Using High-Frequency Interest Rate Data from Zillow’s Online Mortgage Marketplace

To many observers of U.S. mortgage markets, it is obvious that interest rates respond to policy decisions from the Federal Reserve Board, particularly when these decisions are unexpected. Financial news and investors pay careful attention to the precise wording and delivery of monetary policy statements, looking for insights into the future direction of the key policy interest rate—known as the Federal Funds Rate—that is managed by the Fed and that influences the full spectrum of U.S. lending and borrowing terms. Like other interest rates, mortgage rates are closely tied to Fed policy, particularly for adjustable rate mortgages, but also for more common fixed rate mortgages.[1]

There is a rich literature studying the impact of Fed monetary policy statements on a wide array of markets. Most of this research has focused on markets where high-frequency data are widely available—such as in stock, bond, commodities, futures, and foreign exchange markets—to allow precise identification of narrow time frames during which markets are expected to respond to a specific piece of macroeconomic news.[2] Measuring these responses has proven more difficult when it comes to mortgage rates, due in part to the relative paucity of high-frequency data on mortgage rates.

The most commonly used source of data on mortgage rates is the Freddie Mac Primary Mortgage Market Survey (PMMS), which surveys around 125 lenders nationwide each week between Monday and Wednesday. The data are compiled and published on Thursday. However, because of the design of the survey, the PMMS can systematically fail to capture changes to mortgage rates that occur late in the week—for example, responses to monetary policy statements from the Fed which are typically released on Wednesday afternoons.[3] In particular, when the Fed statements surprise markets late on Wednesday, the PMMS essentially becomes substantially less informative well before publication.

On weeks when the Fed surprises markets, or when other market-moving news breaks late in the week, mortgage quote data from the Zillow Mortgage Marketplace (ZMM)—a free online marketplace that connects thousands of borrowers and lenders each day—may provide more timely insight into the rates that mortgage lenders are offering.[4] In this Research Brief, we assess the degree to which mortgage quotes on Zillow track mortgage rates reported by the PMMS, and we use the Zillow data to test whether mortgage rates systematically respond to surprise monetary policy pronouncements.

