Negative Equity Falling Faster Among Less-Expensive Homes

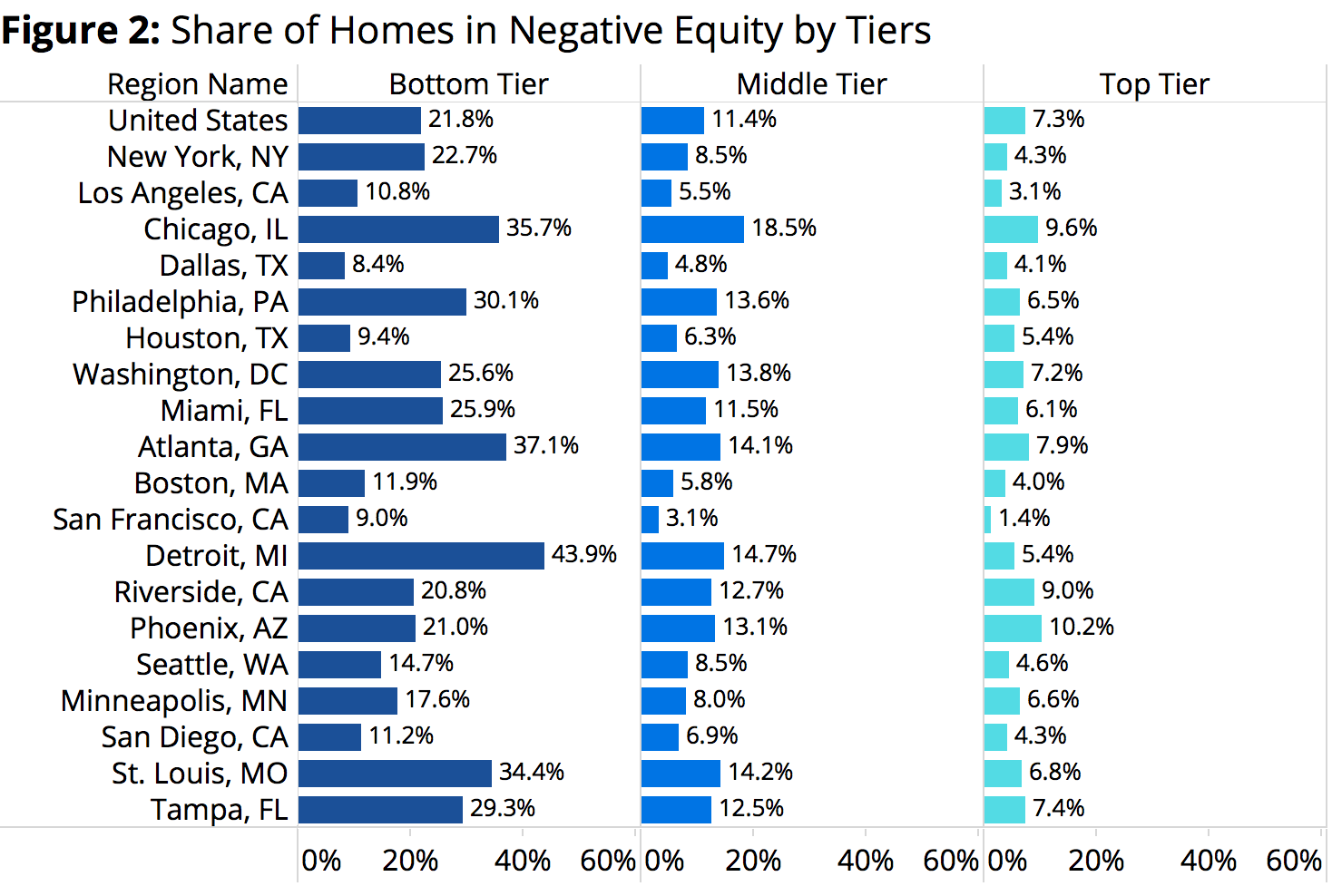

The overall negative equity rate among bottom-tier homes nationwide was 21.8 percent in Q1, compared to 7.3 percent among top-tier homes, 11.4 percent for middle-tier homes and 12.7 percent for all U.S. homes.

