Negative Equity in Las Vegas: Deep and Durable

On October 14, Zillow will make Las Vegas the sixth stop on its Housing Roadmap to 2016 tour of America, aimed at discussing housing challenges in the cities most impacted by them. And while Vegas has a number of housing challenges, none have proven more troublesome – and long-lasting – than negative equity.

One in four homeowners with a mortgage in the Las Vegas metro, or more than 83,000, are in negative equity, or underwater – owing more on their home than it is currently worth. And this says nothing of the 3.4 percent of Las Vegas homeowners who owe twice or more what their home is worth to the bank, one of the highest rates among large markets nationwide. Home values in Las Vegas remain almost 40 percent below their pre-recession peaks, and as home value growth slows, it’s increasingly likely that many homes may never attain those values again.

In advance of our trip, we will take a deep dive into the negative equity problem in Las Vegas, as well as explore the market’s housing basics. All of our Las Vegas-specific research can be found here.

We invite you to join Zillow and our co-hosts at the Lied Institute for Real Estate Studies at the University of Nevada, Las Vegas, on October 14. If you can’t make it, don’t worry! Please follow and contribute to the discussion on social media using the hashtag #HousinginAmerica. We look forward to hearing from you.

More than nine years after Las Vegas’ housing market began its epic collapse, things are looking better. But daily reminders of one of the nation’s most dramatic local boom-and-bust periods remain in and around Las Vegas, especially the long shadow of negative equity.

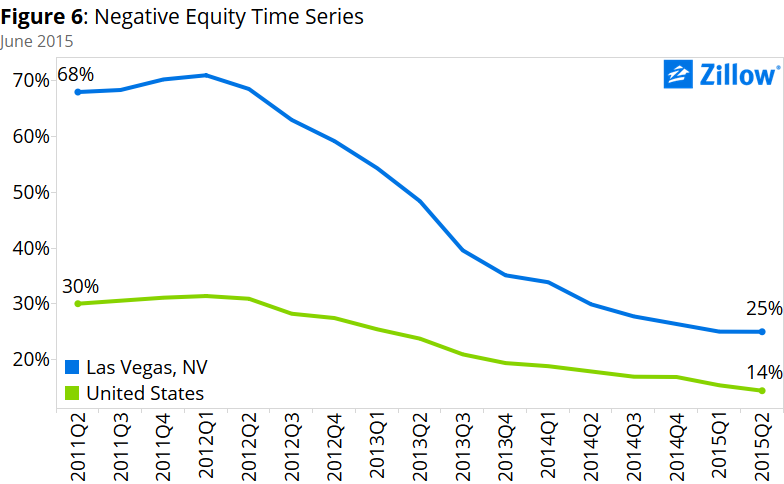

Negative equity occurs when homeowners owe more on their mortgage than what their home is actually worth, also known as being “underwater.” For 17 straight quarters, the negative equity rate in the Las Vegas metro has been the highest among the nation’s largest markets, peaking at 71 percent in the first quarter of 2012. Through the second quarter of 2015, the negative equity rate in and around Las Vegas has fallen to 25 percent, a healthy decline from peak, but still the highest rate in the nation among other large metros. And in more normal times and typical markets, negative equity is generally as low as 1 percent to 3 percent.

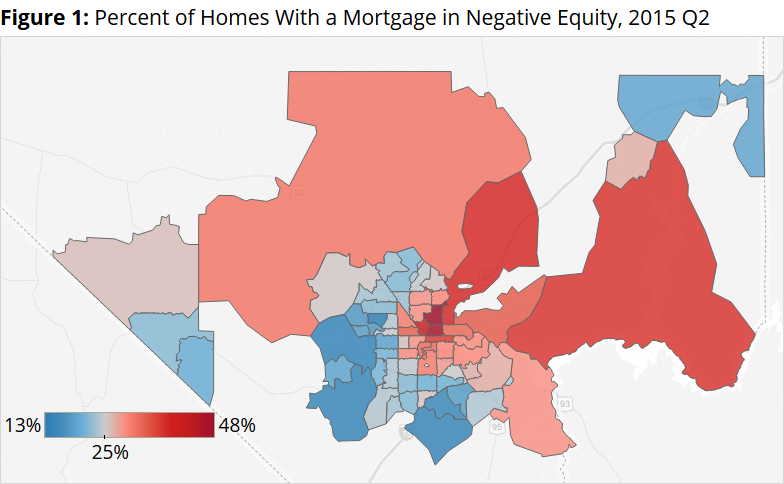

So Las Vegas still has a long way to go before negative equity will no longer impact the local housing market. The rate remains very elevated in many parts of the metro (figure 1).

