Renters by Choice or Circumstance? Many Big-City Renters Earn Enough to Buy

The homeownership rate has steadily declined to generational lows over the past decade, pushing a broader-than-ever swath of Americans from all social and economic backgrounds into the rental market – including a large share that could likely afford to buy a home, but aren’t.

- As the homeownership rate has declined over the past decade, a broader socio-economic swath of Americans are renting than at any time in recent history.

- Housing markets with lower homeownership rates tend to have more financially qualified renters. But even controlling for the homeownership rate, Silicon Valley renters appear to be exceptionally qualified.

- Across the country’s largest markets, 13.6 percent of on-market renters have strong credit scores and relatively high incomes and 13.8 percent could afford to buy the median home in their market.

The homeownership rate has steadily declined to generational lows over the past decade, pushing a broader-than-ever swath of Americans from all social and economic backgrounds into the rental market – including a large share that could likely afford to buy a home, but aren’t.

There are a number of factors driving this shift. Demographics play a role: Young adults are waiting longer to buy homes as they put off many of the decisions and events that typically accompany homeownership, including getting married and starting families. An evolving economy is also having an impact. Some locally booming labor markets – driven by tech or, until recently, energy – have attracted well-heeled newcomers who tend to rent before deciding whether to settle permanently.

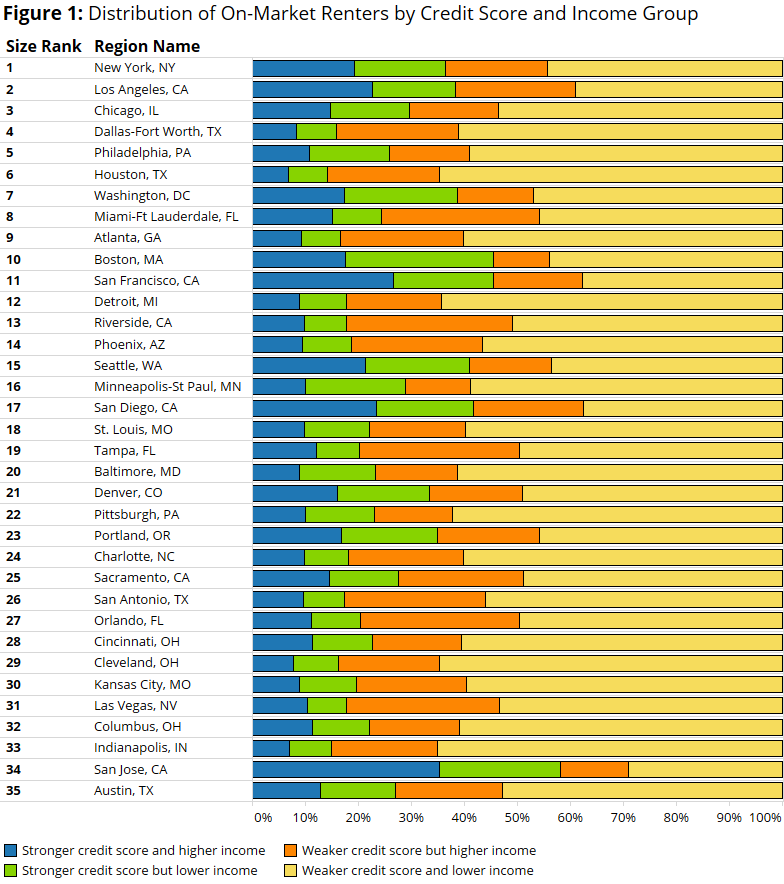

Using a unique Zillow dataset of on-market renters[1] based on Zillow’s Renter Profiles, we analyzed the self-reported credit scores and incomes of renters actively searching for a home during the first half of 2016 to assess which large housing markets have the most highly qualified renters.

For each of the markets with sufficient data, we grouped renters based on two criteria:

- Renters with a self-reported credit score of 700 or higher were classified as having a “stronger credit score.” Renters with a self-reported credit score below 700 were classified as having a “weaker credit score.”

- Renters with self-reported monthly income equal to or greater than the monthly income necessary to afford the typical rental in the metro area were classified as “higher income” renters. Those reporting a monthly income below this amount were classified “lower income” renters. We calculate the income necessary to afford the typical rental in the metro area using the Zillow Rent Index and Zillow’s Rent Affordability data.

We determined the distribution of renters across these groups for the country’s 35 largest housing markets (figure 1). Across these large markets, 13.6 percent of on-market renters on average have both stronger credit scores and higher incomes, while 53.1 percent have weaker credit scores and lower incomes. San Jose is the only large market analyzed where the share of on-market renters with strong credit and high incomes exceeds the share of on-market renters with weak credit and low-incomes.

The remaining renters are caught in a middle ground between the most- and least-qualified renters. On average across the large markets, 13.1 percent of renters have stronger credit scores but lower incomes, while 20.2 percent have higher incomes but weaker credit scores.

The remaining renters are caught in a middle ground between the most- and least-qualified renters. On average across the large markets, 13.1 percent of renters have stronger credit scores but lower incomes, while 20.2 percent have higher incomes but weaker credit scores.

Among these renters, it is generally much more common to encounter relatively high-earning renters with relatively low self-reported credit scores. This could be the result of several factors, including renters who experienced a temporary loss of income and/or foreclosure during the housing bust, contributing to a weak credit history, or younger adults with strong earnings but short credit histories.

