, with annual growth more in line with 3 to 5 percent historical appreciation rates. Markets that were hit especially hard during the bust (places like Atlanta, Las Vegas, Tampa and Riverside) may continue to see above-average appreciation.

The January 2015 Zillow Real Estate Market Reports cover 513 metropolitan and micropolitan areas. In January, 333 (65 percent) of these markets showed monthly home value appreciation, and 419 (82 percent) experienced annual home value appreciation.

Among the nation’s 35 largest metros, all but Indianapolis experienced year-over-year home value increases in January. Four metro areas (Cleveland, Chicago, Philadelphia and Los Angeles) experienced monthly declines in home values. Seven metro areas experienced double-digit annual appreciation in January – Denver, Miami, Houston, Austin, Atlanta, San Jose and Las Vegas.

Rents

The Zillow Rent Index (ZRI) covers 859 metropolitan and micropolitan areas, 622 (72 percent) of which experienced year-over-year gains in January. In 480 (56 percent) rents rose on a monthly basis. U.S. median rents rose 3.3 percent year-over-year in January, to a Zillow Rent Index of $1,350. Annual rental appreciation peaked in September 2012 at 6.3 percent.

The Zillow Rent Index (ZRI) covers 859 metropolitan and micropolitan areas, 622 (72 percent) of which experienced year-over-year gains in January. In 480 (56 percent) rents rose on a monthly basis. U.S. median rents rose 3.3 percent year-over-year in January, to a Zillow Rent Index of $1,350. Annual rental appreciation peaked in September 2012 at 6.3 percent.

Of the largest 35 metro areas covered by Zillow, all but Minneapolis and Chicago experienced annual gains in rents. The metro areas with the largest gains in rents were San Francisco (14.9 percent), San Jose (13.4 percent), Denver (10.2 percent), Kansas City (8.5 percent) and Portland (7.2 percent). Fifteen of the largest 50 metro areas experienced annual growth in rents of 5 percent or higher. In 367 of the metros analyzed, annual rental growth exceeded that of the nation as a whole, including 247 where the pace of annual rental growth was 5 percent or higher.

Many areas have seen the pace of rental appreciation exceed home value appreciation in the last year. While this is occurring in some of the larger, less-affordable areas we would expect—San Francisco for example—we have also observed the same pattern in Midwestern and East Coast metro areas including Kansas City, Indianapolis, Cleveland, St. Louis and Charlotte. In Kansas City, for example, rents grew 8.5 percent in the last year, while home values grew 5.9 percent. In Cleveland, rents grew two percentage points faster than home values, 4.2 percent compared to 2.2 percent. In January, rents grew faster than home values in 202 of the 490 metro areas where both Zillow Home Value Index and Zillow Rent Index data was available. This phenomenon was particularly evident in areas including Birmingham, Alabama; Louisville, Kentucky; Hartford, Connecticut; and Memphis, Tennessee.

Many areas have seen the pace of rental appreciation exceed home value appreciation in the last year. While this is occurring in some of the larger, less-affordable areas we would expect—San Francisco for example—we have also observed the same pattern in Midwestern and East Coast metro areas including Kansas City, Indianapolis, Cleveland, St. Louis and Charlotte. In Kansas City, for example, rents grew 8.5 percent in the last year, while home values grew 5.9 percent. In Cleveland, rents grew two percentage points faster than home values, 4.2 percent compared to 2.2 percent. In January, rents grew faster than home values in 202 of the 490 metro areas where both Zillow Home Value Index and Zillow Rent Index data was available. This phenomenon was particularly evident in areas including Birmingham, Alabama; Louisville, Kentucky; Hartford, Connecticut; and Memphis, Tennessee.

Inventory

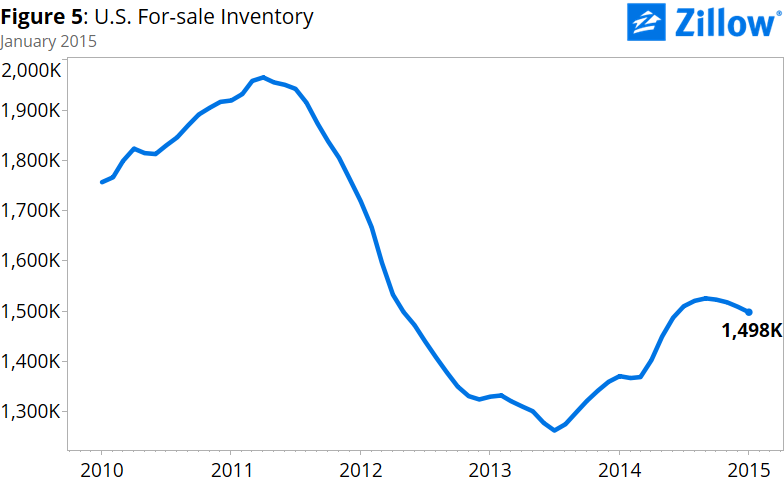

The number of homes listed for sale on Zillow was up 9.3 percent year-over-year in January, but down slightly from December (0.7 percent, seasonally adjusted). This is the fourth month in which for-sale inventory has declined compared to the month prior.

The number of homes listed for sale on Zillow was up 9.3 percent year-over-year in January, but down slightly from December (0.7 percent, seasonally adjusted). This is the fourth month in which for-sale inventory has declined compared to the month prior.

Zillow’s for-sale inventory data covers 639 metro areas. In January, for-sale inventory rose on an annual basis in 459 metro areas (72 percent). Of the largest metro areas covered by Zillow, inventory rose the most over the past year in Washington, D. C., Riverside, Las Vegas and Orlando. Compared to January 2014, there were less homes for sale during January 2015 in Phoenix, Kansas City, Houston, Dallas, Charlotte, Columbus and Denver.

Outlook

Steadily rising rents, coupled with stagnant wages, are both helping to erode rental affordability and making saving for a down payment more difficult as tenants devote an increasing portion of their incomes to rent payments each month. Increasingly unaffordable rents have made headlines in large West Coast markets including Los Angeles, San Francisco and Seattle for years. But now, rents are also seeing above-average appreciation in smaller, less flashy, non-coastal markets including Kansas City, Nashville and Charlotte. Unlike home values, which experienced a dramatic fall at the onset of the Great Recession and have largely yet to get back to pre-crisis levels, rents have largely kept chugging upward since 2000. High rental demand, both from families displaced by foreclosure during the crisis who were forced to turn to the rental market and from younger renters moving into their first apartments and staying in them longer, is also driving rents up. More apartment supply will help ease the crunch, but this won’t happen overnight.