So Las Vegas still has a long way to go before negative equity will no longer impact the local housing market. The rate remains very elevated in many parts of the metro (figure 1).

For many, negative equity is an academic issue – they can afford the payments on their current home, and plan on staying there long-term, so the practical impacts of negative equity are muted. But the nature of negative equity is such that it can distort housing markets in huge ways, even if individual homeowners aren’t affected or are only touched on paper.

If and when it comes time to sell, most underwater homeowners realistically can’t sell their home, unless they bring sometimes substantial amounts of their own cash to the closing table in order to satisfy their outstanding mortgage balance, or are able to arrange a short sale with their lender. And there are typically only two ways to clear negative equity from the books outside of cash at closing or a short sale.

In most cases, an underwater homeowner will simply wait for their home’s appreciation alone to bring them back above water. This isn’t as unrealistic as it might seem at first blush, given that just two years ago, in October 2013, annual Las Vegas home value growth reached a post-recession peak of a whopping 29 percent per year, helping bring the negative equity rate down precipitously. But lately, that growth has slowed to a roughly 7 percent pace. While this is still a very healthy rate of appreciation, it has caused the pace of reduction in negative equity to slow dramatically, and even pause. For the past two quarters, the area’s negative equity rate has remained unchanged at 25 percent.

The second way to clear negative equity is through foreclosure. Because underwater homeowners are often locked into their homes and can’t sell in an emergency, they’re less able to absorb life’s curveballs – things like a lost job, costly car repair or a surprise medical expense. In these situations, when something has to give, the thing that often does end up giving is their mortgage payment. These homeowners often fall into delinquency and eventually foreclosure.

Once a home is foreclosed – either because a homeowner can’t keep up with mortgage payments, or because they simply choose not to – negative equity is wiped clean. At the peak of the foreclosure crisis, roughly 60 of every 10,000 homes in the Las Vegas area was foreclosed upon, six times the national rate. These homes exited the foreclosure pipeline as foreclosure re-sales, or REOs, often sold by the lender that had taken them back in the first place at a sometimes drastically reduced price. An abundance of homes listed for sale at a lower-than-market-value price helped to further bring prices down on those homes not in negative equity.

On top of it all, negative equity is not an equal opportunity offender. Negative equity is overwhelmingly concentrated in condominiums and the lowest-priced homes – the exact homes most likely to be sought by current renters, first-time buyers and young families. Lower-end homes, those homes valued in the bottom one-third of all home values, were much harder-hit during the housing bust than top-tier homes. From the market’s peak through its bottom, homes in the bottom tier lost a median of 74 percent of their value, versus “just” 55 percent at the median for top-tier homes. As a result, the negative equity rate among bottom-tier Las Vegas homes is currently about 38 percent, compared to 17 percent for top-tier homes.