1. How do rates quoted on ZMM compare to rates reported by Freddie Mac?

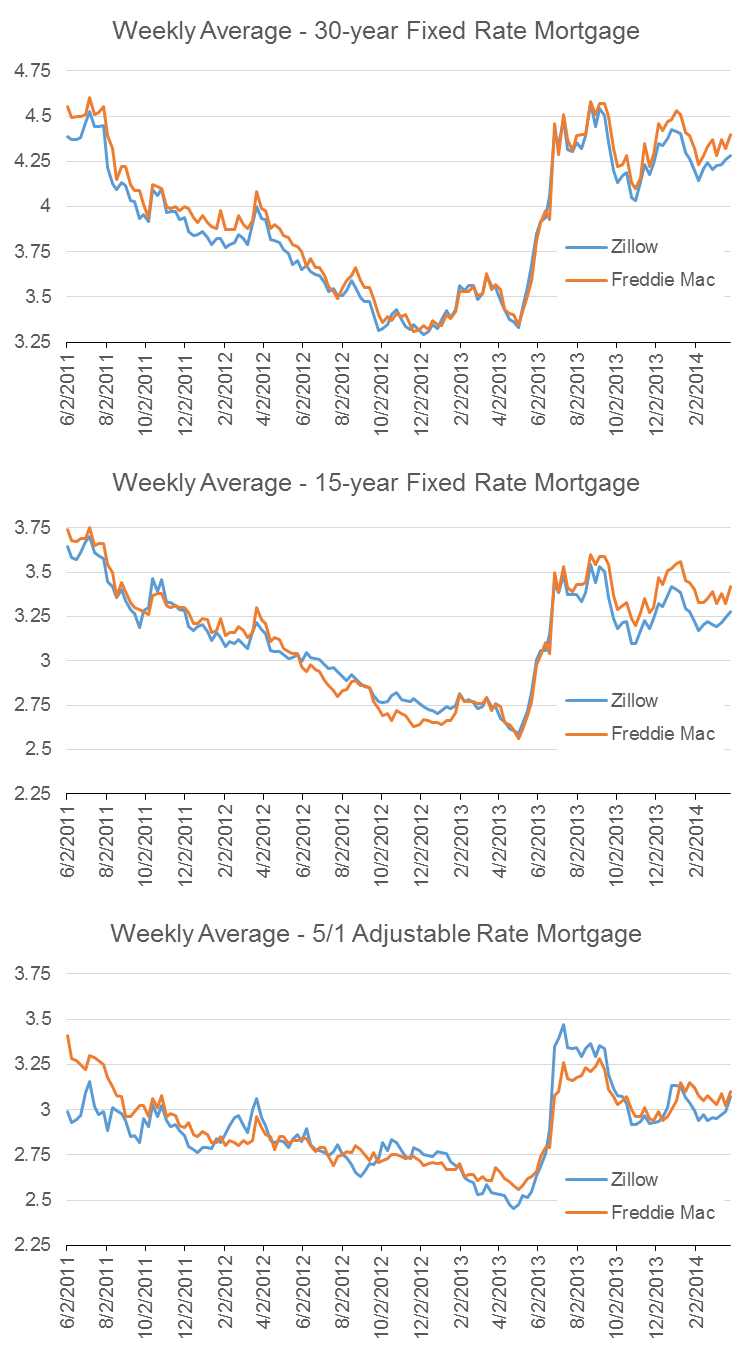

The Freddie Mac and Zillow data track each other very closely. Between June 2011 and March 2014, the rate reported in PMMS and the average rate quoted on Zillow between Monday and Friday of a given week moved together 99.2 percent of the time for the 30-year fixed rate mortgage, 97.9 percent of the time for the 15-year fixed rate mortgage, and 85.1 percent of the time for the 5/1 adjustable rate mortgage. The lower correlation between the PMMS and Zillow data on adjustable rate mortgages could reflect rapidly evolving market conditions and the faster response of adjustable rate mortgages to market movements. The three graphs to the right show the average rates reported in the two data series for the 30-year and 15-year fixed rate mortgages, and for the 5/1 adjustable rate mortgage.

Despite the close correlation, the average rate quoted on ZMM is slightly below the rate reported by Freddie Mac across a range of mortgage products. Over the sample period, the Freddie Mac rate is 5 basis points above the Zillow rate for the 30-year fixed rate mortgage, 3 basis points higher for the 15-year fixed rate mortgage, and 2 basis points higher for the 5/1 adjustable rate mortgage.[5] This difference could reflect a range of factors, such as greater competition in online marketplaces where borrowers can more easily compare offers, or potentially different credit characteristics between online versus brick-and-mortar mortgage shoppers.

The question naturally arises as to whether the average rate quoted on ZMM or the average rate reported in the PMMS more accurately represents the “true” state of the market. Unfortunately, there is no straightforward answer to this deceivingly simple question. The PMMS surveys lenders and then weights these responses according to mortgage volumes reported in the most recent Home Mortgage Disclosure Act (HMDA) data. Since HMDA data are typically published in mid-September of the following year, these weights reflect market conditions that are anywhere from nine to 21 months out of date. This can bias the averages reported by PMMS, particularly when market conditions are changing rapidly. By contrast, the Zillow data more closely capture current market conditions, but as suggested above, may be biased to the extent that borrowers who shop for a mortgage online differ in terms of key lending characteristics—such as income, credit history, or loan-to-value—from other borrowers.

2. Do mortgage rates respond to Fed news?

To assess whether markets respond to monetary policy statements from the Fed, we rely on the higher frequency of the Zillow data to conduct two tests.

- The first test uses the Zillow data to check whether, in weeks when there is an unexpected Fed statement, there is a jump between the average rate quoted on Monday and Tuesday, and the average rate quoted on Thursday and Friday.

- The second test checks whether Zillow’s Monday/Tuesday data or its Thursday/Friday data are closer to the rates reported by Freddie Mac in weeks when the Fed surprises markets.