- The overall negative equity rate among bottom-tier homes nationwide was 21.8 percent in Q1, compared to 7.3 percent among top-tier homes, 11.4 percent for middle-tier homes and 12.7 percent for all U.S. homes.

- The negative equity rate among bottom-tier homes has fallen 3.7 percentage points in the past year. Middle-tier negative equity has fallen by 2.7 percentage points and top-tier negative equity has fallen by 1 percentage point. Over the same period, the negative equity rate among all U.S. homes fell 2.7 percentage points.

Owners of the east-expensive homes were roughly three times more likely to be underwater on their mortgage than owners of the most-expensive homes in markets nationwide as of the end of Q1 2016. But the negative equity rate for those less-expensive, entry-level homes has fallen faster over the past year than for middle- and top-tier homes as entry-level home value appreciation picked up.

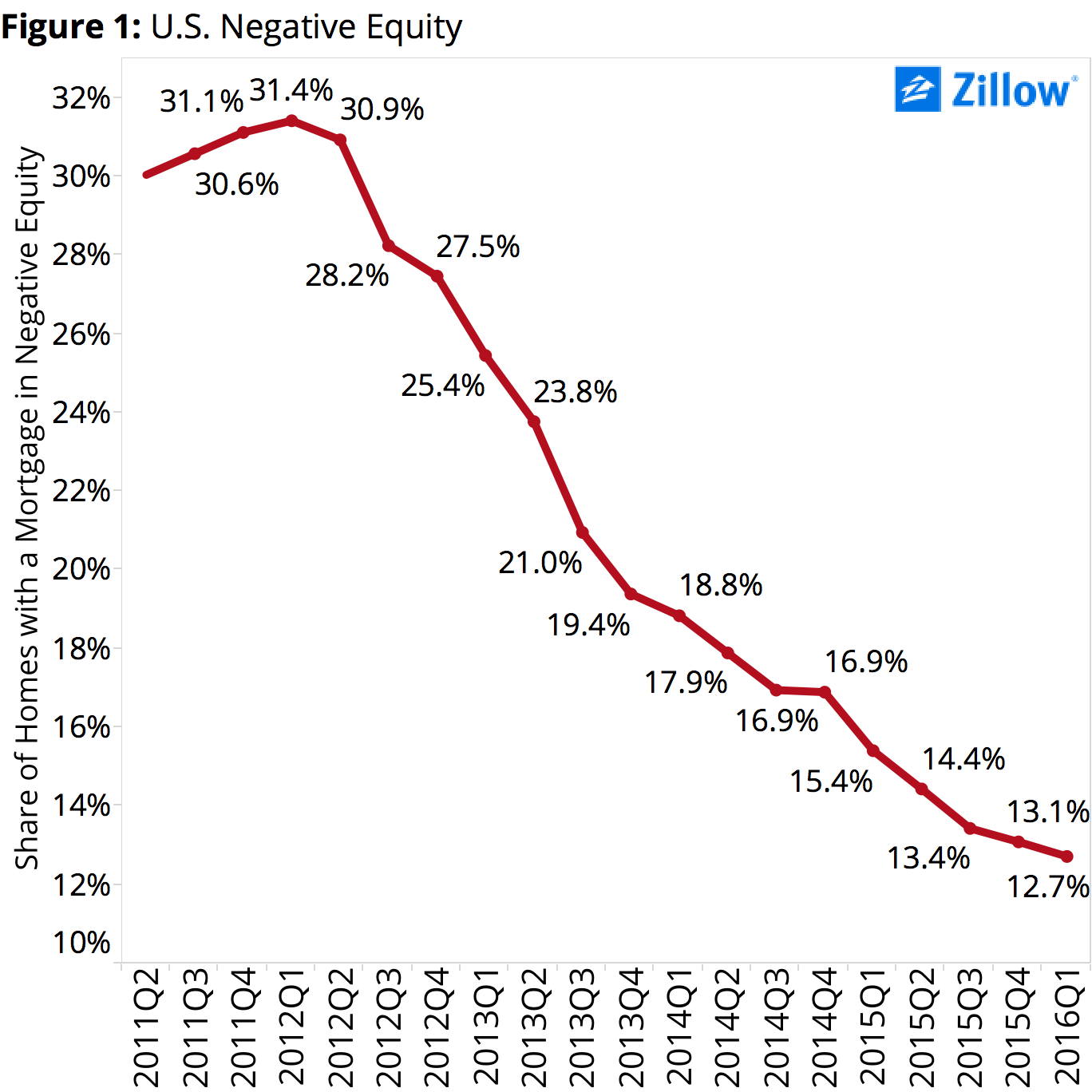

The overall negative equity rate among bottom-tier homes nationwide was 21.8 percent in Q1, compared to 7.3 percent among top-tier homes, 11.4 percent for middle-tier homes and 12.7 percent for all U.S. homes (Figure 1). Among the 35 largest metros, Detroit (43.9 percent), Cleveland (37.7 percent) and Atlanta (37.1 percent) had the highest share of bottom-tier homes in negative equity in Q1.

The overall negative equity rate among bottom-tier homes nationwide was 21.8 percent in Q1, compared to 7.3 percent among top-tier homes, 11.4 percent for middle-tier homes and 12.7 percent for all U.S. homes (Figure 1). Among the 35 largest metros, Detroit (43.9 percent), Cleveland (37.7 percent) and Atlanta (37.1 percent) had the highest share of bottom-tier homes in negative equity in Q1.

That the bottom third of the market was hit disproportionately hard by negative equity, and has been slow to recover, is not exactly a new story. But comparing negative by tiers over time reveals a somewhat different, if not exactly surprising, story: Over the past year, negative equity in the bottom tier has been receding more quickly than other tiers. And in some markets, much more quickly.

As of Q1 2015, the bottom-tier negative equity rate stood at 25.5 percent, compared to 8.3 percent at the top and 14.1 percent for the middle. In other words, the negative equity rate among bottom-tier homes has fallen 3.7 percentage points in the past year. Middle-tier negative equity has fallen by 2.7 percentage points and top-tier negative equity has fallen by 1 percentage point. Over the same period, the negative equity rate among all U.S. homes fell 2.7 percentage points.