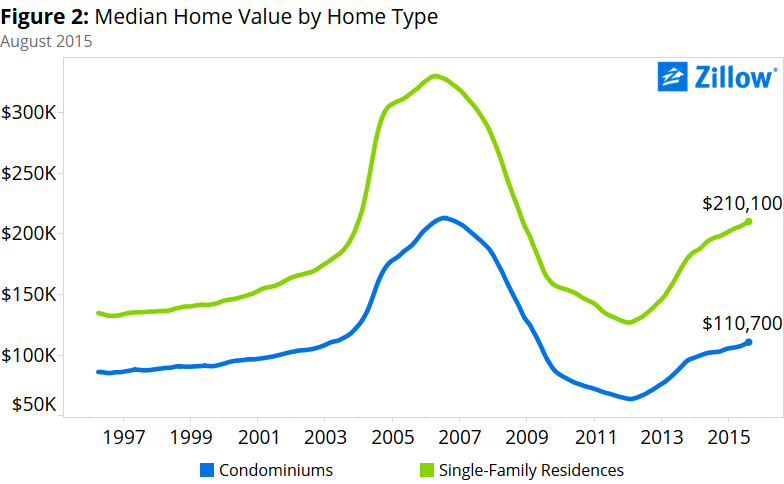

It’s a similar story for condos versus single-family homes. Condos and co-operative homes in the Las Vegas area lost 70 percent of their value, at the median, while single-family homes lost about 62 percent (figure 2). Currently, 37 percent of condominiums in the Las Vegas area are underwater, compared to 24 percent of single-family homes.

It’s a similar story for condos versus single-family homes. Condos and co-operative homes in the Las Vegas area lost 70 percent of their value, at the median, while single-family homes lost about 62 percent (figure 2). Currently, 37 percent of condominiums in the Las Vegas area are underwater, compared to 24 percent of single-family homes.

However, the bottom tier of homeowners is not only more likely to be underwater, but also more likely to be deeper underwater than the top tier. At its worst in the first quarter of 2012, more than one in four mortgaged Las Vegas homeowners owed their lender more than double what their home was worth, with many of these homeowners located in the bottom tier. And problems at the bottom cause ripples throughout the entire market.

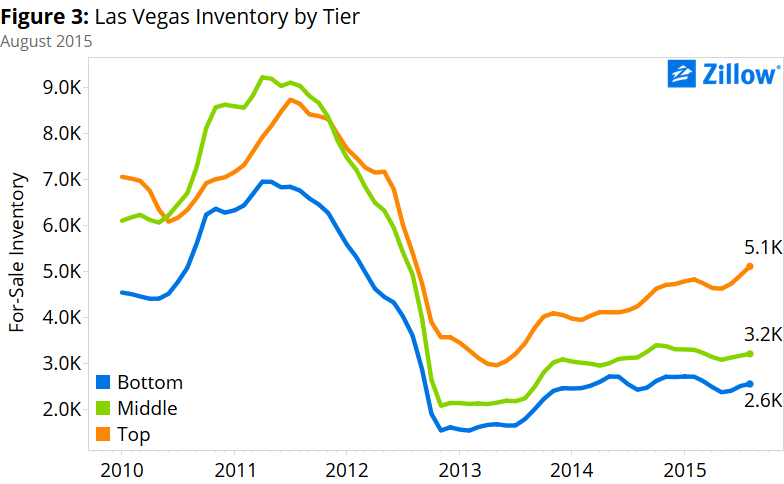

As noted above, negative equity’s impacts are numerous. Negative equity will help increase the number of foreclosures, and these in turn will continue to depress the market. In turn, whole neighborhoods may become blighted, increasing the chances of local home value volatility. Last but not least, and perhaps most importantly long-term, negative equity can depress inventory levels, especially of bottom-end homes (figure 3). If many homeowners are locked into their homes because of negative equity, those homes that would normally change hands on the open market now no longer do. And homeowners that would normally upgrade to the next home don’t. This means fewer entry-level and starter homes are made available, and first time homebuyers have a hard time finding a home.

As noted above, negative equity’s impacts are numerous. Negative equity will help increase the number of foreclosures, and these in turn will continue to depress the market. In turn, whole neighborhoods may become blighted, increasing the chances of local home value volatility. Last but not least, and perhaps most importantly long-term, negative equity can depress inventory levels, especially of bottom-end homes (figure 3). If many homeowners are locked into their homes because of negative equity, those homes that would normally change hands on the open market now no longer do. And homeowners that would normally upgrade to the next home don’t. This means fewer entry-level and starter homes are made available, and first time homebuyers have a hard time finding a home.