These tests pose unique (although not uncommon) econometric challenges. Markets typically have strong expectations about the content of monetary policy statements and these expectations are incorporated into interest rates well in advance of Fed pronouncements. When market expectations prove accurate, interest rates do not respond to the Fed. However, when market priors prove wrong, and the Fed surprises markets, this new information is rapidly incorporated into interest rates. Mirroring other studies that attempt to capture market responses to macroeconomic news, we study the historical record to gauge market expectations. In this case, we classify a “surprise” Fed statements as one where contemporaneous news reports characterize the statement as unexpected.[6] By our reading of the historical record, of the 25 Federal Open Market Committee statements between June 2011 and March 2014, 11 are categorized as “surprises.”

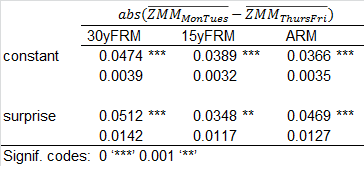

The first test shows that there is typically a jump between the average rate quoted early in the week (on Monday and Tuesday) and the average rate quoted late in the week (on Thursday and Friday). However, this gap roughly doubles in weeks when there the Fed surprises markets. In the table below, we show the results of a regression of the absolute difference between the average Monday/Tuesday rate quoted on Zillow, and the average Thursday/Friday rate, on a constant and a dummy indicating whether the Fed surprised markets or not in a given week. For the 30-year fixed rate mortgage (column labeled 30yFRM), the results show that in weeks when there is no unexpected news from the Fed, rates change by around 5 basis points between the early part of the week and the later part of the week. In weeks when there is unexpected news from the Fed, the average change is closer to 10 basis points (4.7 plus 5.1). For the 15-year fixed rate mortgage (column labeled 15yFRM), the change is 4 basis points when there is no news from the Fed versus 7 basis points when there is news from the Fed.

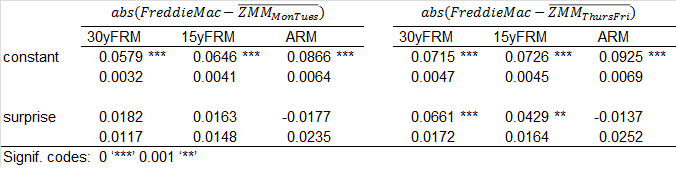

The second set of tests show that the differences between the Freddie Mac and Zillow data in weeks when the Fed surprises markets is driven almost entirely by quotes later in the week. When we compare the difference between the Freddie Mac rates and the average Zillow rates quoted on Monday/Tuesday of a given week, there does not appear to be a significant response to Fed surprises, as the table below illustrates. However, when we compare the difference between the Freddie Mac rates and the average Zillow rates quoted on Thursday/Friday of a given week, there is a strongly significant response to Fed surprises—at least in the case of the 30-year and 15-year fixed rate mortgage. (In this test, the 5/1 adjustable mortgage rate does not appear to significantly respond to Fed news, although this may result from a relatively short time series or other statistical noise in the data.)

