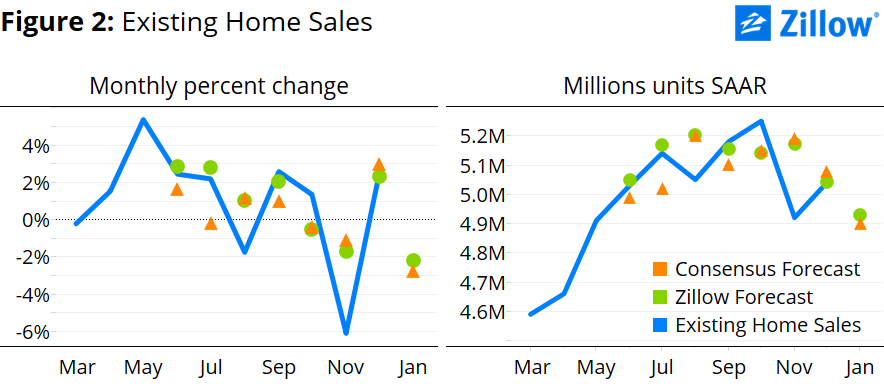

- Zillow expects existing home sales to fall 2.2 percent to 4.93 million units (SAAR) in January.

- The combination of falling interest rates and gradually improving mortgage credit availability is expected to be offset by rising prices and a falling homeownership rate.

- The effect of declining pending home sales in December is expected to outweigh recent movements in existing home sales, leaving sales lower than December.

Zillow expects Monday’s existing home sales data from the National Association of Realtors (NAR) to show a decrease of about 2.2 percent to a seasonally adjusted annual rate (SAAR) of 4.92 million units in January, down from 5.04 million units (SAAR) in December.

2014: Year in Review

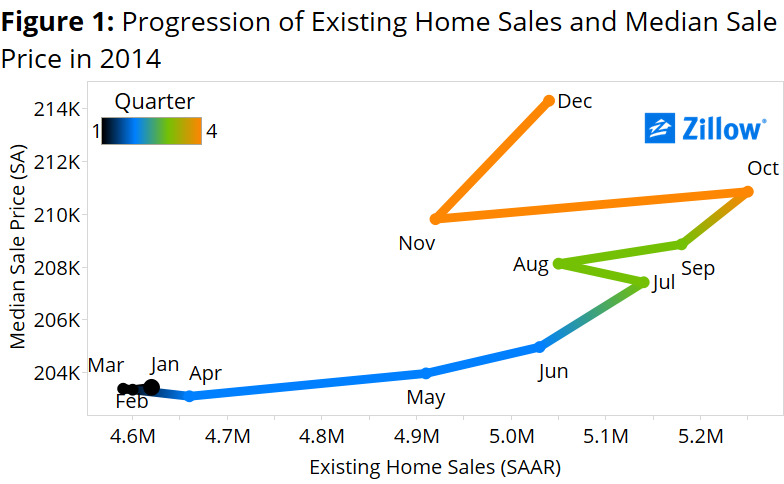

We examined the progression of existing home sales and the median sale price of existing homes in 2014 from the perspective of a supply and demand framework (figure 1). Over the first half of 2014, demand for existing homes remained fairly constant relative to supply (black and blue segments). Demand began to increase relative to supply in Q3 (green segments). Supply then retreated somewhat in Q4 (orange segments), consistent with Zillow’s for-sale-inventory series. This progression ultimately led to an increase in prices.

We examined the progression of existing home sales and the median sale price of existing homes in 2014 from the perspective of a supply and demand framework (figure 1). Over the first half of 2014, demand for existing homes remained fairly constant relative to supply (black and blue segments). Demand began to increase relative to supply in Q3 (green segments). Supply then retreated somewhat in Q4 (orange segments), consistent with Zillow’s for-sale-inventory series. This progression ultimately led to an increase in prices.

After a slow start to the year, sales of existing homes ended 2014 on a positive note, increasing to 5.04 million units (SAAR) in December, up 3.5 percent year-over-year. Sales reached their lowest point of 2014 in March, falling to 4.59 million units (SAAR) before rebounding in the second quarter, growing at an average of 3.1 percent per month between April and June. The upward momentum in sales slowed during the last half of the year, peaking at 5.25 million units (SAAR) in October. Prices moved in line with volumes over the course of the year, showing almost no growth in the first quarter but ending 2014 at a seasonally adjusted $214,300, up 6.1 percent from a year earlier.

Defying most expectations, interest rates on a 30 year fixed-rate mortgage fell steadily last year and continued to decline into January 2015, falling to 3.71 percent, down 72 basis points from a year ago[i]. This trend likely provided a modest boost to home sales overall in 2014, though the effect appears to have diminished somewhat in the fourth quarter.

After stabilizing somewhat in the second quarter, the homeownership rate continued its years-long decline, falling at a fairly constant pace of 0.11 percentage points over the last half of 2014. This decline likely tempered any demand improvements and offset the effect of falling interest rates in the latter part of the year. However, the falling homeownership rate could actually be a positive signal for future sales if the decline was driven by new renters who will sooner or later become homeowners.

The homeowner vacancy rate, on the other hand, provided mixed signals over the course of the year. It declined 0.14 percentage points over the first half of the year, signaling growing demand. It then reversed course in July, before falling again in November and December, consistent with waning home sales growth over that period.

If mortgage rates continue to remain low and the homeowner vacancy rate continues its decline, demand for existing homes should remain strong in 2015. This should be especially true if predictions that millennials will make a strong push in the housing market this year come to pass. Additionally, as prices have continued to grow, the number of homeowners in negative equity should decline. As these homeowners climb out of negative equity, selling their home becomes more attractive, further helping to ease rising demand pressures and moderate price growth.

January Forecast

Our existing home sales forecast uses a best-fit combination of two models, a structural model and a historical model. Both models point toward lower home sales in January, although the structural model suggests a smaller decrease.

The structural model suggests very little change in existing home sales, down just 0.2 percent month-over-month to 5.03 million units (SAAR). Recent changes in the underlying fundamentals are expected to cancel each other out, leaving home sales near their December level.

The historical model suggests a larger decrease of 2.3 percent to 4.92 million units (SAAR). The effect of declining pending home sales in December and the tendency for monthly changes to wash out is expected to outweigh the momentum from December’s jump, resulting in a decline in January.

Using a best-fit combination of the two models, we obtain a point forecast of 4.93 million units (SAAR), a decline of about 2.2 percent from November.

More details about our existing home sales forecast methodology can be found here.

[i] According to Primary Mortgage Market Survey data provided by Freddie Mac.