A handful of metros – mostly areas with very strong labor markets including the Bay Area, Seattle, Washington, DC, Salt Lake City and Boston – buck this trend: The share of on-market renters with strong credit but low income exceeds the share with high income but weak credit.

Fewer Homeowners, More Well-Qualified Renters

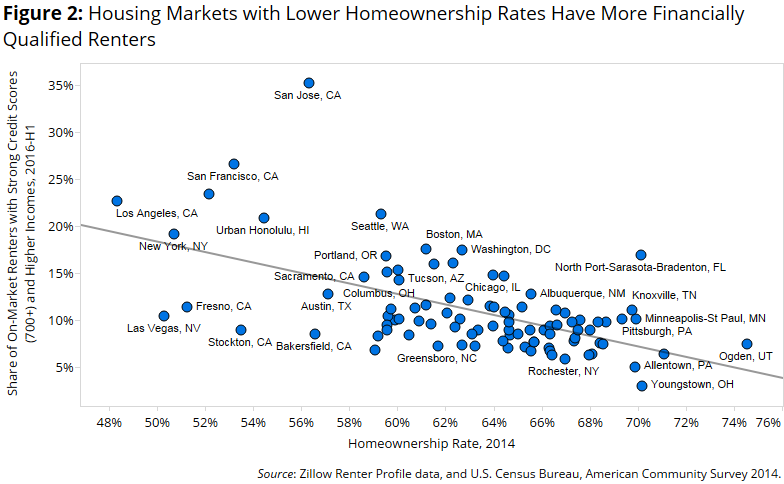

In general, markets with lower homeownership rates have higher proportions of on-market renters with both strong credit and high incomes (figure 2). This alone explains about one-third of the metro-to-metro differences in highly qualified renters. Still, even controlling for the homeownership rate, booming markets closely associated with the tech industry – such as San Jose and San Francisco – tend to have exceptionally high proportions of highly qualified, on-market renters. Interestingly, another outlier is North Port-Sarasota, Florida, where it’s likely a large number of older and/or retired renters contributes to a relatively high proportion of highly qualified on-market renters.

At the other extreme, several markets that were hit particularly hard by the housing bust and foreclosure crisis – including Las Vegas, Fresno, Stockton and Bakersfield – appear to have exceptionally low shares of highly qualified on-market renters.

At the other extreme, several markets that were hit particularly hard by the housing bust and foreclosure crisis – including Las Vegas, Fresno, Stockton and Bakersfield – appear to have exceptionally low shares of highly qualified on-market renters.

Qualified to Buy, Choosing (Having?) to Rent

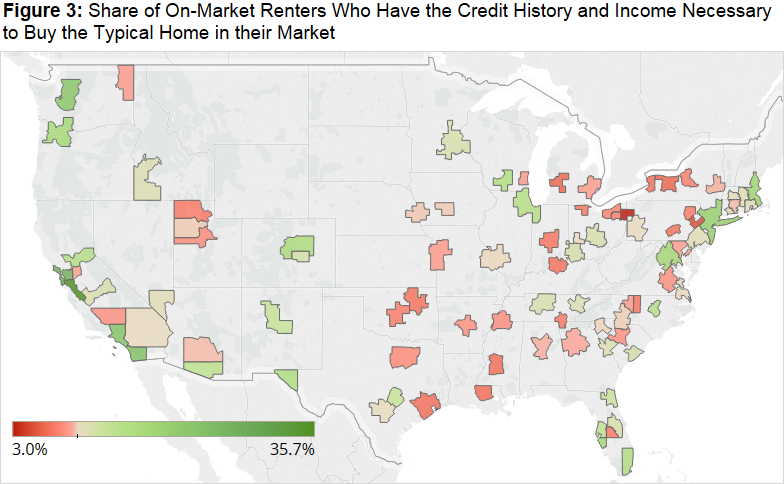

Given their credit histories and incomes, 13.8 percent of on-market renters could afford to buy the typical home in their market.[2] Many Americans of course prefer to rent for lifestyle reasons. And in some instances, these renters may be shopping simultaneously for both a home to buy or a home to rent.

But there are also other factors at play that could be preventing these renters from buying. The markets with the highest proportions of renters who could likely buy a home also tend to be the markets where for-sale inventory tends to be most constrained (figure 3). More than a third of on-market renters in San Jose could likely afford to buy a home in the area based on their credit histories and incomes, as could more than a quarter in San Francisco and more than a fifth in San Diego, Los Angeles and Seattle.

At the other extreme, a very small share of on-market renters could afford to buy in markets like Youngstown, Ohio, Allentown, Pennsylvania and Rochester, New York.

[1] On-market renters are actively searching for a rental unit. The data do not necessarily reflect the full spectrum of renters, only those who have created profiles on Zillow through mid-2016, but still likely capture an important segment of the rental market.

[2] We make several assumptions to calculate this share. In particular, we assume that the renter buys the median home in the metro area (using the Zillow Home Value Index) on a 30-year fixed rate loan carrying an interest rate of 3.5 percent and a 20 percent down payment. We also assume that they are willing to dedicate a proportion of their income to their monthly mortgage payment in line with Zillow’s current metro area mortgage affordability estimates.

{kind=link}