Uncategorized

October Case-Shiller: U.S. Housing Market Continues to Accelerate

The national housing market is continuing to put last decade’s recession in the rearview mirror, according to October Case-Shiller data, accelerating from last month in line with expectations and continuing to reach new highs.

The national housing market is continuing to put last decade’s recession in the rearview mirror, according to October Case-Shiller data, accelerating from last month in line with expectations and continuing to reach new highs.

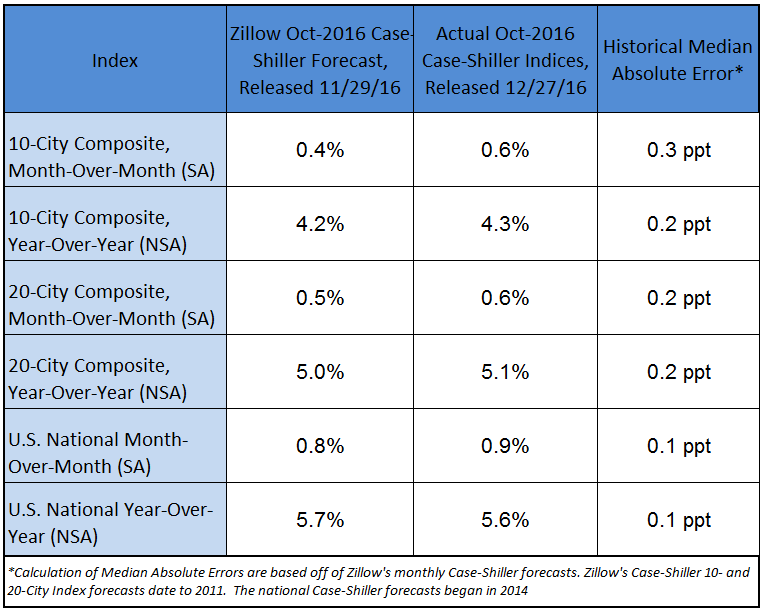

On an annual basis, October Case-Shiller data showed the U.S. national index up 5.6 percent from October 2015 through October 2016, up from 5.4 percent annual growth reported in September. The national home price index is now 0.2 percent above its July 2006 peak level, according to a statement from S&P Dow Jones, which publishes the S&P CoreLogic Case-Shiller Indices.

Seasonally adjusted prices in the national index were up 0.9 percent in October from September, up from monthly growth of 0.8 percent in September. Sustained monthly growth at those levels would translate into annual growth well above 10 percent, a very rapid pace that, coupled with rising mortgage interest rates and much slower wage growth, could soon begin to dent home affordability nationwide. Seasonally adjusted home prices in both the 10- and 20-city composite indices rose 0.6 percent in October from September. Year-over-year, the 10-city index was up 4.3 percent and the 20-city index was up 5.1 percent.

Below are Zillow’s forecasts of September Case-Shiller data, along with the actual September Case-Shiller numbers released today.

Growth in home prices has been accelerating in recent months, reaching levels not seen in many markets since the housing bubble days. Current appreciation rates are similar to back then, but that should be where the comparisons end. A decade ago, growth in the housing market was driven primarily by loose and predatory lending, speculation and over-building – forces that only served to artificially inflate and overheat the market. The growth we’re seeing today is, instead, a natural reaction to basic economic fundamentals. More and better opportunities for American consumers means high demand for housing, and that demand is not being met by an adequate supply of homes for sale – and so prices rise. Rapid growth in home prices may not be welcome news for those struggling to save to buy a home, and coupled with rising interest rates in coming years, some consumers may begin to feel the pinch of worsening affordability, especially in pricier coastal markets. But widespread, rapidly rising national home values themselves should not be confused with a widespread, rapidly inflating national housing bubble. History is not repeating itself, and there is little risk of that happening as long as the national market continues to be driven by fundamentals.

{kind=link}