In Seattle, bottom-tier negative equity fell 9.2 percentage points from Q1 2015 to Q1 2016 (23.8 percent to 14.7 percent), compared to just a 1 percentage point drop among top-tier Seattle homes (5.69 percent to 4.64 percent) – the largest such difference among big U.S. metros. In Columbus, bottom-tier negative equity fell 8.8 percentage points, compared to 1.2 points at the top. The bottom-tier negative equity rate in Atlanta fell 8.9 points, compared to just 2.1 points among top-tier homes (Figure 2).

There’s a few reasons for this trend, not the least of which is that negative equity in the bottom tier simply has farther to fall compared to already-low levels of negative equity at the top. But the most obvious reason behind the different speeds at which negative equity is falling among different home value tiers boils down to simple differences in home value growth. Growing home values means shrinking negative equity. And while home values have grown across the board fairly consistently since the housing market hit bottom in early 2012, over the past year bottom-tier home values have grown much faster, in most markets, than top-tier values and home values overall. Between Q1 2015 and Q1 2016, bottom-tier median home values grew 7.6 percent. Over the same period, top-tier median home values grew 4.3 percent.

In the long-run, this combination of faster home value growth and more quickly receding negative equity at the bottom end of the market should prove to be a positive. It’s true that rapid appreciation on its own at the bottom end may price some entry-level buyers out of the market before they even have a chance to get in.

But for owners of bottom-tier homes, this rapid appreciation is a boon, especially if they’re underwater. And a big reason why appreciation is so rapid at the bottom is precisely because so few homes are available for sale in part because so many are locked in negative equity. If this fast growth continues, it’s more likely bottom-tier underwater owners will be able to get back into positive equity more quickly (assuming they’re not too far deep underwater to begin with). For buyers, this means it’s more likely they’ll be able to find a home to buy as more previously underwater owners re-surface and begin to list their homes for sale.

At least, eventually. In the meantime, the slow march back to a balanced market will continue.

{kind=link}