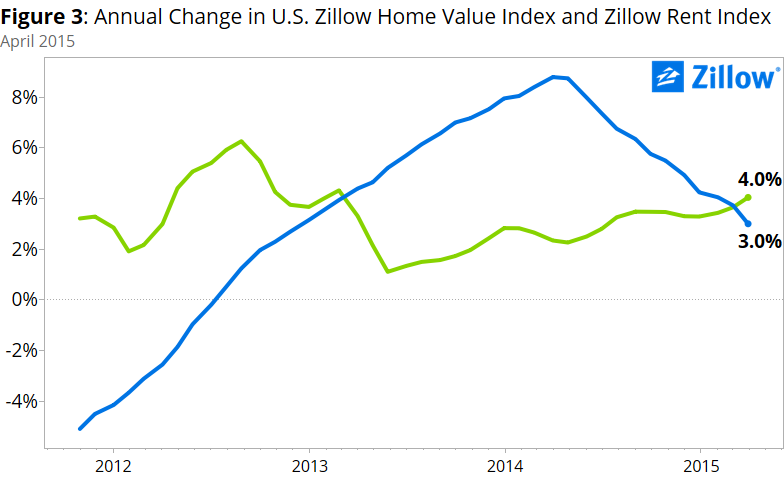

- U.S. rents grew at their fastest pace in two years in April, surpassing growth in home values.

- Rents grew faster than home values in 20 of the 35 largest U.S. housing markets.

- Home value growth is expected to slow further in the second half of the year as the for-sale housing market stabilizes.

At the end of last year, we predicted that 2015 would be a big year for home buyers. One of our main reasons for thinking this was our assumption that annual rental growth would eclipse home value growth this year, forcing many renters to consider the relative value and stability of homeownership and boosting the sales market.

We were right. But we’ll hold off on popping the champagne – for now, at least.

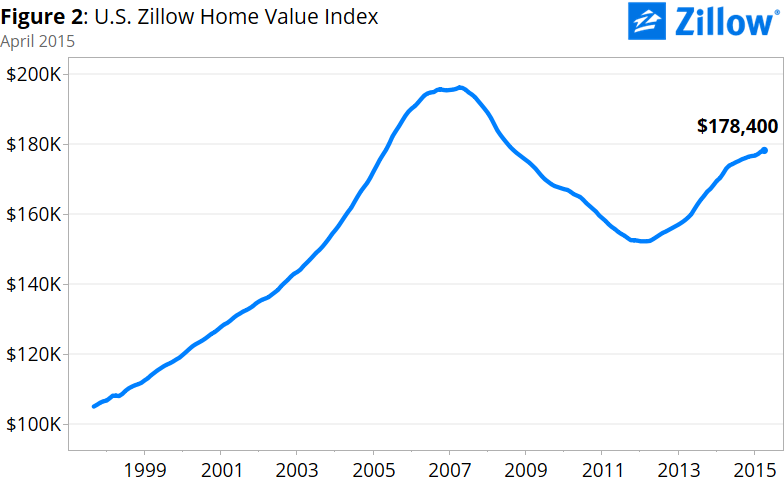

Home values in April ticked slightly upward from March, to a national Zillow Home Value Index of $178,400 – a 3 percent increase over last April. The Zillow Rent Index (ZRI) rose 4 percent year-over-year, to $1,364. Annual rents in April grew faster than home values in 20 of the 35 largest U.S. housing markets.

Rental demand is skyrocketing, thanks to a combination of younger workers staying in rental housing longer and families turning to the rental market after losing their homes to foreclosure during the recession. Builders are doing what they can to keep up, but it can take a while to get large multi-family projects off the ground, and demand is very hot right now.

Our assumption was, and still is, that those current renters who can afford a down payment, qualify for a loan and find an affordable home to buy would be very tempted to buy a home, especially as rental affordability worsens in the face of rising rents and flat wages. Currently, the typical renter should expect to spend about 30 percent of his or her income on the median rental home, up from 25 percent historically. Home buyers, on the other hand – thanks largely to low mortgage interest rates and home values that remain below their recent peaks in many areas – should expect to spend just 15 percent of their income on a mortgage, down from 21 percent historically.

Add in the fact that mortgages are getting easier to obtain as minimum credit scores fall, and it all adds up to what should be a banner year for home sales. But while the conditions we’re seeing are right in line with what we expected, the volume of sales we’re seeing has been underwhelming, at best.