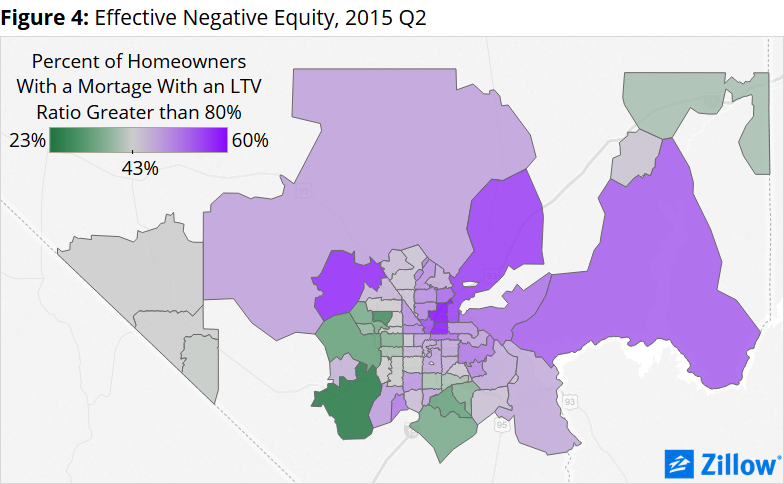

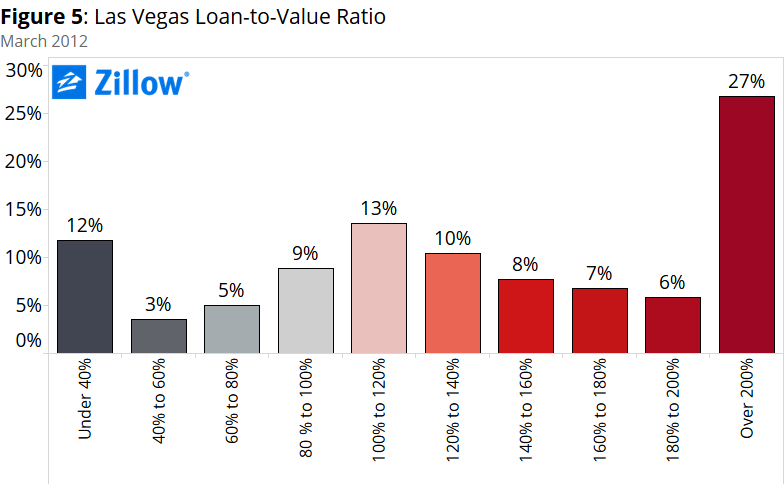

Given the slowdown in home value growth and the rate at which negative equity is receding, negative equity may be part of the new normal for the Las Vegas market for years to come. This is especially true since negative equity can have an impact even if a homeowner isn’t officially underwater. Typically, when a homeowner sells a home, they then use the proceeds from that sale to help cover the down payment and closing costs associated with buying a new home. But even if a homeowner has some equity in their home, it may not be enough to comfortably cover those costs. Counting those homeowners with a loan-to-value ratio of 80 percent or higher (those with 20 percent or less equity in their home), the so-called “effective” negative equity rate in and around Las Vegas is even higher, at 43.2 percent (figure 4).

Given the slowdown in home value growth and the rate at which negative equity is receding, negative equity may be part of the new normal for the Las Vegas market for years to come. This is especially true since negative equity can have an impact even if a homeowner isn’t officially underwater. Typically, when a homeowner sells a home, they then use the proceeds from that sale to help cover the down payment and closing costs associated with buying a new home. But even if a homeowner has some equity in their home, it may not be enough to comfortably cover those costs. Counting those homeowners with a loan-to-value ratio of 80 percent or higher (those with 20 percent or less equity in their home), the so-called “effective” negative equity rate in and around Las Vegas is even higher, at 43.2 percent (figure 4).

Put another way, almost half of Las Vegas homeowners with a mortgage likely can’t sell their home currently without incurring a lot of personal costs.

Put another way, almost half of Las Vegas homeowners with a mortgage likely can’t sell their home currently without incurring a lot of personal costs.

This new normal might eventually force local homeowners and policymakers to find creative ways to live with negative equity and work around it. And believe it or not, that is possible, and there’s reason for hope. The negative equity rate in Las Vegas remains the highest among large American metros, but it has also fallen by 46 percentage points since peaking in early 2012, the largest decline among those same metros over that time. Federal loan modification and refinance programs have provided a template for ways to help homeowners manage negative equity. And Las Vegas residents themselves are optimistic: Expectations for future market performance among Vegas residents are relatively high compared to other markets across the country, and have improved dramatically in just a short time.

{kind=link}