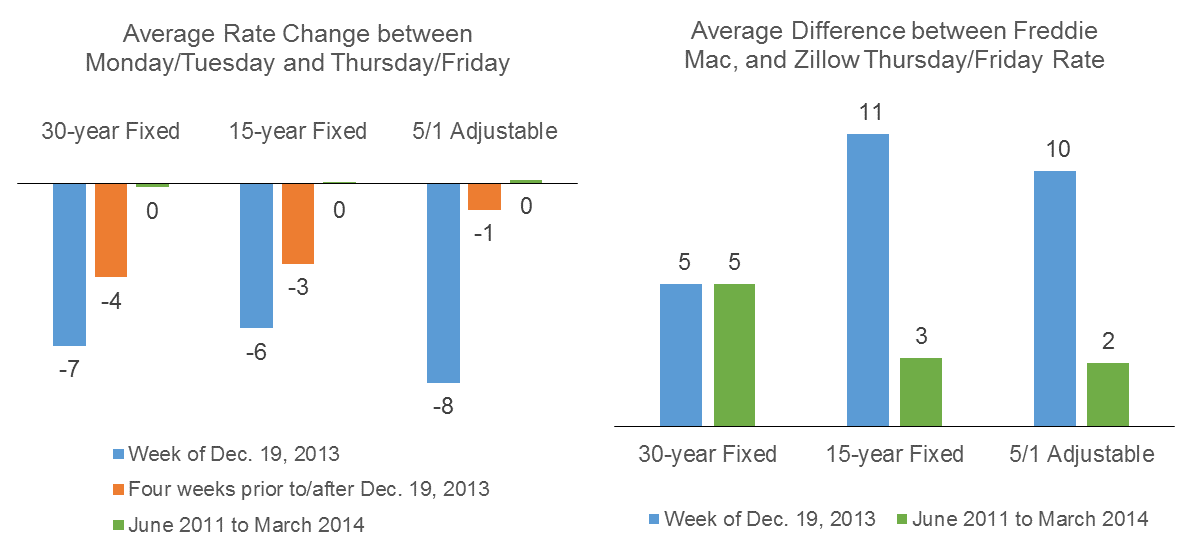

As an example, consider the FOMC’s statement on Dec. 19, 2013, when the Fed surprised markets with its decision to not begin to slow its purchases of U.S. Treasury and Mortgage Backed securities, commonly referred to as “tapering”. Markets had widely expected the FOMC to begin its taper of asset purchases, but they were wrong.

The average 30-year fixed rate mortgage rate quoted on ZMM the two days prior to the announcement was 4.35 percent, but the average rate for the subsequent two days was 4.42 percent, a change of 7 basis points, as illustrated by the blue bars in the graph on the left below. For 15-year fixed rate mortgages, the average changed 6 basis points from 3.34 percent to 3.40 percent, and for 5/1 adjustable rate mortgages, the average changed 8 basis points from 2.97 percent to 3.06 percent. As the graph below illustrates, these changes were much larger than the average inter-week changes in the preceding and subsequent four weeks (orange bars), and over the full June 2011 to March 2014 sample period (green bars).

By comparison, the PMMS rates reported for that week were 4.47 percent, 3.51 percent, and 2.96 percent for the 30-year fixed, 15-year fixed, and 5/1 adjustable rate mortgages, respectively. Compared to the average rate quoted on Zillow on Thursday and Friday, these rates were roughly normal in the case of the 30-year fixed-rate mortgage, but were much larger than normal in the cases of the 15-year fixed rate and 5/1 adjustable rate mortgages (graph on the right below).

Overall, the data presented in this Research Brief suggest that while Freddie Mac’s Primary Mortgage Market Survey is one of the most commonly referenced sources of mortgage rate data—and is even the source of information in official data reports such as the Federal Reserve Board’s Weekly Selected Interest Rates Statistical Release[7]—it can systematically fail to capture rate movements that occur late in the week. In these instances, Zillow’s real-time mortgage rates more accurately reflect market conditions and can be a more reliable resource for determining mortgage rate movements. Using Zillow’s unique high frequency data on mortgage rates, we identify a strongly significant response of mortgage rates to unexpected policy pronouncements from the Federal Reserve, a conclusion that would be impossible to test using lower frequency data.

[1] See Carlos Garriga, Finn E. Kydland, and Roman Šustek, “Mortgages and Monetary Policy,” Federal Reserve Bank of St. Louis, Working Paper 2013-037A, December 2013.

[2] For example, see Magnus Andersson, “Using Intraday Data to Gauge Financial Market Responses to Federal Reserve and ECB Monetary Policy Decisions,” European Central Bank, Working Paper No. 726, February 2007; Ben S. Bernanke and Kenneth N. Kuttner, “What Explains the Stock Market’s Reaction to Federal Reserve Policy?” Board of Governors of the Federal Reserve, Working Paper 2004-16, March 2004; Kenneth Kuttner, “Monetary Policy Surprises and Interest Rates: Evidence from the Fed Funds Futures Market,” Federal Reserve Bank of New York, Staff Report 99, February 2000.

[3] According to Freddie Mac’s website, most survey responses are received by Tuesday, with smaller numbers arriving on Wednesday. See the response to third question at “Primary Mortgage Market Survey FAQs.”

[4] Every Tuesday, the Zillow Mortgage Rate Ticker is released, and reports the most recent changes in the market.

[5] A basis point is .01 percent.

[6] When contemporaneous news reports overwhelmingly refer to the Fed statement as containing “no surprises” or “as expected”, the statement is not classified as a surprise.

[7] See footnote 16 at Federal Reserve Board, Selected Interest Rates (Weekly)—H.15.