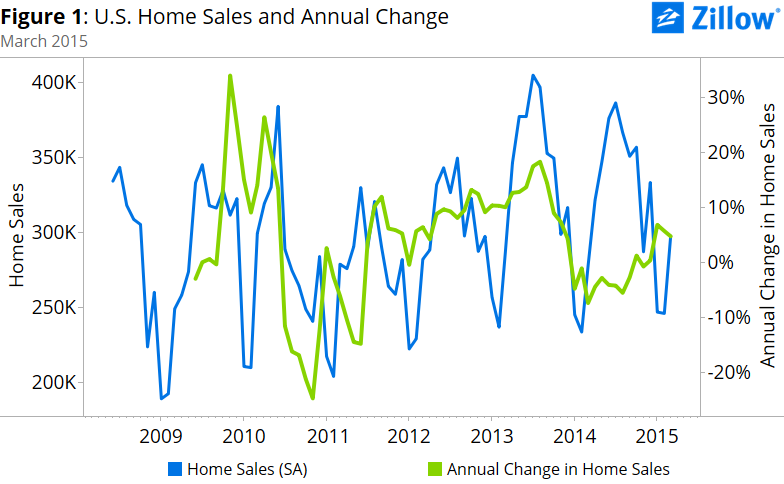

The seasonally adjusted total number of recorded U.S. home sales measured by Zillow was up 4.7 percent year-over-year as of March, which on the surface is a positive sign. But that 4.7 percent bump is the smallest annual gain observed so far this year – down from annual gains of 6.8 percent and 5.6 percent in January and February, respectively.

The seasonally adjusted total number of recorded U.S. home sales measured by Zillow was up 4.7 percent year-over-year as of March, which on the surface is a positive sign. But that 4.7 percent bump is the smallest annual gain observed so far this year – down from annual gains of 6.8 percent and 5.6 percent in January and February, respectively.

And total sales fell 6.4 percent in March compared to February – a month when buyers typically emerge from their winter slumber and begin to kick the tires on homes to buy, boosting monthly sales volume. In four of the past six years, dating to 2010, sales have increased in March over February, falling only this year and last year.

Looking ahead, we expect more weakness in both new and existing home sales in April, in part driven by continued low levels of inventory, especially at the low-end of the market.

Even so, while sales volumes this year have been less-than-inspiring, it’s still very early. The real spring home shopping season is just starting to heat up, and should last through the early fall, before it’s time for kids to head back to school. And there are some encouraging signs. The price of newly built homes has fallen each month since November, potentially signaling a shift in construction away from higher-end homes and towards the needs of the younger, more entry-level home shoppers we expect to make up the bulk of buyers this year.

Which, of course, we also predicted.

Slowing & Steadying Home Value Growth

The April 2015 Zillow Real Estate Market Report covers 507 metropolitan and micropolitan areas. In April, home values rose year-over-year in 358 out of 507 metros.

The April 2015 Zillow Real Estate Market Report covers 507 metropolitan and micropolitan areas. In April, home values rose year-over-year in 358 out of 507 metros.

The median U.S. home value was $178,400 in April, up 0.2 percent from March and 3 percent from April 2014. Annual appreciation in home values peaked at 8.8 percent in April 2014, and the rate of appreciation has declined each month for the past year. Home values remain 9 percent below their April 2007 peak of $196,400.

Of the largest 35 metro areas covered by Zillow, Denver continues to be the fastest-growing market, up 14.2 percent annually. San Jose (11.9 percent), Dallas (11 percent), San Francisco (10.3 percent) and Miami (9.9 percent) rounded out the top five fastest-growing large metro markets. Home values in 34 of the 35 largest metros grew on an annual basis, with 23 metros growing faster than the U.S. as a whole.

Rapidly Rising Rental Growth

U.S. rents grew 4 percent year-over-year in April, to a Zillow Rent Index (ZRI) of $1,364.

U.S. rents grew 4 percent year-over-year in April, to a Zillow Rent Index (ZRI) of $1,364.

Of the 862 metropolitan and micropolitan areas covered by the ZRI, 620 experienced year-over-year rent increases in April. Nationwide, rents have risen for the past 11 months when compared to the month prior.

Annual rental appreciation in 17 of the 35 largest metro areas covered by Zillow exceeded 5 percent in April, and rents in 23 of those markets grew faster than in the U.S. as a whole. The San Francisco metro experienced the highest annual rent appreciation among large markets, up almost 15 percent since April 2014. Other markets with double digit appreciation in rents were San Jose (12.9 percent) and Denver (11.6 percent).

Looking Ahead

Zillow expects U.S. home values to grow another 2 percent through April 2016, according to the Zillow Home Value Forecast, continuing the stabilization of the for-sale housing market. But stability in the purchase market isn’t being matched in the rental market, which shows few signs of slowing. There are tremendous incentives to get into homeownership these days: mortgage access is improving, interest rates are low and home values remain below prior peaks. But it will be increasingly difficult for many renters to realize these benefits as the country’s growing rental affordability crisis continues to worsen. More income going to rent means less going to savings for a down payment and other costs, keeping renters renting longer and feeding into the high demand that is contributing to rising rents in the first place. This cycle will be difficult to break, and it is a symptom of the imbalances that still exist in the housing market as we struggle to get back to normal. New construction, increasing for-sale inventory and rising wages will help, but none are coming very quickly.